NAB Personal Loans

Buy a car, go on holiday or renovate your home with an unsecured personal loan.

We currently don't have that product, but here are others to consider:

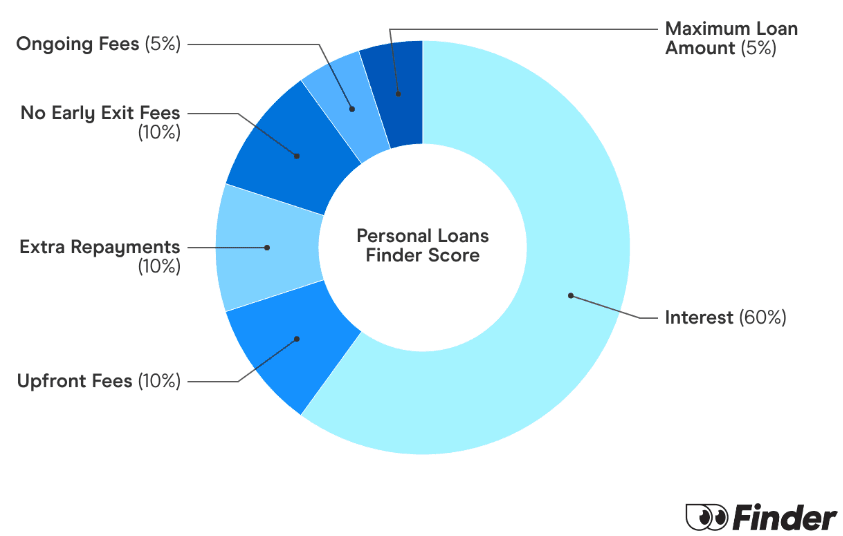

How we picked theseNeed a lower rate on your loan?

Compare now and find a better deal.

Applying online is a straightforward process. You'll need to meet general eligibility requirements including:

A marketplace personal loan with personalised interest rates.

Borrow between $5,000 and $50,000 with an unsecured personal loan from Revolut, and don't pay any fees while you repay!

When you have a large expense that your savings can’t cover, a personal loan at a fixed rate from Great Southern Bank is an option worth considering. With no fees and a competitive fixed interest rate, this could be the right loan for you.

A fixed rate secured personal loan from Latitude Financial Services with personalised interest rates.

Fin out if the Heritage Bank Standard Personal Loan is right for you.

An unsecured personal loan with interest rates tailored to your risk profile.

Benefit from a minimum interest rate in the top 5% of personal loans and pay no application or ongoing fees.

Find out how you can apply for a Jacaranda Finance personal loan.

Get a variable rate personal loan with personalised rates and same-day funding.

The Latitude Financial Service Personal Loan is a flexible loan with a competitive fixed interest rate, flexible repayment options and the ability to make additional repayments. Application is simple and can be completed online – find out if you're eligible.

I’m a self-funded retiree could I get a short-term loan of $15500 to be paid off in two months

Hi Bruce,

With a NAB personal loan specifically you usually need to take out a minimum loan term of 1 year. NAB does offer early repayment without fees though. But you’ll need to speak to the bank directly for their eligibility criteria to see if you qualify for a loan.

Thanks,

Rebecca

is it possible to borrow against a asset such as a house for a car loan plus interest rates

Hi Mike,

Yes this can be possible. To do this you refinance your current home loan (say $500,000) into a new loan worth more (say $525,000) and you can use the extra $25,000 towards a car, a holiday or renovations.

Your ability to do this depends on a few things: how much your property asset is worth, how much income you earn and whether you can afford the new higher repayments. This can be a good way to pay a lower interest rate (a home loan interest rate is lower than a car loan rate), but you will be paying it off over a longer period of time, which means you can pay more over the long term. One way to reduce the interest is to make extra repayments.

You can review some options for refinancing here.

Hope this helps!

Hi there, my partner using my NAB account to put his salary. He wants to apply for a home loan, can he use my bank account?

Hi Mary Jane,

To apply for a home loan, your boyfriend will need to verify his income. They’ll usually request evidence in the form of pay slips, bank statements and potentially tax records. Supplying your bank statements should be fine, as long as the bank can verify that the income relates to his employment and correlates to his payslips.

Hope this helps!

If I own my own business, and it’s been dormant for long enough to make my ABN need renewing, and registration again, and I have guaranteed work with it, but also my car was struck recently and I need a ute to run the business, will anyone give me finance while I’m on a pension? .

Hi Brad,

Thank you for your inquiry. We appreciate your patience.

Is this pension you’re receiving a Centrelink pension? If so, yes, there are lenders who might offer you a business loan while on a pension from Centrelink. You can find helpful tips and guidance from our Centrelink business loans page on how to apply and from which lender. When you’ve chosen a lender already, best to contact them directly so you can discuss your eligibility or options. When you are ready, you may then click on the “Go to site” button if available and you will be redirected to the lender’s website where you can proceed with the application or get in touch with their representatives for further inquiries you may have.

Hope this helps.

Cheers,

May

Will I be eligible for acceptance for the loan application? Please let me know. Thanks!

Hi John,

Thank you for getting in touch with finder.

As a friendly reminder, while we do not represent any company we feature on our pages, we can offer you general advice.

As long as you meet the eligibility criteria while applying for a NAB personal loan then you have the chance to be accepted. In this page just click “Go to Site” to get started.

The application requirements for a NAB personal loan are:

– Be at least 18 years old

– Be an Australian citizen or permanent resident of Australia

– Earn a regular income or wage

– Be able to afford the loan repayments

To apply for a NAB personal loan, make sure you have the following on hand to complete the application:

– Income and employment details

– Details of your assets, debts and liabilities

– If you’re self-employed, you’ll need a personal income tax return and your most recent notice of assessment

– If your business runs as a partnership, company or trust, you’ll need a partnership, company or trust tax return

I hope this helps.

Have a great day!

Cheers,

Jeni