The crème de la crème of personal loans. These products offer the lowest cost loans accompanied by the best features.

7+

Great

Slightly higher in cost and fewer features, but these products are still competitive.

5+

Standard

Typically offering above average rates and possibly lacking in the features department.

0+

Basic

The least competitive in terms of both cost and features.

Personal loan interest rates tend to be peresonalised. That means the rate you'll get depends on factors like your credit score, income, liabilities and other factors. The lowest personal loan rates are for borrowers with excellent credit scores taking out secured personal loans.

But whatever your personal situation is, there are ways to get a lower rate and save money on a personal loan.

What's a low personal loan interest rate?

Lowest unsecured personal loan rate: Harmoney Unsecured Personal Loan: 5.76% (comparison rate 6.55%).

Lowest secured personal loan rate: MoneyPlace Secured Personal Loan: 5.67% (comparison rate 7.14%).

Average unsecured personal loan rate in Finder's database: 10.32% p.a.

The average Australian with a personal loan borrows $8,622 with a 4 year term according to Finder's data.

Source:Finder's rate database

How much can you save with a low rate personal loan?

While fees are important too, it's the interest rate that has the biggest impact on most personal loans.

A lower rate means lower monthly repayments and less interest paid over the life of the loan.

Let's compare loans to see how a lower interest rate would impact the cost of the loan:

Loan amount

Loan term

Interest rate (p.a.)

Monthly repayments

Total loan cost*

$15,000

1 year

14.00%

$1,346

$16,162

$15,000

1 year

19.00%

$1,382

$16,588

$15,000

1 year

27.00%

$1,440

$17,283

*For this simple example we've ignored loan fees, but it's important to factor in any upfront and ongoing fees.

Our expert says: Here are 3 tips to find the best loan

"1. Check your credit score before you apply. A higher score usually unlocks better rates. 2. Compare rates from multiple lenders to make sure you're getting a more competitive offer. 3. Choose your loan length carefully: too long and you'll pay more interest, too short and your monthly repayments will be too high (use a calculator to check)."

Not every borrower will qualify the absolute lowest personal loan interest rate on offer, but there are things you can do to get a lower rate. Here are our six tips:

1. Improve your credit score

The best thing you can do to get a lower interest rate is improve your credit score. This means making regular payments on existing debts and making sure you don't have any missed payments or defaults. You could also lower your credit card limit and make sure you only have one card.

2. Offer security

Having an asset to act as collateral (like a car or house) can get you a lower rate. If you have an asset you can and are willing to secure, it's worth checking if you can use it even when applying for a loan advertised as unsecured. Just make sure you can comfortably afford the repayments so you don't risk losing that asset.

3. Borrow less

A smaller loan amount makes you a less risky borrower in a lender's eyes. And it may get you a slightly lower personal loan rate. Keep in mind that some lenders might reject a small loan application if the loan is under its minimum loan amount.

4. Compare your options

Don't just go to your bank and don't apply with the first lender you see. Compare personal loan rates, fees and features from multiple lenders. The market is competitive and you might find a great deal from an online lender. But remember that the minimum rate advertised isn't necessarily the one you'll end up with.

5. Meet all the lending criteria

Before you apply for a loan, check the loan's terms and conditions carefully. Make sure you as a borrower meet the lender's requirements. Otherwise you'll get rejected, or end up on a higher rate.

6. Negotiate

You can sometimes ask the lender for a lower interest rate. If you find a lower rate elsewhere you could ask them to match, for example. This works if you already have a personal loan too.

Borrowers who already have personal loans can get lower rates too

The above point about negotiating with your lender applies to people who already have loans too. Let's say you've significantly improved your credit score since you took out the loan. Tell your lender and see if they can give you a lower rate.

Like we've already said, personal loans use risk-based pricing. The interest rate you're given is determined by your credit score, your income, your outstanding debts and the type of loan you're applying for.

This is why you'll see an interest rate range advertised, like:

Interest rate: 8.49% p.a to 27.9% p.a.

The lowest possible rate you can get here is 8.49% p.a. That's if you have an excellent credit score and meet the lender's criteria. But if your credit score isn't so good, your rate could be as high as 27.9% p.a.

Before applying for any personal loan you should know what your credit score is. You can check your credit score for free through Finder in just minutes.

The type of personal loan you're looking for has an impact on the rate you can get.

