A personal loan can usually be used for a number of worthwhile personal reasons, like making a large purchase, completing home improvements, or consolidating debt.

Personal loan interest rates are often personalised depending on the borrower's credit score, which is why there are minimum and maximum rates for each loan.

You can choose between a secured or unsecured personal loan: a secured personal loan usually has lower interest rates, but you put an asset at risk.

Finder's picks for the best personal loans for July 2026

The crème de la crème of personal loans. These products offer the lowest cost loans accompanied by the best features.

7+

Great

Slightly higher in cost and fewer features, but these products are still competitive.

5+

Standard

Typically offering above average rates and possibly lacking in the features department.

0+

Basic

The least competitive in terms of both cost and features.

What is a personal loan?

A personal loan is money that you borrow to cover the cost of expensive purchases such as a holiday, a car, a renovation, a wedding or medical bills. You repay the loan, plus interest and fees, over time.

Personal loan amounts can often be anywhere from a few hundred dollars up to $100,000. Typically, personal loans are used for larger expenses that can't easily be covered by your savings or other forms of borrowing like Buy Now Pay Later or a credit card, which are usually used for smaller costs.

The features of a personal loan

Loan terms. Usually 1 to 7 years.

Personalised interest rates. Many lenders determine your personal loan interest rate based on your credit score, income and other factors.

Loan purpose. A personal loan can be used "for any worthwhile purpose". But you can't use a personal loan to gamble or invest.

How do I compare personal loans?

1

Look for a lower interest rate

The lower the rate, the less interest you pay. You can choose loans with fixed or variable interest rates. Personal loans offer personalised interest rates tailored to your credit score, so the minimum advertised rate may not be what you're offered.

2

Look for a loan with lower fees

Factor in the cost of any application or establishment fees, plus the ongoing monthly service or account fee. You can spot a loan with high fees by looking at the comparison rate.

3

Consider your loan size

You won't be able to borrow $30,000 if the lender's maximum loan amount is $25,000.

4

Decide your loan term

Most lenders offer terms of 1 to 7 years. Longer terms mean lower monthly repayments but you end up paying more interest. Shorter terms mean less interest and you'll pay off the loan faster, but you pay more each month.

5

Look at the features included

Some lenders let you repay the loan faster, so you can get out of debt quickly. Some even let you redraw those extra repayments to spend in an emergency. Other popular features include a lender's app, which can make it easier to track and manage your debt.

6

Keep an eye out for sneaky extra costs

Be aware if any break fees or early repayment fees apply to your personal loan in the event you pay out your personal loan earlier than the original loan term.

Compare personal loans in under a minute

No contact details required

How your credit score affects your personal loan rate

Most lenders in Australia use risk-based pricing for personal loan interest rates. Every borrower gets a different rate based on their credit score and their own circumstances.

If you have an Excellent credit score you can get a lower interest rate. If your score is Good or Average the rate will be higher.

You can check your credit score for free through Finder before applying for a personal loan. If you have an Average or Bad credit score you can improve it before applying for credit.

How do I know what my personal loan repayments will be?

Because your rate will be personalised it's best to get a quote from a lender once you are comfortable you fit its eligibility criteria. That quote should include the interest rate you are offered, as well as any fees.

When you have that information, use a personal loan calculator to be able to confidently tell what your repayments will be.

Compare personal loan types

Unsecured personal loans

Unsecured personal loans mean you're still responsible for repaying the loan, but you don't have to offer a car, property or other asset as security for the loan. This usually means a slightly higher rate.

Secured personal loans

A personal loan secured by an asset, such as a car, term deposit or home equity. If you fail to repay the loan, the lender can take the asset. Secured loans often have lower rates and better terms since the risk to the lender is lower.

Car loans

While you could buy a car with a typical personal loan, rates are often better if you specifically take out a car loan. You can buy a car with a secured or unsecured loan, depending on the car you're buying. Banks and lenders offer car loans, and so do many car dealers.

