0% foreign transaction fees is just the beginning. The best international credit cards in Australia also give you travel insurance, lounge access and points.

The best credit card to use internationally is one that doesn't charge international or foreign currency conversion fees.

Beyond this feature, a good card should also have a low annual fee and offer perks like complimentary travel insurance.

But a credit card is not your only option for international spending. Consider a debit card with 0% foreign transaction fees or a travel money card.

Best international credit cards

Every month at Finder we analyse all the credit cards in our database with 0% foreign transaction fees and rank them using the Finder Score system.

The top scoring credit cards all have 0% international transaction fees, but also score highly if they have complimentary travel insurance, low overseas ATM fees and low annual card fees.

Updated August 2026 by Finder's senior money editor, Richard Whitten.

How to find the best international credit card for you

The most important factor: 0% international transaction fees

The best international credit cards all offer 0% foreign transaction fees. That's the most important feature to look at because it saves you a lot of money when using the car overseas.

Many credit cards charge around 3% for every transaction in a foreign currency. That includes:

Example: saving money with a 0% foreign fee credit card

Let's say you spent $3,000 on your credit card while travelling overseas. A 3% fee would cost you $90.

So a 0% foreign transaction fee is really what makes a credit card great for international use, whether you're travelling or shopping overseas.

5 more factors to compare when finding the right international credit card

The annual fee. A lower annual fee makes a big difference to the cost of your international credit card. Card annual fees range from $55–$400, and some cards don't charge an annual fee in the first year.

Overseas ATM fees. Many credit and debit cards charge a fee for using ATMs overseas. But some don't, so this can make a big difference.

Complimentary travel insurance. Many travel-oriented credit cards offer free travel insurance cover. To qualify, you need to book some of the travel costs (like flights or accommodation) using the card. It's a great benefit, especially if you plan to use the card internationally.

The purchase rate. This is the interest rate you get charged on your card spending if you don't repay the card balance in full each month. Many credit cards charge up to 22%. But if you repay your card spending in full, you won't get charged interest.

Extra perks and benefits. Credit cards come with all kinds of benefits, from cashback on spending to complimentary insurance cover like purchase protection and the ability to earn reward points.

International credit card fees

International transaction fees (sometimes called foreign currency conversion fees) on Australian credit cards range from under 1% up to 3.65% of a transaction. Most cards charge a 3% fee. There are fewer than 30 cards on the market that don't charge international transaction fees.

Source:Finder's credit card database

All the perks and benefits of 0% foreign fee cards

Many of the best international credit cards in Finder's database offer some of these extra benefits. Just keep in mind that the more benefits a credit card offers the higher the annual fee.

Interest-free days on purchases. This is a standard feature on most credit cards but important, and worth comparing. Interest-free days mean you can spend on the card and not get charged interest for longer. Some cards give you 44 days from the start of your statement period before charging interest, some are as high as 55 days.

Reward points. Many credit cards let you earn rewards points on your spending. There are bank rewards programs like Commbank Award Points or NAB Rewards Points, plus Amex's Membership Rewards Points.

Cashback. Some credit cards let you earn cashback on your spending. Usually this is capped at a percentage of your spending, and it effectively offers a small discount on your card spending.

Insurance cover. Beyond travel insurance, many international credit cards offer purchase protection insurance or extended warranties. Very useful if you're making big purchases. Just keep in mind extended warranty cover typically only applies to domestic purchases, not international ones.

Alternative travel card options

You don't have to use a credit card with 0% international fees when spending internationally. Your best option may be one of these:

Use a debit card with no international transaction fees

If you've got the money to spend already (so you don't need credit), a debit card with 0% foreign currency conversion fees is a good option.

Popular bank accounts with debit cards and 0% international transaction fees include:

You can load up a prepaid travel money card with a foreign currency before you travel. This is a really cost-effective method and you can lock in your exchange rate before you travel.

These aren't credit cards, and you'll need to add money to them before you travel or when you're on the road.

With most credit cards you really just need to pay the annual fee to keep the account active.

If your card offers rewards points, you'll only earn points when you spend money with the card. And if there's a bonus points offer you'll need to spend a certain amount within a given time frame.