Secured loans. If you have an asset, usually a car or property, you can offer that as security for your lender. This means you'll get a lower rate compared to an unsecured personal loan.

Risk-based personal loans (if you have excellent credit). Most lenders use risk-based pricing, meaning your rate is lower if you have a good or excellent credit score and meet the lender's criteria. If you have a strong credit score then a risk-based personal loan could offer a lower rate.

Loans from online lenders. Online lenders have lower operating costs and often boast some of the market's lowest personal loan rates. But these days even the big banks offer quite competitive rates. That's why comparing all your options is so important.

Can I still get a competitive rate with an unsecured loan?

If you don't have anything to offer as security you can still find unsecured personal loans with low interest rates. Often, there's only a couple of percentage points between a lender's lowest secured rate and lowest unsecured rate. Sometimes less than that.

How do I compare to find a low interest personal loan?

A low rate personal loan can become expensive if it has high fees and a long loan term. It's also pointless if it's not the right loan for your needs.

These are the key things to look at in your comparison to finding the right loan:

Interest rate. A solid start to finding that low rate personal loan is to look for the lowest advertised rate. Remember that this normally advertises the lowest rate the lender offers, so if you don't have a perfect credit score you will probably be offered a higher rate. Non-risk based loans do exist though, where everyone who is approved receives the same interest rate regardless of credit score.

Comparison rate. The comparison rate gives you an idea of how expensive a loan is when you include monthly and establishment fees. This is an example based on a 'typical' loan, so it won't be exactly the same for you however it's still the easiest way to see how expensive the loan is at a glance.

Loan features. If a personal loan lets you make extra repayments and allows you to pay off the loan early, you can save money by getting out of debt faster. Some loans may have a cap on how many extra repayment you can make in a year. Some may not allow it at all.

Fees. Personal loan fees can be hefty. There's usually an application fee of more than $100, or a fee charged as a percentage of the loan amount. And there's often a small monthly fee too. Add up the cost of fees before you apply for a loan.

Loan terms. If your loan has a long term (say, 5 years) your monthly repayments will be smaller. But you'll pay much more interest over 5 years. A shorter loan term works out cheaper because you'll pay less interest. However, your monthly repayments will be higher. So you need to find a balance between a short and long loan term.

Loan purpose. Not every borrower needs a lump sum of cash right now. There are other loan types that might work out cheaper for you, even with a higher rate. If you have a series of expenses to cover over time then a line of credit might work better. Or a personal overdraft.

Frequently asked questions about low interest personal loans

When comparing lenders it's important to check the minimum loan amount before applying.

Most personal loan lenders in Finder's database have minimum loan requirements of between $2,000 and $5,000. If a lender says its minimum loan amount is $3,000, then it won't lend you $2,000.

You can borrow very small amounts of money, but you'll have to look at a or other short term finance options. These smaller loans don't charge interest in some cases but charge hefty fees instead - up to 20% of the loan amount plus a 4% monthly fee.

This makes a small loan a very expensive prospect.

Any debt you can pay off faster saves you money. But another financial rule of thumb is to prioritise paying off high interest debts first.

If you have a small low interest personal loan, a home loan and a big credit card debt you could approach it like this:

Keep making the minimum repayments on all your debts, obviously.

Prioritise putting any extra money you have into paying off the credit card debt as fast as possible. It has the highest rate.

Once that's sorted out, concentrate on the personal loan debt, which has a higher rate than your mortgage.

Keep in mind this is simply a general example and is not personal financial advice. Your own situation may be different.

Online lenders often have the lowest interest rates on personal loans. But the stereotype of the big banks being uncompetitive with rates just isn't always true.

Looking at Finder's database, even some of the Big Four banks have personal loans with much lower rates than average. So don't count them out completely when comparing your options.

And if you're already a customer with a big bank, you might find personal loan approval is fast and easy. And if you're already using the bank's app, you've got all your financial products on your phone in one place. The convenience might be worth a slightly higher rate.

Self-employed borrowers often choose low doc personal loans because they don't have evidence of consistent income to qualify for a standard loan.

As you'd expect these loans have higher rates. But if you have alternative proof of income (business tax returns, financial statements), your business is doing well and you have a good credit score you could qualify for a standard personal loan with a low rate.

