Finder's low rate credit score analyses hundreds of credit cards and ranks each card based on a combination of low rates, annual fees and the number of interest-free days.

Updated in July 2026 by Finder's senior money editor, Richard Whitten.

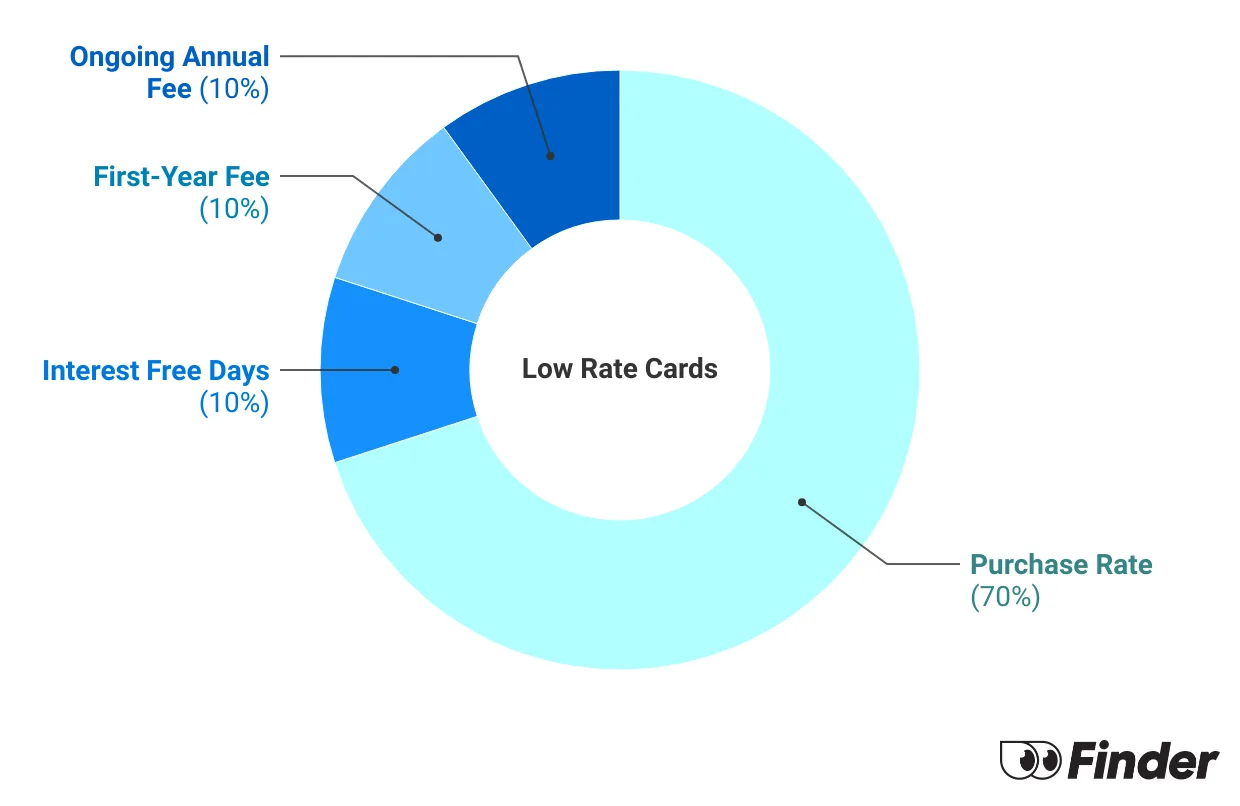

Number crunching the Finder Score

9+ Excellent - These cards offer the lowest ongoing purchase rates, high number of interest free days, and competitive introductory and ongoing annual fees.

7+ Great - Reasonable ongoing purchase rates and fees, with the potential for additional perks.

5+ Satisfactory - Low interest rates, but watch out for above average ongoing fees.

Less than 5 – Basic - These are generally cards with low interest rates, however could charge high ongoing fees.

Tell me more about the low rate credit card score

Finding the perfect low rate card is about more than just the rate (although that is the most important thing).

