Third party, fire and theft insurance covers you if your vehicle's stolen or damaged by fire. Or, if you're at fault for an accident that damages a person's vehicle or property.

These products offer the best value and outcomes considering various product features and price.

7+

Great

Competitive products within their group.

5+

Standard

But these products still offer reasonable value and have the basics sorted.

0+

Basic

Offering basic cover with limited features or higher pricing.

Finder Score for car insurance

We analyse over 30 car insurance products across insurance providers, and rate each one for price and features. We collect up to 36 quotes per product, for male and female drivers in New South Wales, Victoria, Queensland, South Australia, Tasmania and Western Australia. Quotes are collected for 20 year olds, 30 year olds and 60 year olds, assuming an excess of $850 for a 2020 Toyota Corolla 4 door sedan model, with an average 15,000 kms driven each year. While we are not allowed to display actual quotes, our Finder Score aims to serve as an indicative guide to how cost and feature competitive a product might be for you.

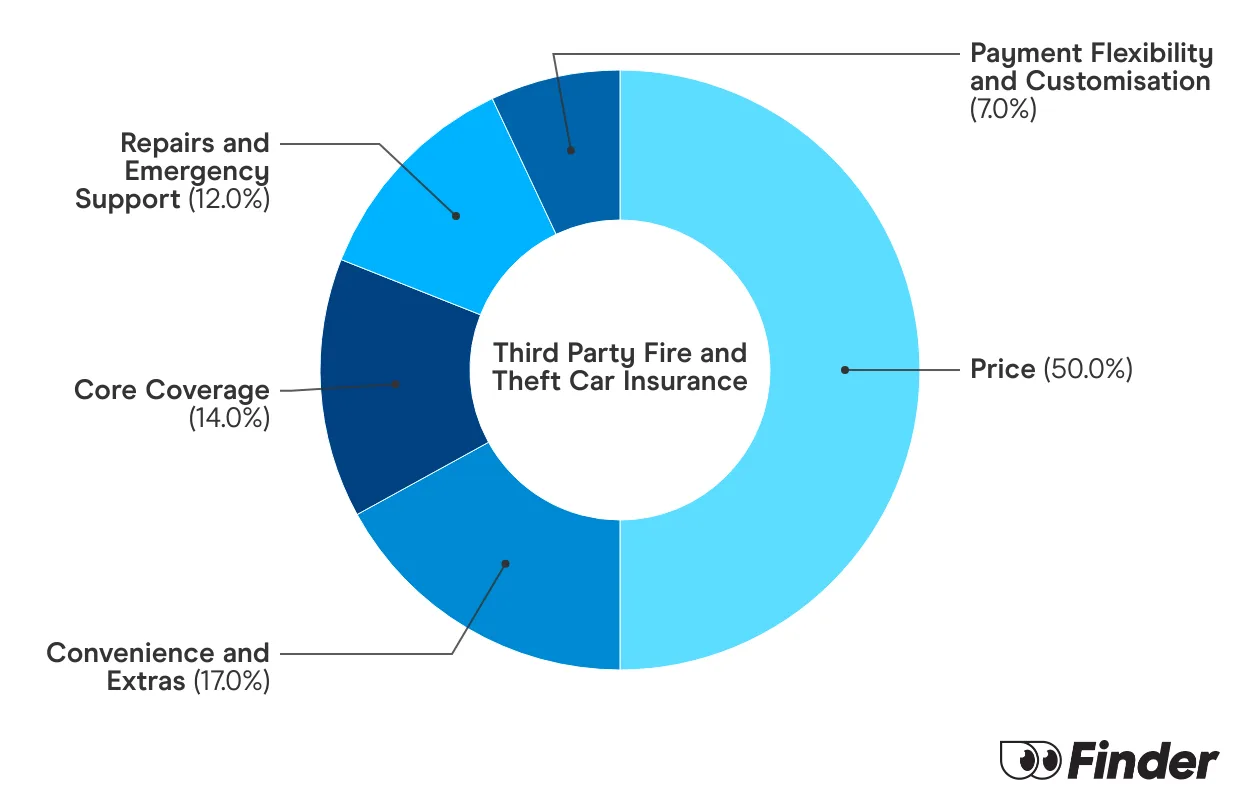

Our feature score assesses each product for more than 15 features across loss and damage coverage, repairs and assistance coverage, personal items coverage and policy coverage. Features we assess include but are not limited to legal liability, essential repairs, new car replacement, car hire events, roadside assistance, agreed or market value, windscreen damage and natural disaster coverage.