Peer to peer lenders are online platforms that connect investors with money to individual borrowers. You request a loan and the platform checks your credit, processes the application and connects you to the funds.

When it works well, you can get a fast low rate loan approved without too much trouble.

But if you're borrowing a lot and your credit score isn't great, your rate could rise a lot more. And it might end up being higher or comparable to other lenders.

You might not be able to borrow as much via peer to peer lenders, and you might not get loan features like a redraw facility.

Why compare personal loans with Finder?

Addicted to details - we know taking out a personal loan is something you'll be hooked up with for a while. That's why we put hours into research for this guide (and still do at least once a month).

Rates obsessed - lenders come in all shapes and sizes, that's why we don't just track the big banks, but all the digi folk too. Pretty much everyone but your parents to be honest.

Cash for whatever you need - Lending rates verified from 180+ products day and night. Whether you're buying a car, rennovating your home or heck just ready to let loose with the spending - we got you.

Richard Whitten is Finder’s Senior Money Editor, with over eight years of experience in home loans, property, credit cards and personal finance. His insights appear in top media outlets like Yahoo Finance, Money Magazine, and the Herald Sun, and he frequently offers expert commentary on television and radio, helping Australians navigate mortgages and property ownership. Richard started his career in education and textbook publishing in South Korea. He holds multiple industry certifications, including a Certificate IV in Mortgage Broking (RG 206) and Tier 1 and Tier 2 certifications (RG 146), as well as a Bachelor of Education from the University of Sydney and a Graduate Certificate in Communications from Deakin University.

See full bio

Richard's expertise

Richard

has written

758

Finder guides across topics including:

I see you’re interested in getting a personal loan. You can use our comparison table to help you find the lender that suits you. When you are ready, press the ‘Go to site’ button to apply. As a friendly reminder, review the eligibility criteria of the loan before applying to increase your chances of approval. Read up on the terms and conditions and product disclosure statement and contact the bank should you need any clarifications about the policy.

Hope this helps!

Best,

Nikki

RebFebruary 6, 2019

Hi! When applying for a personal loan via this site, do the lenders only look at your credit score and report on finder as there are many different credit score sites that display different credit scores.

Thank you!

Finder

JoshuaFebruary 12, 2019Finder

Hi Reb,

Thanks for getting in touch with finder. I hope all is well with you. :)

When you apply for a personal loan featured on our website, the lenders have their own way of assessing your eligibility. The credit score you get from our website is generated by Experian. There are a lot of lenders who use Experian, but there are also those that use other credit reporting bureaus.

In most cases, there is a small discrepancy between scores that you get from different bureaus. If the discrepancy is huge, then there could be an error that you need to fix.

I hope this helps. Should you have further questions, please don’t hesitate to reach us out again.

Have a wonderful day!

Cheers,

Joshua

LeeJanuary 13, 2019

Can I go for a loan?

Finder

JoshuaJanuary 14, 2019Finder

Hi Lee,

Thanks for getting in touch with finder. I hope all is well with you. :)

Yes, you can go for a loan as long as you meet the eligibility requirements of your chosen lender. You can compare your options above by using our comparison table. You can compare based on interest rate, loan term, and fees, to name a few. Once you found the right one for you, click on the “Go to site” green button to learn more or initiate your application.

Please make sure that you’ve read the relevant T&Cs or PDS of the loan products before making a decision. Moreover, check the eligibility requirements as well and consider whether the product is right for you.

I hope this helps. Should you have further questions, please don’t hesitate to reach us out again.

Have a wonderful day!

Cheers,

Joshua

WilfredoOctober 12, 2018

hi, I am looking for a medical dental done overseas and pay a small personal loan and a credit card ,probably make extra repayments so I can pay back the sooner I can I need to borrow 25000.

Finder

JohnOctober 12, 2018Finder

Hi Wilfredo,

Thank you for leaving a question.

This page gives you a comprehensive list of lenders that you could reach out to if you need to borrow money. Kindly review and compare your options on the table displaying the available providers. Once you have chosen a particular provider, you may then click on the “Go to site” button and you will be redirected to the provider’s website where you can proceed with the application or get in touch with their representatives for further inquiries you may have.

Before applying, please ensure that you meet all the eligibility criteria and read through the details of the needed requirements as well as the relevant Product Disclosure Statements/Terms and Conditions when comparing your options before making a decision on whether it is right for you. Hope this helps!