When you make an international credit card transaction with an Australian card, the transaction is converted into Australian dollars. Mastercard and Visa have their own conversion rates.

Some overseas merchants may let you pay in Australian dollars instead, using something called Dynamic Currency Conversion (DCC).

According to the Commonwealth Bank, DCC rates and fees are "determined by the merchant" and while convenient,"you'll often end up paying more for the transaction."

You may be better off paying in the local currency if you have the option.

Plenty of debit cards have similar international transaction fees to credit cards. But we've listed several options that don't charge a fee, like the Suncorp Everyday Options account, the Ubank Spend account and the HSBC Everyday Global account.

These cards offer lower currency conversion fees and relevant perks for travelers like insurance and ATM access.

7+

Great

Reasonable cards for travelers, however can potentially charge higher fees.

5+

Standard

While eligible to be used to travelers internationally, these cards may charge currency conversion, overseas ATM withdrawal and ongoing fees.

0+

Basic

These cards should be used for international purchases only in the event of an emergency.

How the Finder Score works

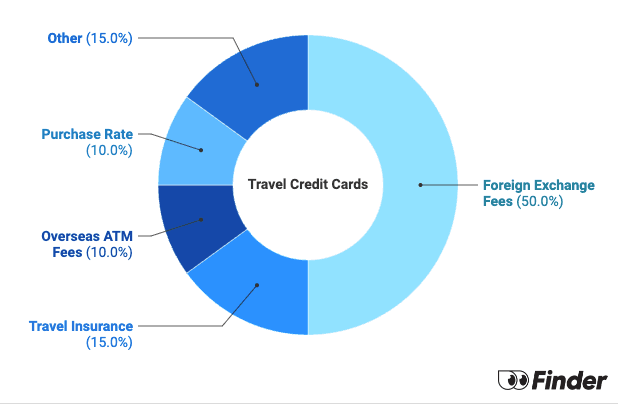

The Finder Score gives you a simple score out of 10, the higher the better. To determine the best credit cards for travel and international use we examine 250+ credit cards and assess six features, assigning them scores out of 10.

This includes international transaction fees, travel insurance, annual fees and the purchase rate. Cards with 0% foreign transaction fees and other travel perks score higher.

The methodology is designed by our insights and editorial team. Commercial partnerships carry no weight, all products in the database are scored objectively.

9+ Excellent - These cards offer lower currency conversion fees and relevant perks for travellers like insurance and ATM access.

7+ Great - Reasonable cards for travellers, however can potentially charge higher fees. 5+ Satisfactory - While eligible to be used to travellers internationally, these cards may charge currency conversion, overseas ATM withdrawal and ongoing fees.

Less than 5–Basic - These cards should be used for international purchases only in the event of an emergency.

Finder Score metric assessment - Travel credit cards

Feature

Definition

Assessment

Weight

Foreign Exchange Fees

Fees charge on international transactions

Lower fees score higher

50%

Travel Insurance

Complimentary travel insurance

Full score for complimentary insurances

15%

Overseas ATM Fees

Fees charged by card provider to withdraw from international ATMs

Lower fees score higher

10%

Purchase Rate

Interest rate on new purchases

Lower rates score higher

10%

First-Year Fee

Annual fee charged in the first year of ownership

Lower fees score higher. $0 fee receives the maximum points.

7.5%

Ongoing Annual Fee

Annual fee charged from the second year onwards

Lower fees score higher. $0 fee receives the maximum points.

Richard Whitten is Finder’s Senior Money Editor, with over eight years of experience in home loans, property, credit cards and personal finance. His insights appear in top media outlets like Yahoo Finance, Money Magazine, and the Herald Sun, and he frequently offers expert commentary on television and radio, helping Australians navigate mortgages and property ownership. Richard started his career in education and textbook publishing in South Korea. He holds multiple industry certifications, including a Certificate IV in Mortgage Broking (RG 206) and Tier 1 and Tier 2 certifications (RG 146), as well as a Bachelor of Education from the University of Sydney and a Graduate Certificate in Communications from Deakin University.