If you have a bad credit score and a history of financial trouble you can still get a personal loan. Bad credit personal loans have higher rates, so be careful when taking one out as they are not long-term financial solutions.

Before getting a personal loan you should always check that you can afford the personal loan repayments and ask yourself whether you really need the loan.

If you are in a financial emergency, you should understand that taking out a loan may trap you in a cycle of debt. For more resources and support, visit the Australian government's MoneySmart website.

Alternatives to personal loans

Personal loans are suited to borrowers looking to fund specific, one-off purchases or expenses, like a car, a wedding or a holiday. But there are other forms of credit that borrowers can use.

But remember that some of these options may be riskier and more expensive than a personal loan.

Credit cards.A credit card lets you spend money flexibly, up to an approved limit, and pay it off over time. If you manage your card well, it can be a good form of credit. For smaller purchases it could be cheaper than a personal loan. But if you don't stay on top of your repayments, you'll end up paying a high interest rate month after month.

Buy now pay later (BNPL). Many Australians use BNPL to cover small purchases in a similar way to a credit card. BNPL services are easy to use and don't charge interest, which can be a trap. You have to pay fees, and if you miss repayments then you'll get hit with more fees.

Pay on demand.Pay-on-demand platforms let you access a portion of your salary before payday, but you'll pay a fee to do so. This might be a convenient short-term solution but if you find yourself repeatedly accessing your salary early and paying a fee to do so, you could find yourself falling further behind financially.

Payday loans. These are short-term loans limited to $2,000. They are an emergency option but an expensive one. Payday lenders don't charge interest but instead charge hefty fees.

How much are Aussies borrowing?

According to Finder's Consumer Sentiment Tracker, there's a distinct difference between the amount of debt carried by different generations. While Gen X have an average of $9,346 in debt, millennials have $7,861 and the younger Gen Z has $5,473 in personal loan debt.

Compare personal loan products. You can use our table to find one that suits your needs and has a low interest rate.

Check the lender's eligibility criteria. There's no point applying for a loan you can't get. Make sure you meet the employment, residency and income requirements.

Check your credit score and get a quote. Knowing your credit score helps set your expectations for what interest rate you'll be offered and helps you spot ways to improve your score. Lenders can also provide quotes to give you an idea of your loan.

Submit your application. You'll need some ID and details about your income, spending and employment.

Wait for approval. Most lenders can process a personal loan application within 1 business day. Some can do it in hours.

Documents you need for your personal loan application

ID. A driver's licence, Medicare card, passport or birth certificate.

Proof of income. Payslips, bank statements, a tax return or letter of employment.

Other debts. You may need to provide an account statement from other debts you have, including loans or BNPL accounts.

Security. If the loan is secured you'll need to provide some details about the car or asset offered as security. This can include a tax invoice from a car dealership and evidence of a car insurance policy.

"When I took a personal loan recently it was a smooth and quick experience. I was approved for the loan with the repayments I was happy with. One thing that helped me out was knowing early on what I can afford to pay on the loan."

Raj Lal

Publisher

FAQs about personal loans

The average interest rate for unsecured personal loans in Australia is 10.32% p.a (as of April 2026). This is the average rate taken from Finder's database, based on an individual with Excellent credit.

Your own credit score, and therefore the rates you are offered, may differ.

There's no simple answer for which bank is best for your personal loan. Your credit score and relationship with the bank will impact the rate you are offered. Comparison tables can help you understand the full interest rate ranges banks offer. It's best to see which is offering the lowest rates, check to see if you match its eligibility criteria and then get a quote. It may also be worth looking at non-bank lenders, as they operate under the same regulation as banks and can have more competitive rates.

For a quicker answer, Finder has done its own research into our top picks for the best personal loans.

Whether you get a personal loan from a Big Four bank, a smaller lender or an online lender, you'll most likely be applying online anyway.

Here are your main lender options:

Big Four banks. If you already bank with CommBank, Westpac, NAB or ANZ then it can be easier to get a personal loan approved. And you'll have all your accounts in one place. Keep in mind that the Big Four may have less competitive rates than online lenders.