Cheers,

Reggie

PaulMay 3, 2018

I want to buy land in Thailand with my Thai wife we are looking for $45000 can you suggest the best loan for this.

ArnoldMay 5, 2018

Hi Paul,

Thanks for your inquiry

Generally, Australian banks can’t take a foreign property as security for a home loan. However, they can help you fund your future investment plans if you have an existing property with enough equity. There are also a number of non-Australian owned international banks that may be able to help you with finance. A mortgage broker may be able to help you with this by getting touch with the branch themselves.

One important thing to note is that some countries limit you to borrowing 80% of the property value or Loan to Value Ratio (LVR).

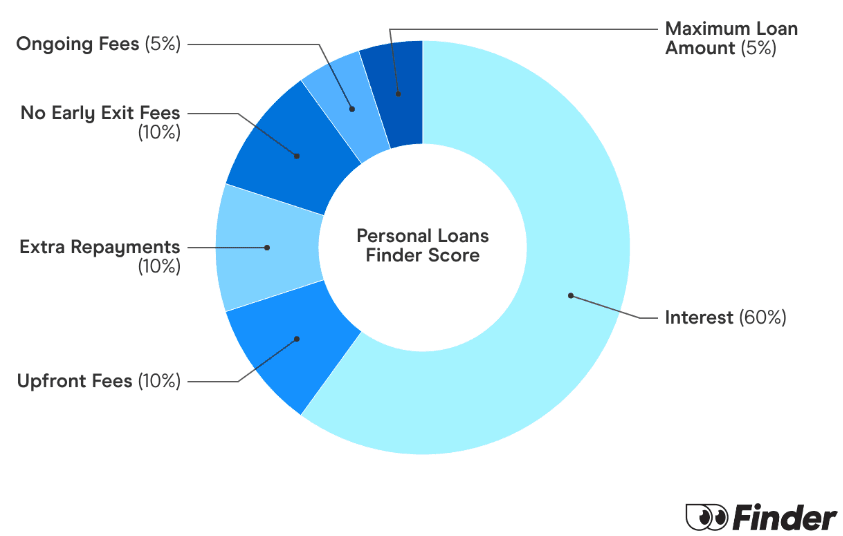

With a high Finder Score of 9.2, Pepper Money Unsecured Fixed Rate Personal Loan ranks among the top 13% in our database. Its competitive minimum interest rate from 5.95% is in the top 10% of the lowest rates available.

Temporary Australian residents may be eligible to apply for personal loans, depending on the visa they hold.

Important information about this website

Finder makes money from featured partners, but editorial opinions are our own.

Finder is one of Australia's leading comparison websites. We are committed to our readers and stand by our editorial principles.

We try to take an open and transparent approach and provide a broad-based comparison service. However, you should be aware that while we are an independently owned service, our comparison service does not include all providers or all products available in the market.

Some product issuers may provide products or offer services through multiple brands, associated companies or different labeling arrangements. This can make it difficult for consumers to compare alternatives or identify the companies behind the products. However, we aim to provide information to enable consumers to understand these issues.

We make money by featuring products on our site. Compensation received from the providers featured on our site can influence which products we write about as well as where and how products appear on our page, but the order or placement of these products does not influence our assessment or opinions of them, nor is it an endorsement or recommendation for them.

Products marked as 'Top Pick', 'Promoted' or 'Advertisement' are prominently displayed either as a result of a commercial advertising arrangement or to highlight a particular product, provider or feature. Finder may receive remuneration from the Provider if you click on the related link, purchase or enquire about the product. Finder's decision to show a 'promoted' product is neither a recommendation that the product is appropriate for you nor an indication that the product is the best in its category. We encourage you to use the tools and information we provide to compare your options.

Where our site links to particular products or displays 'Go to site' buttons, we may receive a commission, referral fee or payment when you click on those buttons or apply for a product.

When products are grouped in a table or list, the order in which they are initially sorted may be influenced by a range of factors including price, fees and discounts; commercial partnerships; product features; and brand popularity. We provide tools so you can sort and filter these lists to highlight features that matter to you.

Please read our website terms of use and privacy policy for more information about our services and our approach to privacy.

We update our data regularly, but information can change between updates. Confirm details with the provider you're interested in before making a decision.

How likely would you be to recommend Finder to a friend or colleague?