Third party, fire and theft car insurance covers you for damage to another person's vehicle or property as well as damage to your car by fire or theft. It does not cover damage to your vehicle in the event of an accident; for that, you'll need comprehensive car insurance.

What does third party fire and theft cover?

Third party fire and theft car insurance covers you for damage to another person's vehicle or property, plus damage to your car by fire or theft.

It's a step up from third party car insurance, which only covers damage to another person's vehicle or property.

It doesn't cover damage to your vehicle in the event of an accident; for that, you'll need comprehensive car insurance.

Finder's top pick for August 2026

If you're looking at third party fire and theft car insurance, chances are you don't want to dish out thousands a year for comprehensive cover but you want a bit more than a basic third party policy. Maybe you're worried about theft, live in a bushfire area; regardless, we can help. Our insurance team collected 199 third party fire and theft quotes from 20 popular car insurers and analysed dozens of features to see who came out on top.

Budget Direct third party fire and theft

Our verdict

Budget Direct was the cheapest third party fire and theft policy on average across all major states, according to our research. In addition to cover for damage to other people's property, fire and theft, it also covers your car for damage caused by an uninsured driver, up to $5,000.

Pros and cons

Cheap third party fire and theft policy.

You can reduce costs by restricting drivers.

Hire car following theft - up to $1,500, up to 21 days.

The 15% sign-up discount only applies for the 12 months.

It doesn't generally cover damage to your own car (only if an uninsured driver hits you).

AAMI and Virgin were around the same price in our analysis – marginally more expensive.

There are 4 main types of car insurance available. Here's a summary of what they cover. As you can see, third party fire and theft is a good medium for those who want some cover but don't want the full expense of comprehensive cover:

Cover

CTP insurance

Third party property damage insurance

Third party, fire and theft insurance

Comprehensive car insurance

Damage to my vehicle in an accident

No

No

No

Yes

Damage to another person's vehicle or property

No

Yes

Yes

Yes

Loss or damage to my car due to fire

No

No

Yes

Yes

Loss or damage to my car due to theft

No

No

Yes

Yes

Loss or damage to my car due to storm, hail and flood

No

No

No

Yes

Our expert says

"I have a Third Party, Fire and Theft policy with Budget Direct. I went with this policy because it gives me peace of mind but is also cost-effective. I drive an older car and I would replace it if it were damaged or broke down. So this policy makes sense for me."

What are the benefits of third party, fire and theft car insurance?

It covers some common risks. Get protection for car accidents, theft and fire damage – among the biggest risks all drivers face.

It can be cheaper than comprehensive car insurance. This mid-level policy option combines a decent range of cover with competitive premiums. But, it doesn't offer the same level of insurance as comprehensive cover. For example, it won't cover the contents in your car or replacement keys.

It offers additional benefits. Most third party, fire and theft policies also include a range of additional benefits, such as towing and storage costs, a hire car after theft, and cover for damage caused by uninsured motorists.

It provides peace of mind. Like any form of car insurance, third party, fire and theft insurance is all about peace of mind. It gives you the confidence and reassurance you need before getting behind the wheel.

What isn't covered by third party, fire and theft insurance?

There are a few situations where third party, fire and theft insurance won't cover you. The main ones relate to damages to your car.

Natural disasters. You won't be covered for natural disasters including storms, floods, hailstorms, earthquakes or landslides. The one exception is bushfire since it does cover fire of all types.

Accidents you cause. You won't be covered for any damage to your own car if you cause the crash.

Vandalism. You won't be covered for vandalism. However, you will be covered if someone damages your car while attempting to steal it.

Hitting an animal. You won't be covered for hitting an animal, even if there was nothing you could do to avoid it.

How can I find the cheapest third party, fire and theft policy?

Compare policies. It's quick and easy to compare car insurance quotes online, so get quotes from multiple insurers and see which policy comes out on top.

Choose a higher excess. The higher your excess, the cheaper your premium will be.

Take advantage of discounts. Many insurers offer discounts to new customers. Some sign up discounts are as generous as 15% off.

