Updated July 2026 by Finder's senior money editor, Richard Whitten.

Types of cashback credit card offers

A cashback credit card gives you money back on your statement or vouchers you can spend.

The most common cashback offers are:

Earning cashback per $1 spent on the card. Some cards offer a percentage cashback on your spending. With a 1% cashback, if you spent $2,000 in a month you'd earn $20 cashback. These cashbacks are typically capped to a certain dollar amount each month.

Promotional sign-up cashbacks. New customers can sometimes get a one-time cashback (often worth several hundred dollars) if they spend a certain amount in the first month or two after activating the card.

You can also convert reward points to cashback

Most rewards credit cards give you the option to convert your reward points into cashback. You can convert 1,250 ANZ Reward Points to a $5 cashback, for example.

The CommBank Yello Cashback Offers program gives people with an eligible Commonwealth Bank credit card or debit card access to cashback offers through the CommBank app. And people with a Westpac credit card can get cashback offers through Westpac Extras.

BCU limits your cashback amount to $500 a year and ING limits the cashback amount to $30 a month or $360 a year. Queensland Country Bank reward dollars are capped at $70 per month or $840 a year.

The pros and cons of cashback credit cards

Pros

Simplicity. Unlike rewards credit cards, where figuring out the value of rewards can be complicated, cash back rewards are straightforward.

Usefulness. Cash or statement credits are a practical and versatile reward. If it's money you were going to spend anyway, the cashback is a nice bonus.

Other perks. Credit cards with cashbacks may offer features like complimentary travel insurance or airport lounge passes.

Cons

Annual fees. Most cards charge an annual fee. Most cashback cards have lower annual fees than frequent flyer or rewards cards though.

High interest rates. If you often carry a balance, the cost of interest could outweigh any cashback rewards that you earn from the card.

Capped rewards. Most cards cap the number of times you can redeem a cashback offer or limit how much of your spending will earn cash back.

Our expert says: Are cashback credit cards worth it?

"I think of cashbacks as a nice little benefit that some cheaper, low rate credit cards offer. The cashback usually outweighs the annual fee but overall it's not the biggest card perk. If you get a more expensive points-earning card you could earn Qantas or Velocity Points worth thousands of dollars. Of course, these cards are for bigger spenders. And some cards offer both a cashback and frequent flyer points! "

Check the introductory offer requirements. If a card offers $200 cashback when you spend $3,000 on eligible purchases in the first 3 months, make sure you can realistically meet that spending requirement. Otherwise you won't qualify for the cashback.

Is the cashback amount worth it? Look at the value of the cash rewards you'll collect versus the card's overall cost. If the value of the cashback isn't worth it, you might find a $0 annual fee or an interest free credit card with a 0% purchase rate offer more suitable for you.

Remember that percentage cashback spend offers are usually capped. Most cashback cards have a limit on how much value you can get back. You could get 1% cashback on your spending, but with a limit of $30 back per month. No matter how much you spend, your cashback will only ever earn you $30 a month or $360 a year.

Rewards value. If you have a rewards credit card that offers cash back and other types of rewards (such as flights, travel upgrades or merchandise), you can check to see if there are rewards that have a higher retail or regular price value than the cashback amount.

How to decide if a cashback credit card is worth it

Let's say you get a credit card that offers 1% cashback on everyday purchases. The card also has a $150 annual fee.

If you spent $3,000 per month on this card: You would earn $30 cash back per month, or $360 per year. If you take the cost of the annual fee out, you would get $210 value from cash back rewards over that year.

But if you only spent $1,000 per month on this card: You would earn $120 cash back in a year. That is $30 less than the $150 annual fee.

In this example the card could still be worth it, if you get other benefits from it like points or complimentary travel insurance. But for the cashback alone it's not worth it.

Frequently asked questions

A cashback credit card offers you rewards in the form of statement credits or vouchers when you meet a spend requirement, or for ongoing eligible spending. Sometimes, you can get a cashback offer on a credit card with ongoing low rates and low or $0 annual fees that aren't typically available with cards that offer ongoing rewards.

Standard rewards credit cards offer points for each $1 of eligible spending, which you can redeem for travel, retail items, gift cards, cashback and more.

You can typically get between $10 and $500 from an introductory cashback offer when you meet the spend requirements. For credit cards that offer ongoing cashback, it's usually between 0.49% and 1% of each eligible transaction.

