The crème de la crème of personal loans. These products offer the lowest cost loans accompanied by the best features.

7+

Great

Slightly higher in cost and fewer features, but these products are still competitive.

5+

Standard

Typically offering above average rates and possibly lacking in the features department.

0+

Basic

The least competitive in terms of both cost and features.

Key takeaways

The amount you can borrow often depends on the value of the asset you're using as security.

Loan amounts and terms vary, so comparing different lenders can help you find the best option.

Risk of losing your collateral exists if you default on the loan, so ensure you can manage the repayments.

What is a secured personal loan?

A secured loan uses an asset as collateral for the funds. This means that if you don't make your repayments, the lender can repossess and sell the asset to get their money back.

Offering security has several advantages, namely a lower interest rate and higher borrowing amount, as the risk for the lender is reduced compared to an unsecured personal loan.

With a secured loan, the value of your asset determines how much you'll be able to borrow. You can use a secured loan for a wide range of things from cars, to weddings, to home renovations.

What assets can be used to secure a personal loan?

New/used car

Using your car as collateral on a personal loan is one of the most common forms of loan security.

Home equity

If you're a homeowner with a mortgage, you can draw against any equity you have in the property to use as a personal loan.

Expensive items

These include high-cost jewellery, fine art, precious metals, prestige cars and antiques.

Term deposits

You can sometimes borrow near the amount of money in a term deposit if you use it as security a loan.

Pros and cons of a secured personal loan vs an unsecured personal loan

Pros

Lower interest rate: Because these loans are less risky for lenders, you'll usually be offered a lower interest rate than you would with an unsecured loan.

Better chance of approval: Even if you're ineligible for an unsecured loan, you may still be eligible for a secured loan - again, because they are less risky for the lender. This could be beneficial for part-time or casual employees and bad credit borrowers.

Higher borrowing amounts: Depending on the value of your asset, you may be able to borrow up to $100,000.

More flexible: With the exception of car loans, you can use a secured personal loan for a variety of reasons.

Cons

Risk to your asset: Your asset acts as the guarantee for the loan. If for some reason you are unable to make your repayments, the lender can repossess and sell your asset to get their money back.

Borrowing amount limitations: The value of your asset determines how much you'll be able to borrow. So if you need a larger amount than what your asset is worth, you may find the loan not fit for purpose.

Our expert says

"Secured loans aren't just for borrowers who are ineligible for an unsecured loan. Even though you put an asset at risk, if you know you'll be able to make your repayments, you may opt for a secured loan for a lower interest rate."

Interest rates: The interest rate is what the lender charges you for borrowing money. This is presented as a yearly percentage. The lower the interest rate, the lower the cost of the loan. By comparing lenders, you can work out if the rate is competitive.

Fees: Upfront or ongoing fees will add to the cost of your loan. As a guide of the true cost of the loan you can look at the comparison rate which includes both interest and fees. It's presented as a percentage and displayed next to the interest rate.

Loan term: This is how long you have to repay the loan. Secured loans offer terms from 1 to 7 years. Longer terms mean lower monthly repayments, but also mean that you'll end up paying more in interest charges.

Asset requirements: Before you can be approved for a secured loan, the lender will need to accept your asset. You'll be able to compare requirements before you apply. These criteria typically include the age and value of your asset.

Repayment flexibility: You can usually choose between weekly, fortnightly or monthly. You may also want the ability to make extra repayments without penalty, so you can save on interest costs and pay off the loan earlier. Variable rate loans typically offer more flexibility when it comes to early repayment.

Eligibility: Lenders will take into account your personal circumstances, including your income, credit score, assets and liabilities, when you apply.

Should I choose a fixed rate or a variable rate?

Whether variable rates are higher or lower, they can change at any time at the lender's discretion. Fixed rate secured loans might be lower than variable rate loans at the moment, but that isn't always the case. Choosing between a fixed or variable loan is often about your own preference than anything else.

The average interest rate for a fixed secured personal loan in August 2026 is 10.04%.

The average interest rate for a variable secured personal loan in August 2026 is 10.81%.

How can I apply for a secured personal loan?

Step 1: Work out how much you need to borrow and what you can afford. You can use a personal loan calculator to help you. Step 2:Compare lenders and loan products. Don't forget to compare interest rates, fees, early repayment terms and eligibility criteria. Step 3: Organise and prepare the required documentation. This will make the application process quicker. Each lender will have its own criteria and requirements, but you'll likely need to have the following documents handy:

100 points of ID proving your name and that you're over 18 years old.

Proof you can pay off the loan. You may have to submit bank statements and payslips.

Details of your address and supporting bills or documents.

Proof of ownership of a valuable asset/property.

Step 4: Apply. Most lenders have their applications available online and the application should only take about 10-15 minutes.

Don't know your credit score? You can check your score and get a free copy of your credit report on Finder

Frequently asked questions about secured personal loans

The primary difference is that a secured loan requires you to put up an asset as collateral to receive the funds. An unsecured loan does not require collateral.