Other banks and institutions. Smaller than the Big Four, banks like ING, Bendigo Bank, Bank of Queensland and many others offer personal loans. Then there are financial service companies like Latitude that specialise in personal lending.

Online lenders. There are many online lenders that offer personal loans with fast approval times and competitive interest rates. Examples include Humm, Harmoney, Now Finance and Wisr.

Credit unions. These member-owned organisations are similar to banks but are often more local and smaller. Credit unions offer personal loans that sometimes have quite competitive rates. Some offer online service while many have physical branches in certain towns and cities.

Most unsecured loans offer amounts between $2,000 and $50,000, while secured loans offer up to $100,000. But the actual amount you can borrow depends on factors including your credit score and ability to make repayments.

A good unsecured personal loan interest rate is around 6–15% for people with an Excellent credit score. Personal loans use your credit score to determine the rate, with higher scores leading to lower rates. As a guide, Finder analysis shows most Australians have a Good or Very Good credit score.

An Australian credit score of 550 is generally the minimum you need to qualify for a personal loan. This will likely be an expensive loan, as most Australian lenders use risk-based pricing.

Lower credit scores could qualify for payday or short term loans, though these will be more expensive than even a bad credit personal loan.

It usually takes a few business days to get the money from a personal loan once your application is approved, but it does vary.

Some banks are able to offer existing customers same-day personal loans.

Some payday lenders also offer 1-hour turnarounds but these loans come with risks including higher interest rates and fees.

There is no way to guarantee you're approved for a loan, but there are some key steps you can take before you apply:

Work out how much you can borrow. Lenders have criteria to decide how much you're eligible to borrow, but you also need to understand what is realistically affordable for you.

Maintain a good credit score or improve it. A lower credit score can reduce your chances of getting approved or mean you are offered a higher interest rate. If you already have a poor credit score, you can start improving it by limiting credit applications, paying bills on time and bringing down any limits on your credit card. It can take a while, but these are all good tactics to improve that credit score.

Keep track of your saving goals. If you manage to contribute to your savings regularly, it shows lenders that you are likely to manage ongoing loan repayments.

The lowdown on Finder Score

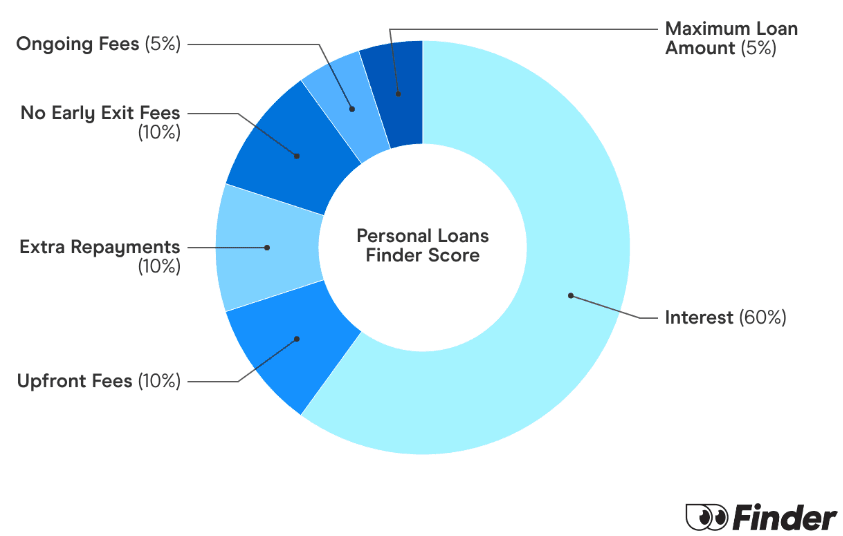

Wondering how we work out Finder Score? We look at 300+ personal loan products across 120+ lenders and we compare them against each other to get our simple score out of 10. Metrics like interest rates, fees and features are weighted and scaled to come up with individual Finder Scores. To give a fair and true personal loan comparison, unsecured and secured personal loan products are scored separately.

