These products offer the best value and outcomes considering various product features and price.

7+

Great

Competitive products within their group.

5+

Standard

But these products still offer reasonable value and have the basics sorted.

0+

Basic

Offering basic cover with limited features or higher pricing.

What is pay as you go car insurance?

Pay as you go car insurance, also known as pay as you drive, is where premiums are based on the actual distance you drive. The insurers allow you to pay less for your insurance, as they recognise the chance of you having an accident is lower, as you're on the road less.

Insurers often use specific product nomenclature for these offerings, such as a Gold Low Kilometres Policy (a specialised tier designed to provide high-level protection for those who spend less time on the road).

Unlike traditional policies with fixed premiums, this model adjusts costs in line with your driving habits. Because your "risk" is lower, so are your premiums.

How does pay as you go car insurance work?

It doesn't necessarily mean you pay "as you drive" – you can still pay your premium annually. But insurers will calculate your premiums based on your vehicle's estimated and actual usage. There are a few ways they do this:

It is important to understand the operational mechanics: while a standard low-km discount is a flat reduction based on your estimated yearly travel, a true Pay As You Drive (PAYD) policy involves more dynamic tracking or specific odometer-based pricing.

Odometer reading

When you're getting a quote, you provide your odometer reading. Then you select how many kilometres you want to pay for — for example, 3,000km per year. You pay and you're ready to hit the road. If your odometer starts to near this limit but your policy term is not yet expired (meaning you haven't hit 12 months yet), you contact your insurer to top it up. The more kilometres you add, the more you'll pay.

Low kilometres options

Certain policies allow drivers to pre-select a kilometres cap, such as 5,000km or 10,000k, based on anticipated usage. You end up with a policy that's the same as regular comprehensive car insurance, however because you've selected your expected kilometres travelled in a year to be lower, you'll pay less in premiums.

Use of a tracker

Some insurers install telematics devices or use mobile apps to monitor the kilometres you're driving in real-time. This allows the insurer to charge you on a per kilometre basis as they'll know how many kilometres you're travelling. It can be a cost effective solution but, unsurprisingly, some get the ick on this because it feels like an invasion of privacy.

Is pay as you drive car insurance the same as comprehensive car insurance?

Yes, the benefits you receive and the coverage you're eligible for are the same as a standard policy. The difference is the way you track your kilometres and pay the insurer.

If you record your odometer reading and are required to 'top up' if you go over the amount of kilometres you've bought — that's a pay as you drive policy. Similarly, if you install a tracking device so the insurer can record your kilometres travelled and charge you accordingly — that's a pay as you drive policy.

Pay as you drive insurance is essentially a type of comprehensive cover, with your premium structured around how much you drive.

What's covered under pay as you drive car insurance?

Coverage typically mirrors that of comprehensive policies, including:

Accidental damage: Repairs for damages from collisions or other accidents.

Theft and vandalism: Protection against vehicle theft or malicious damage.

Fire damage: Coverage for damages resulting from fire.

It's essential to review individual policies, as coverage details and limits can vary between insurers.

Is pay as you drive car insurance good for seniors?

For seniors who often drive less frequently, pay as you drive insurance can be worth considering. By aligning premiums with actual usage, it offers potential cost savings.

However, it's worth noting that many popular car insurance providers offer coverage options for those who drive an average of 5,000 kilometres per year. If you're expecting to drive around this amount or less, then it's worth considering these providers in your car insurance comparison. While pay as you drive options can provide a cheaper option, this doesn't immediately make them the cheapest or the best for your needs.

Pros and cons of pay as you drive car insurance

Pros

Cost savings: Potentially lower premiums for those who drive less.

Personalised coverage: Policies tailored to individual driving habits.

Incentive to drive less: Potential to reduce driving, benefiting the environment and personal health.

Cons

Kilometres monitoring: Requires tracking of driving distance, which some may find intrusive.

Potential extra costs: Exceeding agreed mileage can lead to additional charges.

Compare pay as you go car insurance options

5 of 5 results

Compare other products

We currently don't have that product, but here are others to consider:

Looking for other options? Check out other similar products.