Restrict cover. Restricting younger drivers can help you reduce your premiums as you're seen as less risky. Remember, this is only a good option if you're certain no younger drivers will drive your car.

Secure your vehicle. Vehicles that are kept in a locked garage are often cheaper to insure as they're seen as less risky.

Who is third party, fire and theft car insurance good for?

A third party, fire and theft policy is good if:

You want protection against damage you cause to other people's cars or property; theft or fire damage to your own vehicle; and cover for legal expenses after an accident.

You're keeping a close eye on your budget. Put simply, it's usually cheaper than comprehensive insurance.

Theft is a worry where you live or work. It's worth considering if you're based in an area that carries a high risk of vehicle thefts.

You drive an inexpensive car. If your vehicle has a low market value, you may decide that mid-range coverage is enough for you.

FAQs

Third party, fire and theft is worth it if you don't need the full cover for your own car, but have a higher risk of experiencing fire damage or theft.

Also, you'll find it more useful than the more basic third party property cover, especially if you:

Don't have secure parking

Commonly travel with your car

Live in a bushfire-prone area

Live or work in a high-crime area

Many policies also cover you for a hire car if your car is stolen, and may even offer emergency transportation and accommodation if it's stolen while you're far from home.

CTP only pays for injuries that you cause to others with your car. It's also called your green slip. Whereas third party, fire and theft also protects you if you damage someone's property like their car, bicycle or fence. It can also provide some limited protection for your own car.

Both policies provide cover for your legal liability when you're responsible for a car accident that causes damage to someone else's car or property. But third party, fire and theft insurance provides cover for loss or damage to your vehicle caused by fire or theft; third party property insurance doesn't.

Comprehensive car insurance covers damage to your own vehicle if you're involved in an accident, third party car insurance does not.

No. The insurance is for your vehicle only and will not cover you when you drive other cars.

No. This type of cover only covers damage to someone else's vehicle or property in an accident for which you're responsible. However, many policies will include a limited level of cover when your vehicle is damaged in a no-fault accident with an uninsured motorist.

Yes. Most policies let you accrue a no-claims bonus. But read the policy wording or give an insurer a call if you're in any doubt about what you're covered for.

James Martin was the insurance editor at Finder. He has written on a range of insurance and finance topics for over 7 years. James often shares his insurance expertise as a media spokesperson and has appeared on Prime 7 News, Insurance News, 7NEWS and The Guardian. An experienced journalist, James' work has featured in publications including The Irish Times, Companies100 and In Business. He holds a Tier 1 General Insurance (General Advice) certification and a Tier 1 Generic Knowledge certification, both of which meet the requirements of ASIC Regulatory Guide 146 (RG146).

See full bio

James's expertise

James

has written

180

Finder guides across topics including:

Gary Ross Hunter has over 6 years of expertise writing about insurance, including life, health, home, and car insurance. Having reviewed hundreds of product disclosure statements and published over 800 articles, he loves simplifying complex insurance topics for everyday readers. Gary has contributed to major outlets like Yahoo Finance, The Sydney Morning Herald, and news.com.au, and holds a Bachelor of Arts (Honours) in English Literature from the University of Glasgow, along with a Tier 2 General Advice certification, ensuring his work adheres to ASIC’s RG146 standards.

See full bio

Gary Ross's expertise

Gary Ross

has written

558

Finder guides across topics including:

If you are in an accident caused by another fully insured person and I’m on Third party or third party, Fire/theft is my vehicle fully repaired by their insurance company as I’ve only seen $5000 by an uninsured motorist at fault

Finder

SarahMay 1, 2026Finder

Hi David,

Yes, if the other driver is at fault and fully insured, their insurer should cover the full cost of repairing your vehicle, regardless of whether you only have Third Party or Third Party Fire & Theft. That $5,000 cap you’ve seen applies when you’re claiming through your own policy after being hit by an uninsured driver, not when the at-fault driver has insurance.

In practice, you can either lodge a claim with your own insurer (e.g. NRMA Insurance) and let them recover the costs; or claim directly against the at-fault driver’s insurer and they should pay reasonable repair costs (or market value if it’s a write-off). Just be aware you’ll need to clearly establish fault and provide the other driver’s details, and you may have to chase things a bit more yourself if you don’t go through your own insurer. Hope this helps!

