Bankwest's Breeze Platinum Mastercard is Finder's winning Travel Credit Card at the 2026.00 Finder Credit Card Awards. The card combines 0% foreign transaction fees with a low annual fee.

Yes, you can use any credit card when you travel internationally. Just like in Australia, the business will need to accept card payments, but that's common in a lot of popular travel destinations.

Keep in mind that many credit cards and debit cards charge a 2-3% foreign transaction fee when you make payments in another country. So before you go overseas with your everyday card, check its foreign currency fee to make sure it's affordable.

If you're trying to save money, the best credit card to use overseas is likely one with 0% foreign transaction fees. If you want a card that can help you earn points and get you there for free, you can compare frequent flyer credit cards.

We currently don't have that product, but here are others to consider:

How we picked theseThere are 4 main types of credit cards that offer features and benefits for travellers:

A credit card is not your only option to spend money overseas.

"Last time I went overseas I didn't use a credit card once I landed. I used a Wise multi-currency card, which I was able to pre-load in the local currency for a small fee and a pretty competitive rate. Then I just used that card as if it was a local debit card. It was quick to top up mid-journey as well. But I did book flights, hotels and a hire car in advance using a credit card that earns frequent flyer points."

Planning your next trip? Check out our selection of frequent flyer credit cards and see if you can get a few thousand bonus Qantas or Velocity Points when you book your trip.

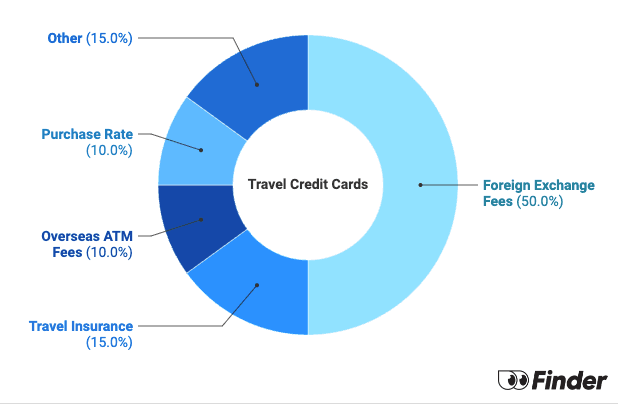

The Finder Score gives you a simple score out of 10, the higher the better. In the travel card category we examine 250+ credit cards and assess six features, assigning them scores out of 10.

We look at features like international transaction fees, travel insurance, annual fees and the purchase rate. Cards with 0% foreign transaction fees and other travel perks score higher.

The methodology is designed by our insights and editorial team. Commercial partnerships carry no weight, all products in the database are scored objectively.

The same card will receive a different score within each category, depending on the features being assessed.

Our intention is to enable informed financial decision-making quickly and easily. Please consider your own financial circumstances when making a decision.

"I always travel with my CBA Gold card. It has no foreign transaction fees and also has travel insurance included. The other benefit to using credit cards when you travel is that any fraud happens, it is dealt with swiftly by the bank."

Each year the Finder Credit Card Awards recognises Australia's top credit cards, with expert analysis of rates, fees and offers based on 12 months' worth of data. Here are the top performing travel credit cards.

Bankwest's Breeze Platinum Mastercard is Finder's winning Travel Credit Card at the 2026.00 Finder Credit Card Awards. The card combines 0% foreign transaction fees with a low annual fee.

Bankwest's Breeze Platinum Mastercard is Finder's winning Travel Credit Card at the 2026.00 Finder Credit Card Awards. The card combines 0% foreign transaction fees with a low annual fee.

The Bendigo Bank Ready Credit Card finished highly commended in the Travel Credit Card category with its low fees and 0% foreign transaction fee.

The Bendigo Bank Ready Credit Card finished highly commended in the Travel Credit Card category with its low fees and 0% foreign transaction fee.

Bankwest's More Platinum Mastercard was highly commended in the Travel Credit Card category at this year's awards.

Bankwest's More Platinum Mastercard was highly commended in the Travel Credit Card category at this year's awards.

The Bank First Visa Platinum Credit Card ranked highly commended in the Travel Credit Card category with its 0% foreign transaction fee and complimentary travel insurance.

The Bank First Visa Platinum Credit Card ranked highly commended in the Travel Credit Card category with its 0% foreign transaction fee and complimentary travel insurance.