That's why we created the Finder Score. It's an easy, data-driven way to judge credit cards at a glance.

Every month, our insights team analyses over 250 credit cards.

We assess ten features for each card, rating each feature.

Then these ratings are combined via a weighted methodology to create a simple score out of 10.

We give different scores for different categories. So a card might get a 9 in the low rate category but an 8 in the balance transfer category.

The Finder Score is designed by our insights and editorial team. We score credit cards objectively. Commercial partnerships don't affect the scores at all.

Remember that Finder Score is just one factor to consider. Look at other aspects like fees, features, benefits and risks to make sure a product is suitable for you. Double-check details that matter to you before applying or buying.

Low rate credit cards - score weightings

Feature

Definition

Assessment

Weight

Purchase Rate

Interest rate on new purchases

Lower rates score higher

70%

Interest Free Days

Number of days with no interest charged on new purchases

Higher number of days score higher

10%

First-Year Fee

Annual fee charged in the first year of ownership

Lower fees score higher. $0 fee receives the maximum points

10%

Ongoing Annual Fee

Annual fee charged from the second year onwards

Lower fees score higher. $0 fee receives the maximum points

10%

What is a low interest rate on a credit card?

In Australia anything under 15% is a fairly low purchase rate for a credit card. Some cards have interest rates as low as 8% or as high as 22%.

Some cards even offer 0% interest rates, but those are usually introductory offers that revert to a much higher rate after 6 months.

A low rate credit card gives you a way to spend money and then pay it off over time without getting hit with high interest rate charges.

2 ways to avoid or minimise interest charges on a credit card

Pay the card off completely each month and pay no interest at all. Any credit card becomes a 0% interest rate card if you pay your spending off in full before interest charges kick in.

Get a low rate credit card and pay it off as quickly as you can. If you can't afford to pay off your card spending fully, a low or 0% rate is the next best option. This lets you pay the card spending off over time while minimising the interest charges.

Average credit card interest rates in Australia

Excluding 0% card offers, the average credit card purchase rate in Australia is 17.15%, according to Finder's database. The highest purchase rate is 27.99% and the lowest purchase rate is 8.99%.

Source:Finder's database of over 250 credit cards

Why do people use low rate credit cards?

You can't afford to pay off your card spending in full

Sometimes in life it just isn't possible to pay off your card spending each month before you start getting charged interest. Life is expensive.

If you frequently find you spend more than you earn, you may be in deeper financial trouble long term. But it can't be helped sometimes, and a low rate credit card helps you cut down those interest costs.

You need to repay card debt via a balance transfer

The second scenario where people really need a low interest rate credit card is when their existing card spending has gotten them into trouble. That's a where a balance transfer can help.

A good balance transfer credit card offer gives you 0% or very low interest charges for 24 months (or more) on your existing credit card debt. You move the unpaid balance from the old card onto the new one, cancel the old one and then start paying it back.

What about 0% interest rate cards?

There are also cards that offer a 0% purchase interest rate. Some cards give you 0% for 6 months, others charge a monthly fee instead interest.

These cards are useful if you have large purchases, like a holiday, wedding or renovation coming up. You can spend now and pay it off over time without interest charges.

You just need to watch out for:

The revert rate. Some credit cards give you 0% for 6 months. But on month 7 the rate jumps up to 20%. If you haven't paid off your spending, you're suddenly looking at big interest charges.

The fees. Some of these cards never charge interest but do charge an ongoing fee. This fee could be small but still end up costing more than interest charges over a few months.

Pros and cons of low rate credit cards

Pros

You pay less interest. Low rate credit cards can be a cheaper option as you pay less interest on purchases, which will help you save money and avoid falling into unmanageable debt.

You save on fees. Many low interest rate credit cards also have lower annual fees, which helps you save even more money.

You can get promotional offers. Low interest rate credit cards sometimes offer 0% promotions on purchases and/or balance transfers, allowing you to avoid interest altogether for an introductory period.