The Finder Score methodology is designed by our awesome insights team and reviewed by our just-as-awesome editorial team. Don't worry, commercial partners carry no weight and all products are reviewed objectively.

Finder Scores explained

9+ Excellent - The crème de la crème of personal loans. These products offer the lowest cost loans accompanied by the best features.

7+ Great - Slightly higher in cost and fewer features, but these products are still competitive.

5+ Satisfactory - Typically offering above average rates and possibly lacking in the features department.

Less than 5 – Basic - The least competitive in terms of both cost and features.

Richard Whitten is Finder’s Senior Money Editor, with over eight years of experience in home loans, property, credit cards and personal finance. His insights appear in top media outlets like Yahoo Finance, Money Magazine, and the Herald Sun, and he frequently offers expert commentary on television and radio, helping Australians navigate mortgages and property ownership. Richard started his career in education and textbook publishing in South Korea. He holds multiple industry certifications, including a Certificate IV in Mortgage Broking (RG 206) and Tier 1 and Tier 2 certifications (RG 146), as well as a Bachelor of Education from the University of Sydney and a Graduate Certificate in Communications from Deakin University.

See full bio

Richard's expertise

Richard

has written

758

Finder guides across topics including:

When you have a large expense that your savings can’t cover, a personal loan at a fixed rate from Great Southern Bank is an option worth considering. With no fees and a competitive fixed interest rate, this could be the right loan for you.

The Latitude Financial Service Personal Loan is a flexible loan with a competitive fixed interest rate, flexible repayment options and the ability to make additional repayments. Application is simple and can be completed online – find out if you're eligible.

Find out all about the range of Latitude personal loans before you apply. Whether you're looking for a secured car loan or an unsecured personal loan to consolidate debt or make a large purchase or investment, this is the guide for you.

The NAB unsecured 10k+ personal loan allows you to borrow money for the consolidation of debts, a holiday trip or a new car. Learn more about the features and benefits of this loan and how to apply online.

Finder makes money from featured partners, but editorial opinions are our own.

Finder is one of Australia's leading comparison websites. We are committed to our readers and stand by our editorial principles.

We try to take an open and transparent approach and provide a broad-based comparison service. However, you should be aware that while we are an independently owned service, our comparison service does not include all providers or all products available in the market.

Some product issuers may provide products or offer services through multiple brands, associated companies or different labeling arrangements. This can make it difficult for consumers to compare alternatives or identify the companies behind the products. However, we aim to provide information to enable consumers to understand these issues.

We make money by featuring products on our site. Compensation received from the providers featured on our site can influence which products we write about as well as where and how products appear on our page, but the order or placement of these products does not influence our assessment or opinions of them, nor is it an endorsement or recommendation for them.

Products marked as 'Top Pick', 'Promoted' or 'Advertisement' are prominently displayed either as a result of a commercial advertising arrangement or to highlight a particular product, provider or feature. Finder may receive remuneration from the Provider if you click on the related link, purchase or enquire about the product. Finder's decision to show a 'promoted' product is neither a recommendation that the product is appropriate for you nor an indication that the product is the best in its category. We encourage you to use the tools and information we provide to compare your options.

Where our site links to particular products or displays 'Go to site' buttons, we may receive a commission, referral fee or payment when you click on those buttons or apply for a product.

When products are grouped in a table or list, the order in which they are initially sorted may be influenced by a range of factors including price, fees and discounts; commercial partnerships; product features; and brand popularity. We provide tools so you can sort and filter these lists to highlight features that matter to you.

Please read our website terms of use and privacy policy for more information about our services and our approach to privacy.

We update our data regularly, but information can change between updates. Confirm details with the provider you're interested in before making a decision.

How likely would you be to recommend Finder to a friend or colleague?

0

1

2

3

4

5

6

7

8

9

10

Very UnlikelyExtremely Likely

Required

Thank you for your feedback.

Our goal is to create the best possible product, and your thoughts, ideas and suggestions play a major role in helping us identify opportunities to improve.