A secured loan isn't better or worse for your credit score than another type of loan. Applying for any loan may temporarily decrease your score, but by making regular, on-time repayments, you'll usually see a positive impact on your score in the long run.

Compared to unsecured loans, secured personal loans are typically easier to be approved for. This is because they are less risky for the lender - since they can claim your asset if you default on the loan.

If you end up defaulting on your loan, the lender can repossess and sell your asset to recoup their losses. This will also hurt your credit score.

If you're struggling to repay you should speak to your lender and see if they have a financial hardship policy.

Why compare personal loans with Finder?

Addicted to details. We know taking out a personal loan is something you'll be hooked up with for a while. That's why we put hours into research for this guide (and still do at least once a month)

Rates obsessed. Lenders come in all shapes and sizes, that's why we don't just track the big banks, but all the digi folk too. Pretty much everyone but your parents to be honest.

Cash for whatever you need. Lending rates verified from 180+ products day and night. Whether you're buying a car, rennovating your home or heck just ready to let loose with the spending - we got you.

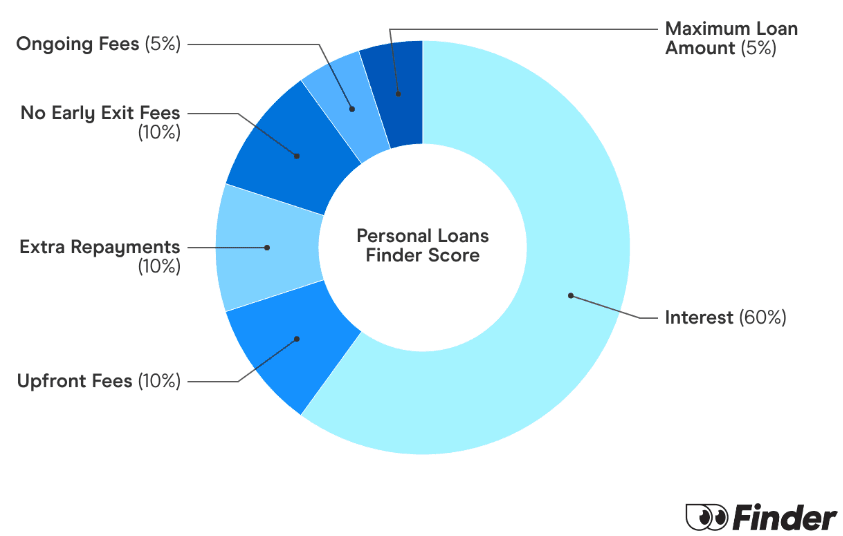

Finder Score for personal loans

To make comparing even easier we came up with the Finder Score. Interest rates, fees and features across 300+ personal loan products and 120+ lenders are all weighted and scaled to produce a score out of 10. The higher the score the better the loan - simple.

For a fair comparison, unsecured loans and secured loans are scored separately. Assumptions are made on the interest rates charged for both excellent credit and average credit customers in each segment.

Richard Whitten is Finder’s Senior Money Editor, with over eight years of experience in home loans, property, credit cards and personal finance. His insights appear in top media outlets like Yahoo Finance, Money Magazine, and the Herald Sun, and he frequently offers expert commentary on television and radio, helping Australians navigate mortgages and property ownership. Richard started his career in education and textbook publishing in South Korea. He holds multiple industry certifications, including a Certificate IV in Mortgage Broking (RG 206) and Tier 1 and Tier 2 certifications (RG 146), as well as a Bachelor of Education from the University of Sydney and a Graduate Certificate in Communications from Deakin University.

See full bio

Richard's expertise

Richard

has written

779

Finder guides across topics including:

I am a retiree. Have a bad debt of approximately Credit Card on 90,000.00 to pay off. Have a home with equity to help try and secure a loan. Can I apply for a loan, please. Thanks.

Finder

RebeccaAugust 11, 2025Finder

Hi Dennies,

With such a high debt you will probably find it difficult to get a loan, but the answer to this really depends on different lenders. Different lenders will have different credit appetites, and being able to secure your loan against your property could help you. You may find you need to pay a higher interest rate though.

As a comparison site we can’t help you apply for a loan. You can use our personal loan tables to find a loan that might suit you and then speak to the lenders directly to find out what your chances of approval are before you apply for anything. Applying for multiple loans in a short period of time will worsen your credit score.

Many lenders won’t approve borrowers with a credit score below 500, so the first thing you should do is check your credit score to see where you stand.

When you have a large expense that your savings can’t cover, a personal loan at a fixed rate from Great Southern Bank is an option worth considering. With no fees and a competitive fixed interest rate, this could be the right loan for you.

The Latitude Financial Service Personal Loan is a flexible loan with a competitive fixed interest rate, flexible repayment options and the ability to make additional repayments. Application is simple and can be completed online – find out if you're eligible.

Important information about this website

Finder is a comparison service. We do not compare every product or every provider in the market.