See full bio

Richard's expertise

Richard

has written

779

Finder guides across topics including:

Compare credit cards that give you an outcome within 60 seconds of when you submit your application online and find out how to increase your chances of getting this type of "instant" credit card approval.

Compare the best Qantas frequent flyer credit cards based on bonus point offers, points per $1 spent, rates, fees and other features so you can find a card that works for you.

When you apply for a credit card online, you could receive a response within 60 seconds. Find out how you to find a card that you're eligible for and increase your chances of approval.

Find out how you can keep your overseas spending costs down by comparing credit cards with no foreign transaction fees and no currency conversion fees.

Important information about this website

Finder is a comparison service. We do not compare every product or every provider in the market.

We make money through commercial arrangements with some of the providers on this site. Products marked 'Sponsored', 'Promoted', 'Featured' or 'Advertisement' appear as a result of a commercial arrangement.

Our editorial content, product reviews and any 'Top Pick' designations are prepared independently of these commercial arrangements.

The default order of products in our tables can be influenced by commercial arrangements. You can re-sort or filter using the controls above each table.

Some content on this site may be generated or supported by AI tools. You should verify details directly with the provider.

Finder is one of Australia's leading comparison websites. We are committed to our readers and stand by our editorial principles.

Our comparison service does not include every product or every provider in the market. Some product issuers offer their products under multiple brands or through associated companies. Where we can, we identify the underlying issuer so you can compare like with like, but you should always check with the provider directly to confirm which brand you are dealing with.

Finder is a comparison website and an intermediary. We are not a product issuer and we do not provide personal financial or credit advice. When you click a link to a product, or apply for a product through our site, you deal directly with the product issuer. We may receive a referral fee, commission or other payment from the issuer if you click through, apply or take out a product. We describe these arrangements in more detail under 'How we make money' below.

Product features, fees, terms and eligibility criteria are set by the product issuer and may change. We rely on information supplied by issuers when we present product details on our site. Before you apply for or take out any product, you should confirm the details directly with the issuer.

We earn revenue from Finder in four principal ways:

Referral fees and commissions. When you click a product link, complete an enquiry form or apply for a product through our site, we may receive a referral fee, commission or other payment from the product issuer. We may also receive payment based on the volume of leads or conversions we send to an issuer.

Sponsored placements. Products marked 'Sponsored', 'Promoted', 'Featured' or 'Advertisement' appear as a result of a commercial arrangement between Finder and the issuer. These labels always indicate a paid placement. We do not use them for editorial choices.

Display advertising. Banner advertising, newsletter advertising and similar display ads on our site are paid by advertisers.

Content sponsorship. Some articles, videos and social media posts are sponsored by an issuer and are clearly labelled as such.

Our editorial opinions, product reviews and any 'Top Pick' designations are prepared independently of these commercial arrangements. A 'Top Pick' is an editorial choice made by our writers and editors based on the criteria described on each comparison page. A 'Top Pick' is not a personal recommendation and does not mean the product is appropriate for your circumstances.

If you would like to know whether we have a commercial arrangement with a specific product issuer, please contact us.

When products are grouped in a table or list, the default order can be influenced by commercial arrangements we have with product issuers. In some categories, sponsored or featured products appear in the top positions of the table by default, and are always labelled as such.

Other factors that influence default order include price, fees and features, and (where relevant) our editorial view of the product.

You can re-sort every comparison table using the controls above the table. You can filter by product features that matter to you. The order you see after re-sorting or filtering is not influenced by commercial arrangements.

Some content on this site is generated or supported by artificial intelligence tools, including our AI-powered assistant FinderBot. AI-generated content may contain errors. Please verify important information directly with the product issuer before making a financial decision. For more information about FinderBot, see the FinderBot Terms of Use and FinderBot Privacy Collection Notice.

Please read our website terms of use and privacy policy for more information about our services and our approach to privacy.

We update our data regularly, but information can change between updates. Confirm details with the provider you're interested in before making a decision.

Our goal is to create the best possible product, and your thoughts, ideas and suggestions play a major role in helping us identify opportunities to improve.