RoscoJune 3, 2025

Can you insure a car for 6 months with third party insurance

Finder

PetaJune 4, 2025Finder

Hi Rosco,

Yes, you can do this but you’ll likely have to opt to pay monthly and then just cancel after 6 months. Most providers only offer annual or monthly payments.

Hope this helps!

ByronJune 20, 2024

I am looking for an insurance company to insurer my son’s vehicle he is 19 years old and has had two suspensions with in 2 years, the vehicle is a 2008 Toyota Hilux.

Finder

SarahJuly 18, 2024Finder

Hi Byron, It may be possible to get cover, but will definitely vary between insurers. He should check out this page: https://www.finder.com.au/car-insurance/high-risk-car-insurance – there’s a section on insurers who we found would insure people after license suspension. Obviously his driver profile will be different so there are no guarantee, but this is a good place to start. Best of luck!

MichelleMay 21, 2024

Need to get motor vehicle cover for one day have asked a couple of insurers, telling me they only do yearly policies, in the old days this was usually done by your insurer as a cover note, only required to drive back from motor vehicle dealership.

Finder

SarahMay 24, 2024Finder

Hi Michelle,

This cover isn’t available any more, as the assumption is you’ll continue to want cover beyond driving the vehicle home from the dealership. In the past this was available because you had to buy a policy during business hours. Now that it’s possible to buy a policy online at any time of the day or night or on weekends, there’s no need for one-day cover anymore.

Hope this helps!

rossMarch 6, 2017

need cover have driver (L)with drug conviction less than 3yrs

Finder

ZubairMarch 8, 2017Finder

Hi Ross,

Thank you for your question.

finder.com.au is a comparison and information service and not an insurer. Most insurers in Australia will ensure you with a drug conviction but depending on the offense, you may pay a little more for cover.

Please make sure though to read the eligibility criteria, features, and details of the policy, as well as the relevant Product Disclosure Statement PDS/T&C’s of the policy before making a decision and consider whether the product is right for you. If necessary, speak to the insurance brand to verify any details.

Australian Unity car insurance, underwritten by Allianz, offers two levels of cover, the freedom to choose your own repairer and an easy 24-hour claims service.

With a higher-than-average price but no particularly impressive benefits, Allianz was outperformed by many other car insurers in the 2024 Finder Insurance Awards.

Explore our analysis and see how you can find the best car insurance for your needs.

Important information about this website

Finder is a comparison service. We do not compare every product or every provider in the market.

We make money through commercial arrangements with some of the providers on this site. Products marked 'Sponsored', 'Promoted', 'Featured' or 'Advertisement' appear as a result of a commercial arrangement.

Our editorial content, product reviews and any 'Top Pick' designations are prepared independently of these commercial arrangements.

The default order of products in our tables can be influenced by commercial arrangements. You can re-sort or filter using the controls above each table.

Some content on this site may be generated or supported by AI tools. You should verify details directly with the provider.

Finder is one of Australia's leading comparison websites. We are committed to our readers and stand by our editorial principles.

Our comparison service does not include every product or every provider in the market. Some product issuers offer their products under multiple brands or through associated companies. Where we can, we identify the underlying issuer so you can compare like with like, but you should always check with the provider directly to confirm which brand you are dealing with.

Finder is a comparison website and an intermediary. We are not a product issuer and we do not provide personal financial or credit advice. When you click a link to a product, or apply for a product through our site, you deal directly with the product issuer. We may receive a referral fee, commission or other payment from the issuer if you click through, apply or take out a product. We describe these arrangements in more detail under 'How we make money' below.

Product features, fees, terms and eligibility criteria are set by the product issuer and may change. We rely on information supplied by issuers when we present product details on our site. Before you apply for or take out any product, you should confirm the details directly with the issuer.

We earn revenue from Finder in four principal ways:

Referral fees and commissions. When you click a product link, complete an enquiry form or apply for a product through our site, we may receive a referral fee, commission or other payment from the product issuer. We may also receive payment based on the volume of leads or conversions we send to an issuer.

Sponsored placements. Products marked 'Sponsored', 'Promoted', 'Featured' or 'Advertisement' appear as a result of a commercial arrangement between Finder and the issuer. These labels always indicate a paid placement. We do not use them for editorial choices.