While these are 2 of the most common types of cashback on credit cards, there are sometimes other promotions that could offer different amounts. For example, a card that has personalised cashback offers with retail partners could offer you $10 back when you spend $30 with the retailer.

Yes, you can generally use cashback rewards to pay your card's annual fee or the outstanding balance of a credit card if you redeem it through a rewards program. But if you get cashback as a credit on your account, you usually still need to make a minimum payment on your account by the statement due date to avoid late payment fees.

Anyone who meets the eligibility requirements for a cashback credit card can apply. These requirements vary between cards, but you can usually expect the following:

Eligibility requirements

Age. You need to be at least 18 years old to apply for a credit card in Australia.

Residency status. Most lenders require you to be a permanent Australian resident or citizen, though some do offer products to specific visa holders.

Income requirements. Some cards list a minimum income amount that you need to earn before you can apply, others require you to earn a regular income. There are also cards that don't list an income requirement – but even then you'll need to include details about your money when you apply.

Credit card eligibility requirements are usually listed on individual card pages, as well as at the start of an online application. Make sure you read them before you apply to help save you time.

How to apply

You can apply online in around 10-20 minutes. Before applying, make sure you meet the eligibility requirements and have the necessary documents needed to complete your application. You'll need to provide proof of identification, proof of income and some additional information about your finances.

Once you have completed and submitted your application, you'll usually receive a response from the credit card provider within 60 seconds. If you're approved, you'll receive your card in the mail within 1-2 weeks.

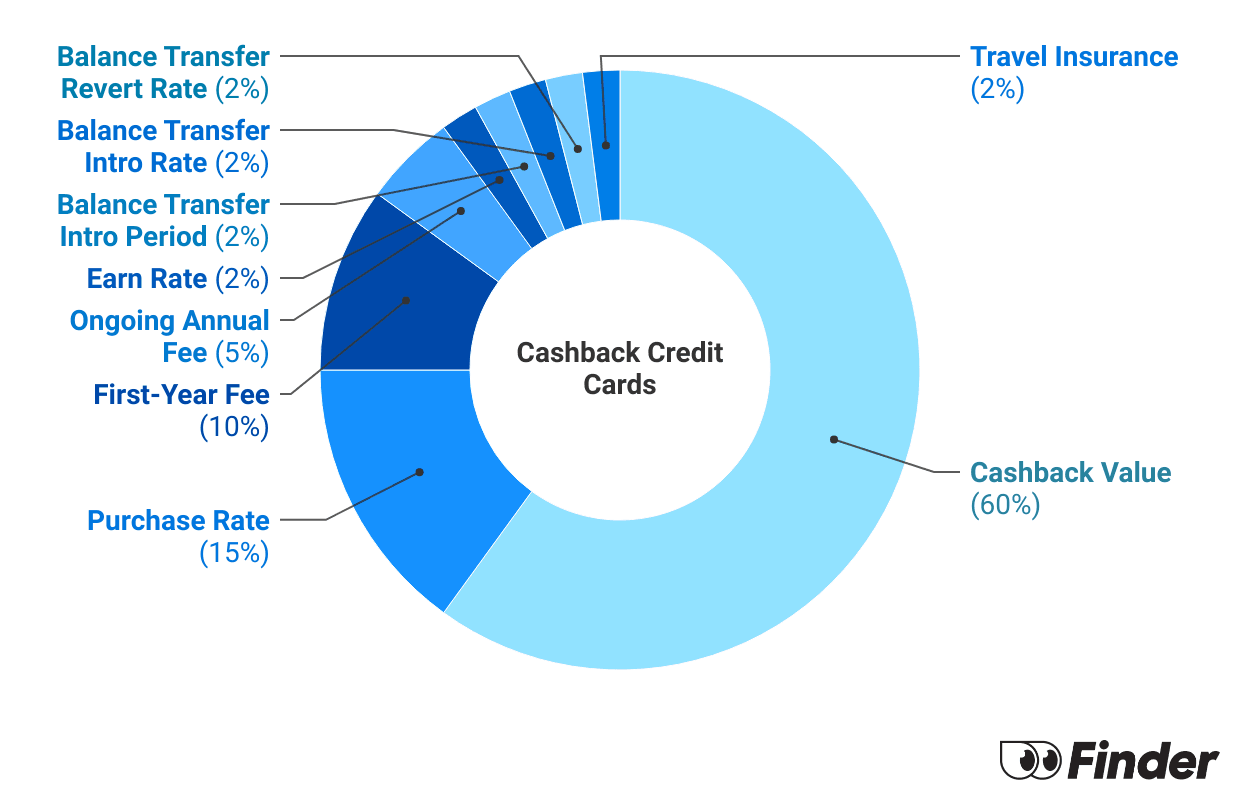

The lowdown on the cashback credit cards Finder Score

The Finder Score helps you sort the junk from the gold so you can compare products faster.