Cons

You get fewer rewards. Low rate credit cards tend to have fewer or no rewards or perks, compared to higher rate, premium rewards and frequent flyer cards.

You get fewer extra features. Lower rates generally mean fewer extra features, unlike platinum cards which often come with complimentary insurance options, cashbacks, concierge services and more.

Watch out for revert rates. If your card offers 0% interest on purchases for a promotional period, it will revert to a higher purchase rate that could be up to 26.99% p.a.

How much can you save with a lower rate?

Most Australians pay their credit cards in full each month. This means they don't get charged any interest on their spending.

But Australians with an unpaid credit card balance have on average $1,655. Let's look at how much interest you end up paying on this balance with different interest rates (assuming you take 12 months to pay off the card:

Balance

Interest rate

Monthly payments (over 12 months)

Total interest charged

$1,655

9.0%

$144.73

$81.79

$1,655

12.0%

$147.04

$109.54

$1,655

15.0%

$149.38

$137.53

$1,655

17.0%

$150.94

$156.33

$1,655

20.0%

$153.31

$184.72

The difference between a 20% interest rate and a 9% rate is over $100 in interest over 12 months.

How to compare low interest rate credit cards

With so many competitive low interest rate credit cards on the market, here are some of the features that can help you narrow down your options:

Compare interest rates. The lower the interest rate the better. Below 15% is good, below 10% is very good. If a card offers a 0% promotional rate, check how long it lasts and remember that it will be much higher after this period ends. Some 0% cards jump to 20% after 6 months!

Look at the card's annual fee. Low rate cards have annual fees of around $59 on the lower end but can go as high as $200. The lower the better, but cards with higher fees may offer useful features and perks. There are also some cards that offer $0 annual fee for the first year or for life.

Factor in other fees. If you use your card for foreign currency or overseas purchases (including online), you will usually be charged a foreign transaction fee of around 2-3.5%. But certain credit cards are more tailored to international use and offer 0% foreign transactions fees.

Compare perks and features. Some low rate cards also come with cashback offers, although you'll usually need to meet a certain spend requirement to get the money back. Some low rate cards offer you complimentary travel insurance and purchase cover.

What perks and benefits can you get with these credit cards?

Let's be clear: low rate credit cards are not the best cards for points, perks and other benefits. Those cards have higher rates and higher annual fees.

But the best low rate cards often come with decent benefits at the price point, such as:

Cashbacks. Quite a few of the top scoring low rate cards in Finder's database offer some form of cashback on your spending. Cashbacks usually give you, say, 10% back on eligible spending, capped at a certain amount. This can save you a few hundred dollars.

0% balance transfers. Low rate cards often have some of the best 0% balance transfer deals. Just keep in mind that a balance transfer customer needs to focus on paying off existing debt rather than adding to it with more spending. So the low purchase rate doesn't matter as much because you should be paying the balance transfer off.

0% foreign transaction fees. A few low rate cards offer 0% foreign transaction/international transaction fees, which saves you money when travelling or shopping overseas.

Complimentary insurance cover. While low rate cards are far less likely to offer complimentary travel insurance, some cards do offer this, or other types of cover like purchase protection insurance.

The bottom line

If you often carry over a balance from one month to the next, a low interest credit card could help you save on interest charges. While there is no "best" low rate care, the mix of credit cards available in Australia means you can compare credit card offers and features to help find a card that you want.

2026 Finder Awards for Low Rate Credit Cards

Each year the Finder Credit Card Awards recognises Australia's top credit cards, with expert analysis of rates, fees and offers based on 12 months' worth of data. Here are the top performing low rate credit cards.

G&C Mutual Bank's Low Rate Visa Credit Card is the winner of this year's low rate credit card award. It has, you guessed it, a very low interest rate. Plus a low annual fee.

G&C Mutual Bank's Low Rate Visa Credit Card is the winner of this year's low rate credit card award. It has, you guessed it, a very low interest rate. Plus a low annual fee.

MOVE Bank's Low Rate Credit Card scored well this year with one of the market's lowest credit card purchase rates.

