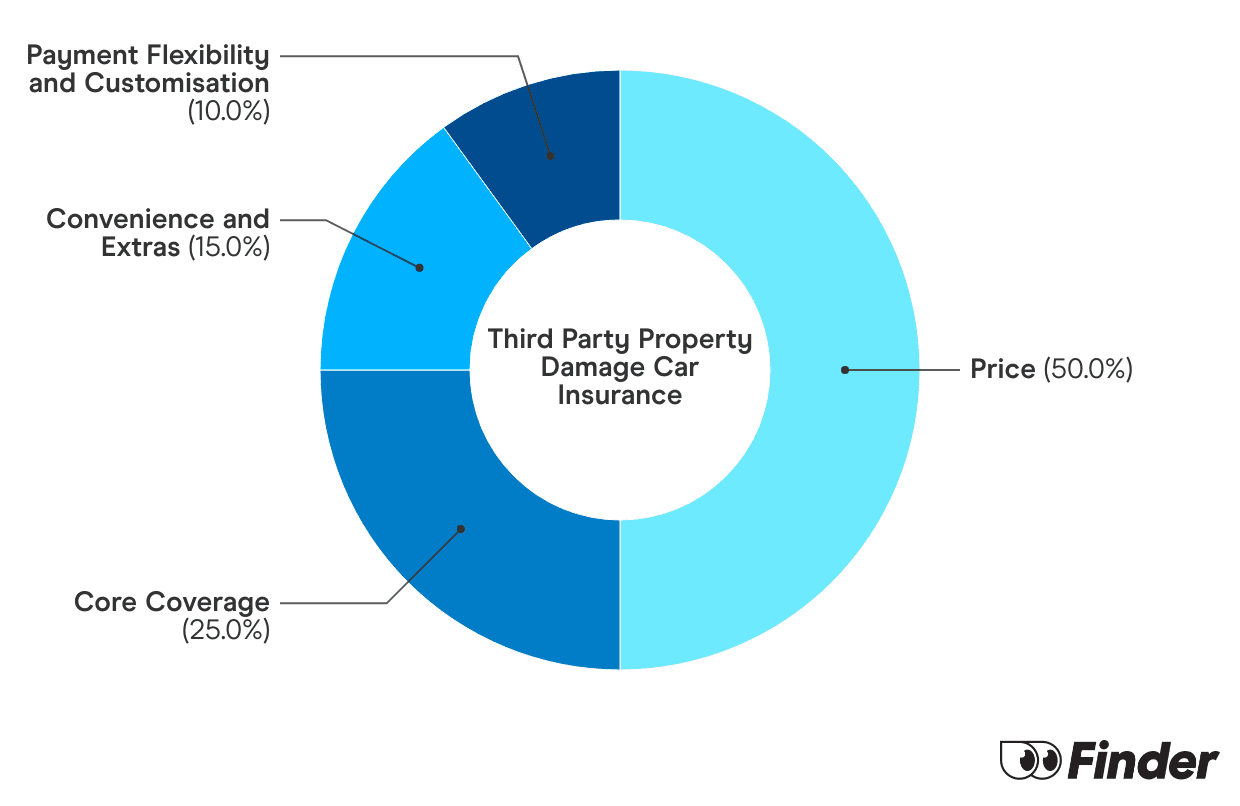

Our verdict:

We researched 31 different third party property damage car insurance policies and Hume Bank was the second cheapest provider, according to our research.

Pros & cons:

- It covers damage you cause to other people's cars or property.

- Hume Bank third party car insurance can also cover you for up to $5,000 if an uninsured motorist damages your car. Not all providers offer this.

- It's underwritten by Allianz so the policy is very similar to Allianz, except it's cheaper.

- Third party policies won't cover damage to your car the same way a comprehensive policy will.

- You're not covered for weather events like fire, storms and hail damage.

I am currently looking for an insurance policy for my son who is about to go on his P’s. I think Third Part Fire and Theft will be fine as we are looking at a car under 10k. However I’m not sure of rates as you need to know models prior to getting quotes. Is there a way of getting quotes without knowing the car you are getting yet?

Hi Suzie, Quotes will always be specific to the model, so you won’t be able to get a quote without one. However, you can get an idea by picking models from your shortlist of potential buys and seeing what the rates are. Realistically, for a P-plate driver you’ll be paying more as the risk is higher for younger drivers, no matter what car you choose.

I have a car with hail damage only.

Can I still get third-party insurance?

Hi Tina,

Provided the car is still safe to drive, it should be possible to get third party car insurance. Good luck!

I am 76, male, car worth less than $10,000, drive less than 5,000 km annually. What’s best, cheapest insurance for me, for damage to other cars only?

Hi Bjorn,

What’s best or cheapest will depend on your personal circumstances and driver profile so I couldn’t recommend specific providers to you. Instead, I can share a few tips to help you find a cheaper policy:

– Get quotes from at least 3-5 providers so you can see the difference in pricing on offer

– Look for sign up discounts

– Consider adjusting your excess; a higher excess means a lower premium. Just be sure you can still afford the excess in the event you’re required to pay it

– Restrict drivers under 25 if you’re sure no one under that age will drive the car. This can help bring the cost down as insurers typically view younger drivers as more risky and can up the premium if they’re not excluded

Remember, every policy varies so to ensure it covers what you need, read the product disclosure statement on the provider’s website.

I hope this helps!

I have a 2004 Holden Berlina which has not been registerred nor driven for 5 years , it is now for sale, can I get CTP insurance for less than 12 months , even 6 month to match the proposed registration term.

James

Hi James, CTP insurance can typically be bought for either 6 or 12 months but it’s best to check with your insurer as payment terms may vary. This page may be helpful for any other questions: https://www.finder.com.au/car-insurance/ctp-insurance

Hello, I have an at fault claim from nearly 4 years ago, a driving under the influence of drugs charge for which I lost my licence for 6 months approx 3 years ago plus I have a criminal record for drug charges… Can you help me weed through the options, if any, available to me to take out a policy?

Hi Ryan,

Check out this article for more info that might be useful for your situation:

https://www.finder.com.au/car-insurance/car-insurance-criminal-record