Each month we carefully analyse over 250 credit card products and assess nine features and benefits of each card.

We assign scores out of 10 for each feature, and adjust the scores depending on what category we're looking at. The same card will receive a different score within each category, depending on the features being assessed.

For cashback credit cards, we focus heavily on the quality of the cashback being offered, along with rates and fees.

To qualify for this category, credit cards must:

Offer some form of cashback on spending. Where cashbacks are based on a % value of spend, we use an average monthly spend derived from RBA figures.

The Finder Score methodology is designed by our insights and editorial team. Commercial partners carry no weight, and all products are reviewed objectively.

Remember that Finder Score is just one factor to consider. Look at other aspects like fees, features, benefits and risks to make sure a product is suitable for you.

Cashback credit cards - score weightings

Feature

Definition

Assessment

Weight

Cashback Value

The value of cash returned per dollar spent

Higher cashback rewards result in higher scores

60%

Purchase Rate

Interest rate on new purchases

Lower rates receive higher scores (up to 22.49% max)

Richard Whitten is Finder’s Senior Money Editor, with over eight years of experience in home loans, property, credit cards and personal finance. His insights appear in top media outlets like Yahoo Finance, Money Magazine, and the Herald Sun, and he frequently offers expert commentary on television and radio, helping Australians navigate mortgages and property ownership. Richard started his career in education and textbook publishing in South Korea. He holds multiple industry certifications, including a Certificate IV in Mortgage Broking (RG 206) and Tier 1 and Tier 2 certifications (RG 146), as well as a Bachelor of Education from the University of Sydney and a Graduate Certificate in Communications from Deakin University.

See full bio

Richard's expertise

Richard

has written

759

Finder guides across topics including:

Compare the best Qantas frequent flyer credit cards based on bonus point offers, points per $1 spent, rates, fees and other features so you can find a card that works for you.

Find out how you can keep your overseas spending costs down by comparing credit cards with no foreign transaction fees and no currency conversion fees.

Important information about this website

Finder makes money from featured partners, but editorial opinions are our own.

Finder is one of Australia's leading comparison websites. We are committed to our readers and stand by our editorial principles.

We try to take an open and transparent approach and provide a broad-based comparison service. However, you should be aware that while we are an independently owned service, our comparison service does not include all providers or all products available in the market.

Some product issuers may provide products or offer services through multiple brands, associated companies or different labeling arrangements. This can make it difficult for consumers to compare alternatives or identify the companies behind the products. However, we aim to provide information to enable consumers to understand these issues.

We make money by featuring products on our site. Compensation received from the providers featured on our site can influence which products we write about as well as where and how products appear on our page, but the order or placement of these products does not influence our assessment or opinions of them, nor is it an endorsement or recommendation for them.

Products marked as 'Top Pick', 'Promoted' or 'Advertisement' are prominently displayed either as a result of a commercial advertising arrangement or to highlight a particular product, provider or feature. Finder may receive remuneration from the Provider if you click on the related link, purchase or enquire about the product. Finder's decision to show a 'promoted' product is neither a recommendation that the product is appropriate for you nor an indication that the product is the best in its category. We encourage you to use the tools and information we provide to compare your options.

Where our site links to particular products or displays 'Go to site' buttons, we may receive a commission, referral fee or payment when you click on those buttons or apply for a product.

When products are grouped in a table or list, the order in which they are initially sorted may be influenced by a range of factors including price, fees and discounts; commercial partnerships; product features; and brand popularity. We provide tools so you can sort and filter these lists to highlight features that matter to you.

Please read our website terms of use and privacy policy for more information about our services and our approach to privacy.

We update our data regularly, but information can change between updates. Confirm details with the provider you're interested in before making a decision.

How likely would you be to recommend Finder to a friend or colleague?

0

1

2

3

4

5

6

7

8

9

10

Very UnlikelyExtremely Likely

Required

Thank you for your feedback.

Our goal is to create the best possible product, and your thoughts, ideas and suggestions play a major role in helping us identify opportunities to improve.