Frequently asked questions

The cheapest card will depend on how you use it. If you pay off your balance every month, a $0 annual fee credit card would likely be the cheapest option.

If you regularly carry a balance from month to month, the cheapest credit card will have a low interest rate and a modest annual fee (less than $100). There aren't many cards on the market that offer both a $0 annual fee and a low rate, but using the table above you can find what you consider to be a cheap credit card.

There is no one "best" low interest rate credit card in Australia. With so many cards on the market, a card's individual features have an impact on how well it suits your circumstances. So the card that's right for you may not be right for someone else. Comparing low interest rate credit cards based on the features you're looking for will help you find a card for your individual needs.

A low rate credit card can be very useful if you carry a balance (can't repay all your card spending in one month) as it cuts down your interest charges. It's also useful if you need to make a large one-off purchase and pay it off over time.

These cards are less useful if you're a big spender who can afford to pay your card spending off in full. You may get more value out of a reward or frequent flyer credit card.

And if you only use the card occasionally and always pay it off, you might save money with a no annual fee credit card.

Low rate and low fee credit cards can both save you money but in different ways. A low interest rate credit card reduces your interest charges if you can't repay your card balance fully each statement period.

A low fee credit card saves you money on fees. They are more suited to customers who pay off the card in full and don't need to worry about interest charges.

Credit card interest rates are usually advertised by the annual rate that applies to the account, shown as "per annum" or p.a. However, interest on your account balance is typically calculated daily and then charged monthly on the statement due date. This means that for every day that you don't make a payment, the interest charges will build up (or compound).

This depends on the credit card and any applicable balance transfer offers. If the card allows balance transfers, it may come with a 0% interest rate for a promotional period before reverting to a standard rate.

Some low interest rate cards apply the standard purchase rate to balance transfers after the introductory period while others apply the cash advance rate, which can be as high as 29.99% p.a. The average standard credit card interest rate is currently 20.99% according to Finder analysis of Reserve Bank of Australia data.

There isn't a single "cheapest" credit card option because everyone uses credit cards differently. There are other costs to consider beyond the purchase rate, such as annual fees and interest rates for cash advances or balance transfers. On the flip side, some people might find cards with high rates and fees "cheap" because of all the complimentary extras.

When you're looking to find a credit card, consider all of the potential costs based on how you plan to use the account. That way, you'll be able to find one with rates and fees that are affordable for you.

Most frequent flyer and rewards credit cards have higher interest rates and fees than low rate cards. But there is a small selection of low rate credit cards that offer points on eligible spending, including the Coles Low Rate Mastercard and Queensland Country Bank Visa My Rewards Credit Card. These cards typically earn fewer points per $1 spent, so it's important to consider whether rewards or a low rate will offer you more value before choosing a card.

If your credit card offers 55 interest-free days and you make a purchase on the first day of your statement period, you'll have 55 days to pay it back before you're charged interest. If you make that purchase on day 15 of your statement period, you'll have 40 interest-free days, and so on.

This only applies if you pay the amount required by the provider by the due date listed on your statement. See Finder's guide to interest-free days for full details.

Richard Whitten is Finder’s Senior Money Editor, with over eight years of experience in home loans, property, credit cards and personal finance. His insights appear in top media outlets like Yahoo Finance, Money Magazine, and the Herald Sun, and he frequently offers expert commentary on television and radio, helping Australians navigate mortgages and property ownership. Richard started his career in education and textbook publishing in South Korea. He holds multiple industry certifications, including a Certificate IV in Mortgage Broking (RG 206) and Tier 1 and Tier 2 certifications (RG 146), as well as a Bachelor of Education from the University of Sydney and a Graduate Certificate in Communications from Deakin University.