Display advertising. Banner advertising, newsletter advertising and similar display ads on our site are paid by advertisers.

Content sponsorship. Some articles, videos and social media posts are sponsored by an issuer and are clearly labelled as such.

Our editorial opinions, product reviews and any 'Top Pick' designations are prepared independently of these commercial arrangements. A 'Top Pick' is an editorial choice made by our writers and editors based on the criteria described on each comparison page. A 'Top Pick' is not a personal recommendation and does not mean the product is appropriate for your circumstances.

If you would like to know whether we have a commercial arrangement with a specific product issuer, please contact us.

When products are grouped in a table or list, the default order can be influenced by commercial arrangements we have with product issuers. In some categories, sponsored or featured products appear in the top positions of the table by default, and are always labelled as such.

Other factors that influence default order include price, fees and features, and (where relevant) our editorial view of the product.

You can re-sort every comparison table using the controls above the table. You can filter by product features that matter to you. The order you see after re-sorting or filtering is not influenced by commercial arrangements.

Some content on this site is generated or supported by artificial intelligence tools, including our AI-powered assistant FinderBot. AI-generated content may contain errors. Please verify important information directly with the product issuer before making a financial decision. For more information about FinderBot, see the FinderBot Terms of Use and FinderBot Privacy Collection Notice.

Please read our website terms of use and privacy policy for more information about our services and our approach to privacy.

We update our data regularly, but information can change between updates. Confirm details with the provider you're interested in before making a decision.

Our goal is to create the best possible product, and your thoughts, ideas and suggestions play a major role in helping us identify opportunities to improve.

If you are in an accident caused by another fully insured person and I’m on Third party or third party, Fire/theft is my vehicle fully repaired by their insurance company as I’ve only seen $5000 by an uninsured motorist at fault

Hi David,

Yes, if the other driver is at fault and fully insured, their insurer should cover the full cost of repairing your vehicle, regardless of whether you only have Third Party or Third Party Fire & Theft. That $5,000 cap you’ve seen applies when you’re claiming through your own policy after being hit by an uninsured driver, not when the at-fault driver has insurance.

In practice, you can either lodge a claim with your own insurer (e.g. NRMA Insurance) and let them recover the costs; or claim directly against the at-fault driver’s insurer and they should pay reasonable repair costs (or market value if it’s a write-off). Just be aware you’ll need to clearly establish fault and provide the other driver’s details, and you may have to chase things a bit more yourself if you don’t go through your own insurer. Hope this helps!

Can you insure a car for 6 months with third party insurance

Hi Rosco,

Yes, you can do this but you’ll likely have to opt to pay monthly and then just cancel after 6 months. Most providers only offer annual or monthly payments.

Hope this helps!

I am looking for an insurance company to insurer my son’s vehicle he is 19 years old and has had two suspensions with in 2 years, the vehicle is a 2008 Toyota Hilux.

Hi Byron, It may be possible to get cover, but will definitely vary between insurers. He should check out this page: https://www.finder.com.au/car-insurance/high-risk-car-insurance – there’s a section on insurers who we found would insure people after license suspension. Obviously his driver profile will be different so there are no guarantee, but this is a good place to start. Best of luck!

Need to get motor vehicle cover for one day have asked a couple of insurers, telling me they only do yearly policies, in the old days this was usually done by your insurer as a cover note, only required to drive back from motor vehicle dealership.

Hi Michelle,

This cover isn’t available any more, as the assumption is you’ll continue to want cover beyond driving the vehicle home from the dealership. In the past this was available because you had to buy a policy during business hours. Now that it’s possible to buy a policy online at any time of the day or night or on weekends, there’s no need for one-day cover anymore.

Hope this helps!

need cover have driver (L)with drug conviction less than 3yrs

Hi Ross,

Thank you for your question.

finder.com.au is a comparison and information service and not an insurer. Most insurers in Australia will ensure you with a drug conviction but depending on the offense, you may pay a little more for cover.

You may find our car insurance for learner drivers and car insurance for drivers convicted of drunk driving guides helpful.

Please make sure though to read the eligibility criteria, features, and details of the policy, as well as the relevant Product Disclosure Statement PDS/T&C’s of the policy before making a decision and consider whether the product is right for you. If necessary, speak to the insurance brand to verify any details.

Cheers,

Zubair