We make money through commercial arrangements with some of the providers on this site. Products marked 'Sponsored', 'Promoted', 'Featured' or 'Advertisement' appear as a result of a commercial arrangement.

Our editorial content, product reviews and any 'Top Pick' designations are prepared independently of these commercial arrangements.

The default order of products in our tables can be influenced by commercial arrangements. You can re-sort or filter using the controls above each table.

Some content on this site may be generated or supported by AI tools. You should verify details directly with the provider.

Finder is one of Australia's leading comparison websites. We are committed to our readers and stand by our editorial principles.

Our comparison service does not include every product or every provider in the market. Some product issuers offer their products under multiple brands or through associated companies. Where we can, we identify the underlying issuer so you can compare like with like, but you should always check with the provider directly to confirm which brand you are dealing with.

Finder is a comparison website and an intermediary. We are not a product issuer and we do not provide personal financial or credit advice. When you click a link to a product, or apply for a product through our site, you deal directly with the product issuer. We may receive a referral fee, commission or other payment from the issuer if you click through, apply or take out a product. We describe these arrangements in more detail under 'How we make money' below.

Product features, fees, terms and eligibility criteria are set by the product issuer and may change. We rely on information supplied by issuers when we present product details on our site. Before you apply for or take out any product, you should confirm the details directly with the issuer.

We earn revenue from Finder in four principal ways:

Referral fees and commissions. When you click a product link, complete an enquiry form or apply for a product through our site, we may receive a referral fee, commission or other payment from the product issuer. We may also receive payment based on the volume of leads or conversions we send to an issuer.

Sponsored placements. Products marked 'Sponsored', 'Promoted', 'Featured' or 'Advertisement' appear as a result of a commercial arrangement between Finder and the issuer. These labels always indicate a paid placement. We do not use them for editorial choices.

Display advertising. Banner advertising, newsletter advertising and similar display ads on our site are paid by advertisers.

Content sponsorship. Some articles, videos and social media posts are sponsored by an issuer and are clearly labelled as such.

Our editorial opinions, product reviews and any 'Top Pick' designations are prepared independently of these commercial arrangements. A 'Top Pick' is an editorial choice made by our writers and editors based on the criteria described on each comparison page. A 'Top Pick' is not a personal recommendation and does not mean the product is appropriate for your circumstances.

If you would like to know whether we have a commercial arrangement with a specific product issuer, please contact us.

When products are grouped in a table or list, the default order can be influenced by commercial arrangements we have with product issuers. In some categories, sponsored or featured products appear in the top positions of the table by default, and are always labelled as such.

Other factors that influence default order include price, fees and features, and (where relevant) our editorial view of the product.

You can re-sort every comparison table using the controls above the table. You can filter by product features that matter to you. The order you see after re-sorting or filtering is not influenced by commercial arrangements.

Some content on this site is generated or supported by artificial intelligence tools, including our AI-powered assistant FinderBot. AI-generated content may contain errors. Please verify important information directly with the product issuer before making a financial decision. For more information about FinderBot, see the FinderBot Terms of Use and FinderBot Privacy Collection Notice.

Please read our website terms of use and privacy policy for more information about our services and our approach to privacy.

We update our data regularly, but information can change between updates. Confirm details with the provider you're interested in before making a decision.

Our goal is to create the best possible product, and your thoughts, ideas and suggestions play a major role in helping us identify opportunities to improve.

Addicted to details. We know taking out a personal loan is something you'll be hooked up with for a while. That's why we put hours into research for this guide (and still do at least once a month)

Addicted to details. We know taking out a personal loan is something you'll be hooked up with for a while. That's why we put hours into research for this guide (and still do at least once a month)

Rates obsessed. Lenders come in all shapes and sizes, that's why we don't just track the big banks, but all the digi folk too. Pretty much everyone but your parents to be honest.

Rates obsessed. Lenders come in all shapes and sizes, that's why we don't just track the big banks, but all the digi folk too. Pretty much everyone but your parents to be honest.  Cash for whatever you need. Lending rates verified from 180+ products day and night. Whether you're buying a car, rennovating your home or heck just ready to let loose with the spending - we got you.

Cash for whatever you need. Lending rates verified from 180+ products day and night. Whether you're buying a car, rennovating your home or heck just ready to let loose with the spending - we got you.

I am a retiree. Have a bad debt of approximately Credit Card on 90,000.00 to pay off. Have a home with equity to help try and secure a loan. Can I apply for a loan, please. Thanks.

Hi Dennies,

With such a high debt you will probably find it difficult to get a loan, but the answer to this really depends on different lenders. Different lenders will have different credit appetites, and being able to secure your loan against your property could help you. You may find you need to pay a higher interest rate though.

As a comparison site we can’t help you apply for a loan. You can use our personal loan tables to find a loan that might suit you and then speak to the lenders directly to find out what your chances of approval are before you apply for anything. Applying for multiple loans in a short period of time will worsen your credit score.

Many lenders won’t approve borrowers with a credit score below 500, so the first thing you should do is check your credit score to see where you stand.

I hope this helps,

Rebecca