0

1

2

3

4

5

6

7

8

9

10

Very UnlikelyExtremely Likely

Required

Thank you for your feedback.

Our goal is to create the best possible product, and your thoughts, ideas and suggestions play a major role in helping us identify opportunities to improve.

Addicted to details - we know taking out a personal loan is something you'll be hooked up with for a while. That's why we put hours into research for this guide (and still do at least once a month).

Addicted to details - we know taking out a personal loan is something you'll be hooked up with for a while. That's why we put hours into research for this guide (and still do at least once a month).

Rates obsessed - lenders come in all shapes and sizes, that's why we don't just track the big banks, but all the digi folk too. Pretty much everyone but your parents to be honest.

Rates obsessed - lenders come in all shapes and sizes, that's why we don't just track the big banks, but all the digi folk too. Pretty much everyone but your parents to be honest.

Cash for whatever you need - Lending rates verified from 180+ products day and night. Whether you're buying a car, rennovating your home or heck just ready to let loose with the spending - we got you.

Cash for whatever you need - Lending rates verified from 180+ products day and night. Whether you're buying a car, rennovating your home or heck just ready to let loose with the spending - we got you.

Personal Loan

Hi Anwar,

Thanks for reaching out to Finder!

I see you’re interested in getting a personal loan. You can use our comparison table to help you find the lender that suits you. When you are ready, press the ‘Go to site’ button to apply. As a friendly reminder, review the eligibility criteria of the loan before applying to increase your chances of approval. Read up on the terms and conditions and product disclosure statement and contact the bank should you need any clarifications about the policy.

Hope this helps!

Best,

Nikki

Hi! When applying for a personal loan via this site, do the lenders only look at your credit score and report on finder as there are many different credit score sites that display different credit scores.

Thank you!

Hi Reb,

Thanks for getting in touch with finder. I hope all is well with you. :)

When you apply for a personal loan featured on our website, the lenders have their own way of assessing your eligibility. The credit score you get from our website is generated by Experian. There are a lot of lenders who use Experian, but there are also those that use other credit reporting bureaus.

In most cases, there is a small discrepancy between scores that you get from different bureaus. If the discrepancy is huge, then there could be an error that you need to fix.

I hope this helps. Should you have further questions, please don’t hesitate to reach us out again.

Have a wonderful day!

Cheers,

Joshua

Can I go for a loan?

Hi Lee,

Thanks for getting in touch with finder. I hope all is well with you. :)

Yes, you can go for a loan as long as you meet the eligibility requirements of your chosen lender. You can compare your options above by using our comparison table. You can compare based on interest rate, loan term, and fees, to name a few. Once you found the right one for you, click on the “Go to site” green button to learn more or initiate your application.

Please make sure that you’ve read the relevant T&Cs or PDS of the loan products before making a decision. Moreover, check the eligibility requirements as well and consider whether the product is right for you.

I hope this helps. Should you have further questions, please don’t hesitate to reach us out again.

Have a wonderful day!

Cheers,

Joshua

hi, I am looking for a medical dental done overseas and pay a small personal loan and a credit card ,probably make extra repayments so I can pay back the sooner I can I need to borrow 25000.

Hi Wilfredo,

Thank you for leaving a question.

This page gives you a comprehensive list of lenders that you could reach out to if you need to borrow money. Kindly review and compare your options on the table displaying the available providers. Once you have chosen a particular provider, you may then click on the “Go to site” button and you will be redirected to the provider’s website where you can proceed with the application or get in touch with their representatives for further inquiries you may have.

Before applying, please ensure that you meet all the eligibility criteria and read through the details of the needed requirements as well as the relevant Product Disclosure Statements/Terms and Conditions when comparing your options before making a decision on whether it is right for you. Hope this helps!

Cheers,

Reggie

I want to buy land in Thailand with my Thai wife we are looking for $45000 can you suggest the best loan for this.

Hi Paul,

Thanks for your inquiry

Generally, Australian banks can’t take a foreign property as security for a home loan. However, they can help you fund your future investment plans if you have an existing property with enough equity. There are also a number of non-Australian owned international banks that may be able to help you with finance. A mortgage broker may be able to help you with this by getting touch with the branch themselves.

One important thing to note is that some countries limit you to borrowing 80% of the property value or Loan to Value Ratio (LVR).

Hope this information helps

Cheers,

Arnold