How we picked these

Finder Score for car insurance

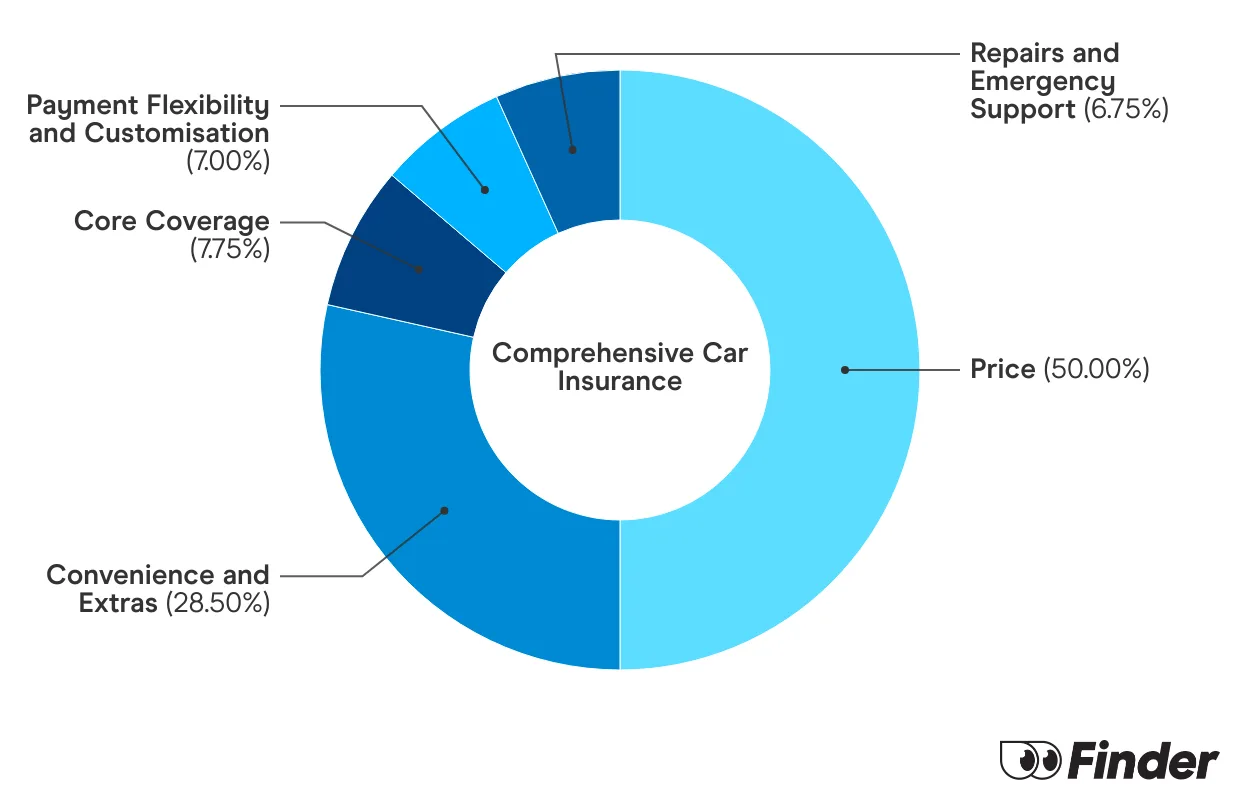

We analyse over 30 car insurance products across insurance providers, and rate each one for price and features. We collect up to 36 quotes per product, for male and female drivers in New South Wales, Victoria, Queensland, South Australia, Tasmania and Western Australia. Quotes are collected for 20 year olds, 30 year olds and 60 year olds, assuming an excess of $850 for a 2020 Toyota Corolla 4 door sedan model, with an average 15,000 kms driven each year. While we are not allowed to display actual quotes, our Finder Score aims to serve as an indicative guide to how cost and feature competitive a product might be for you.