See full bio

Richard's expertise

Richard

has written

759

Finder guides across topics including:

Hi, I’m worried that by applying for credit cards will reduce my score ,I am on Centrelink and feel maybe there is no point trying as I always get rejected.i only wish to have a credit card as it’s getting harder in this economy and would like to have one as a bit of security incase I need a bit extra .with my score is there any point trying or should I stop applying and accept that my income is just never going to be accepted.please help

Finder

AngusFebruary 6, 2025Finder

Hi Billie-Jo, I’d recommend checking our guide to credit cards for people on Centrelink for more on this topic. But you’re right that making multiple unsuccessful credit card applications can reduce your credit score. Realistically, if your Centrelink payment is largely used for basic living expenses (rent+food+transport) then you’re unlikely to be approved for a credit card. It’s also worth remembering that while a credit card can be a useful emergency option, you’ll have to pay the annual fee up front. Hope this helps.

JamesOctober 26, 2023

hi i’m trying to find a best credit card that suits me , first time holder I never hold one in my life .

Finder

AmyOctober 27, 2023Finder

Hi James,

It’s helpful to consider what’s important to you when choosing a credit card. For example, a low rate credit card can help you save on interest charges if you want to pay off spending over time. A card with low fees or no annual fee could also help keep account costs down. Rewards and extras like complimentary insurance are also features you may want to consider. Finder’s guide to credit cards has more details about the different types of cards and what else to consider. I hope this helps.

JadeSeptember 3, 2019

Are there any credit cards available for people on disability pension Centrelink please?

Finder

JeniSeptember 4, 2019Finder

Hi Jade,

Thank you for getting in touch with Finder.

You can start comparing credit cards for pensioners and retirees. I suggest that you contact your chosen bank or credit card issuer before submitting your online application to know your chances of getting approved.

Please make sure though to read the eligibility criteria, features, and details of the card, as well as the relevant PDS/ T&Cs of the card before making a decision and consider whether the product is right for you. When you are ready, press the ‘Go to site’ button to apply.

I hope this helps.

Thank you and have a wonderful day!

Cheers,

Jeni

sueFebruary 24, 2019

Am I better off to get a personal loan to pay credit cards off and get extra money for travel /

would like to consolidate credit card debt and have some money for travel

Finder

JohnFebruary 25, 2019Finder

Hi Sue,

Thank you for reaching out to Finder.

Depending on how much you would require to consolidate your debt as well as have a bit of extra for travel, a personal loan would be able to help you achieve this. You would not be able to have the extra cash when you use a different method in consolidating your debt. You may refer to our list of personal loan. Kindly review and compare your options on the table displaying the available providers. Once you have chosen a particular provider, you may then click on the “Go to site” button and you will be redirected to the provider’s website where you can proceed with the application or get in touch with their representatives for further inquiries you may have.

Before applying, please ensure that you meet all the eligibility criteria and read through the details of the needed requirements as well as the relevant Product Disclosure Statements/Terms and Conditions when comparing your options before deciding on whether it is right for you. Hope this helps!

Cheers,

Reggie

willardDecember 20, 2018

what card would be best for people on s.s?

Finder

JohnDecember 20, 2018Finder

Hi Willard,

Thank you for reaching out to finder.

While we do not provide specific product recommendations, we can help guide you through the process of comparing options. You may want to check our page on “Credit cards for retired and pensioner applicants”. The page will also advise you of what documents to provide during the application process. Please click here to be routed to that page. Hope this helps!

Most credit cards offer interest-free days on purchases – here's how they actually work.

Important information about this website

Finder makes money from featured partners, but editorial opinions are our own.

Finder is one of Australia's leading comparison websites. We are committed to our readers and stand by our editorial principles.

We try to take an open and transparent approach and provide a broad-based comparison service. However, you should be aware that while we are an independently owned service, our comparison service does not include all providers or all products available in the market.

Some product issuers may provide products or offer services through multiple brands, associated companies or different labeling arrangements. This can make it difficult for consumers to compare alternatives or identify the companies behind the products. However, we aim to provide information to enable consumers to understand these issues.

We make money by featuring products on our site. Compensation received from the providers featured on our site can influence which products we write about as well as where and how products appear on our page, but the order or placement of these products does not influence our assessment or opinions of them, nor is it an endorsement or recommendation for them.