The Commonwealth Bank's Smart Awards Credit Card secured a highly commended place in the Travel Credit Card category with a 0% foreign transaction fee and rewards points.

The Commonwealth Bank's Smart Awards Credit Card secured a highly commended place in the Travel Credit Card category with a 0% foreign transaction fee and rewards points.

The Bankwest Qantas Platinum Mastercard was highly commended in the Travel Credit Card category with a combination of no foreign transaction fee, points earning potential and travel insurance.

The Bankwest Qantas Platinum Mastercard was highly commended in the Travel Credit Card category with a combination of no foreign transaction fee, points earning potential and travel insurance.

Bankwest's More World Mastercard finished highly commended in the Travel Credit Card category thanks to its 0% foreign transaction fee, reward points and complimentary travel insurance.

Bankwest's More World Mastercard finished highly commended in the Travel Credit Card category thanks to its 0% foreign transaction fee, reward points and complimentary travel insurance.

Bankwest's Qantas World Mastercard ranked highly commended in the Travel Credit Card category with a 0% foreign transaction fee, a strong Qantas Points offer and free overseas travel insurance.

Bankwest's Qantas World Mastercard ranked highly commended in the Travel Credit Card category with a 0% foreign transaction fee, a strong Qantas Points offer and free overseas travel insurance.

We're tracking every cut to a credit card points program ahead of the credit card surcharge ban.

Find credit cards that make international spending cheaper with 0% international transaction fees.

Applying for a new credit card or upgrading your current one? We've reviewed over 260 cards in Australia!

Insights and analysis on American Express credit cards, costs, acceptance and more.

Get a percentage of your spend back, gift cards or vouchers with a cashback credit card. Find out more and compare current offers in our guide.

You deserve the best credit card. Let us help you find it.

Compare the best Qantas frequent flyer credit cards based on bonus point offers, points per $1 spent, rates, fees and other features so you can find a card that works for you.

Check out bonus point offers and travel perks such as lounge access and complimentary insurance with these Velocity Frequent Flyer credit cards.

Read through this guideline to help protect yourself from any unauthorised transactions from your credit card.

Find out how you can keep your overseas spending costs down by comparing credit cards with no foreign transaction fees and no currency conversion fees.

Hi, Could i ask you to update this International credit card information?

Latitude 28Degrees is changing to an $8 monthly fee as of September/October 2024.

They have sent me the info.

Thanks Stephen, we had made a note to update this on the date of the change coming into effect (Sept 17) but we have updated in advance for full transparency.

A quick note that the Bendigo Ready Credit Card also has a good travel insurance option where you don’t need to pay the whole cost of your travel on the card to activate the travel insurance, just a portion. So, if you have already bought your overseas tickets, and don’t want to pay extra for travel insurance, you might still be able to claim using this card – read the PDS to see the rules. It is also one of the only cards that still has rental car excess reduction on it – so I book all my rental cars through this card

Which cards are best for 2 card holders (husband & wife)?

Hi Saija,

Most credit cards in Australia allow you to share your account with someone by getting an additional card for them that’s linked to your account. A few credit cards also offer joint accounts, where both people share legal responsibility for the credit card account. You can learn more and compare different options in Finder’s guide to joint credit cards. I hope that helps.

Hi Valerie,

Thank you for getting in touch with Finder.

As of this writing, there are some credit cards offering travel insurance for over 65. NAB covers up to 90 years old while Virgin Money, HSBC, and Citi did not include the traveler’s age limit so long that there’s no pre-existing medical condition.

It is recommended that you contact your chosen provider on this matter for further clarification. Once you have decided which credit card to apply with, please make sure though to read the eligibility criteria, features, and details of the card, as well as the relevant PDS/ T&Cs of the card before making a decision and consider whether the product is right for you.

I hope this helps.

Thank you and have a wonderful day!

Cheers,

Jeni

If I have a 28 degrees Mastercard, does it mean when I withdraw cash from an overseas ATM that there will not be a withdrawal fee?

Thanks for your help in clarifying my query.

Hi Bebe, thanks for your inquiry!

The 28 Degrees MasterCard provides no international transaction fees on purchases, which only covers currency conversion rate charges. Overseas ATM withdrawals may still incur a charge, depending on the local ATM’s withdrawal policies and fees.

Cheers,

Jonathan