Our feature score assesses each product for more than 15 features across loss and damage coverage, repairs and assistance coverage, personal items coverage and policy coverage. Features we assess include but are not limited to legal liability, essential repairs, new car replacement, car hire events, roadside assistance, agreed or market value, windscreen damage and natural disaster coverage.

"A pay as you drive policy can be great for those who are driving less than 15,000km per year. However, it's worth knowing that a lot of regular insurers charge a lower premium when you drive less kilometres. Compare a few options from pay as you drive providers and normal providers to be sure that you're getting the best deal."

Peta Taylor

Associate publisher

FAQs

Traditional car insurance involves fixed premiums based on projected usage that typically exceeds 15,000km, while pay as you drive insurance adjusts costs based on actual kilometres travelled, benefiting those who drive less.

Exceeding the predetermined mileage may result in additional charges or a reassessment of your premium. It's crucial to understand the terms of your policy to avoid unexpected costs. In most cases, if you think you're going to exceed your agreed mileage, you can pay to top it up.

Yes, many insurers allow policyholders to switch between pay as you drive and traditional policies. If you anticipate an increase in your driving frequency, discuss options with your insurer to ensure continuous and appropriate coverage.

Monitoring methods differ by insurer. Some may require periodic odometer readings, while others utilise telematics devices or mobile apps to track kilometres in real-time.

Peta Taylor is a publisher at Finder, working across all of insurance. She's been analysing product disclosure statements and publishing articles for over 2 years. Peta is passionate about demystifying complex insurance products to help users make well educated decisions with confidence. Peta is part of Finder's insurance awards team and works alongside editorial and insights experts to bring users the best insurance products every year.

See full bio

Australian Unity car insurance, underwritten by Allianz, offers two levels of cover, the freedom to choose your own repairer and an easy 24-hour claims service.

With a higher-than-average price but no particularly impressive benefits, Allianz was outperformed by many other car insurers in the 2024 Finder Insurance Awards.

With strong cover and reasonably-priced policies, AAMI performed well in the 2024 Finder Awards. However, some popular benefits are missing and cheaper options are available.

Important information about this website

Finder makes money from featured partners, but editorial opinions are our own.

Finder is one of Australia's leading comparison websites. We are committed to our readers and stand by our editorial principles.

We try to take an open and transparent approach and provide a broad-based comparison service. However, you should be aware that while we are an independently owned service, our comparison service does not include all providers or all products available in the market.

Some product issuers may provide products or offer services through multiple brands, associated companies or different labeling arrangements. This can make it difficult for consumers to compare alternatives or identify the companies behind the products. However, we aim to provide information to enable consumers to understand these issues.

We make money by featuring products on our site. Compensation received from the providers featured on our site can influence which products we write about as well as where and how products appear on our page, but the order or placement of these products does not influence our assessment or opinions of them, nor is it an endorsement or recommendation for them.

Products marked as 'Top Pick', 'Promoted' or 'Advertisement' are prominently displayed either as a result of a commercial advertising arrangement or to highlight a particular product, provider or feature. Finder may receive remuneration from the Provider if you click on the related link, purchase or enquire about the product. Finder's decision to show a 'promoted' product is neither a recommendation that the product is appropriate for you nor an indication that the product is the best in its category. We encourage you to use the tools and information we provide to compare your options.

Where our site links to particular products or displays 'Go to site' buttons, we may receive a commission, referral fee or payment when you click on those buttons or apply for a product.

When products are grouped in a table or list, the order in which they are initially sorted may be influenced by a range of factors including price, fees and discounts; commercial partnerships; product features; and brand popularity. We provide tools so you can sort and filter these lists to highlight features that matter to you.

Please read our website terms of use and privacy policy for more information about our services and our approach to privacy.

We update our data regularly, but information can change between updates. Confirm details with the provider you're interested in before making a decision.

How likely would you be to recommend Finder to a friend or colleague?

0

1

2

3

4

5

6

7

8

9

10

Very UnlikelyExtremely Likely

Required

Thank you for your feedback.

Our goal is to create the best possible product, and your thoughts, ideas and suggestions play a major role in helping us identify opportunities to improve.