Products marked as 'Top Pick', 'Promoted' or 'Advertisement' are prominently displayed either as a result of a commercial advertising arrangement or to highlight a particular product, provider or feature. Finder may receive remuneration from the Provider if you click on the related link, purchase or enquire about the product. Finder's decision to show a 'promoted' product is neither a recommendation that the product is appropriate for you nor an indication that the product is the best in its category. We encourage you to use the tools and information we provide to compare your options.

Where our site links to particular products or displays 'Go to site' buttons, we may receive a commission, referral fee or payment when you click on those buttons or apply for a product.

When products are grouped in a table or list, the order in which they are initially sorted may be influenced by a range of factors including price, fees and discounts; commercial partnerships; product features; and brand popularity. We provide tools so you can sort and filter these lists to highlight features that matter to you.

Please read our website terms of use and privacy policy for more information about our services and our approach to privacy.

We update our data regularly, but information can change between updates. Confirm details with the provider you're interested in before making a decision.

Hi, I’m worried that by applying for credit cards will reduce my score ,I am on Centrelink and feel maybe there is no point trying as I always get rejected.i only wish to have a credit card as it’s getting harder in this economy and would like to have one as a bit of security incase I need a bit extra .with my score is there any point trying or should I stop applying and accept that my income is just never going to be accepted.please help

Hi Billie-Jo, I’d recommend checking our guide to credit cards for people on Centrelink for more on this topic. But you’re right that making multiple unsuccessful credit card applications can reduce your credit score. Realistically, if your Centrelink payment is largely used for basic living expenses (rent+food+transport) then you’re unlikely to be approved for a credit card. It’s also worth remembering that while a credit card can be a useful emergency option, you’ll have to pay the annual fee up front. Hope this helps.

hi i’m trying to find a best credit card that suits me , first time holder I never hold one in my life .

Hi James,

It’s helpful to consider what’s important to you when choosing a credit card. For example, a low rate credit card can help you save on interest charges if you want to pay off spending over time. A card with low fees or no annual fee could also help keep account costs down. Rewards and extras like complimentary insurance are also features you may want to consider. Finder’s guide to credit cards has more details about the different types of cards and what else to consider. I hope this helps.

Are there any credit cards available for people on disability pension Centrelink please?

Hi Jade,

Thank you for getting in touch with Finder.

You can start comparing credit cards for pensioners and retirees. I suggest that you contact your chosen bank or credit card issuer before submitting your online application to know your chances of getting approved.

Please make sure though to read the eligibility criteria, features, and details of the card, as well as the relevant PDS/ T&Cs of the card before making a decision and consider whether the product is right for you. When you are ready, press the ‘Go to site’ button to apply.

I hope this helps.

Thank you and have a wonderful day!

Cheers,

Jeni

Am I better off to get a personal loan to pay credit cards off and get extra money for travel /

would like to consolidate credit card debt and have some money for travel

Hi Sue,

Thank you for reaching out to Finder.

Depending on how much you would require to consolidate your debt as well as have a bit of extra for travel, a personal loan would be able to help you achieve this. You would not be able to have the extra cash when you use a different method in consolidating your debt. You may refer to our list of personal loan. Kindly review and compare your options on the table displaying the available providers. Once you have chosen a particular provider, you may then click on the “Go to site” button and you will be redirected to the provider’s website where you can proceed with the application or get in touch with their representatives for further inquiries you may have.

Before applying, please ensure that you meet all the eligibility criteria and read through the details of the needed requirements as well as the relevant Product Disclosure Statements/Terms and Conditions when comparing your options before deciding on whether it is right for you. Hope this helps!

Cheers,

Reggie

what card would be best for people on s.s?

Hi Willard,

Thank you for reaching out to finder.

While we do not provide specific product recommendations, we can help guide you through the process of comparing options. You may want to check our page on “Credit cards for retired and pensioner applicants”. The page will also advise you of what documents to provide during the application process. Please click here to be routed to that page. Hope this helps!

Cheers,

Reggie