Customer service

2025 Finder Customer Satisfaction Award

T&Cs apply

Comprehensive car insurance is the only type of car insurance that will cover your own car as well as other people's property. If you want to protect your own vehicle against accidental damage then comprehensive cover is what you're after.

Our car insurance experts have selected a bunch of comprehensive car insurers that we consider best in class, based on extensive research. Whether you prioritise price, features, customer service or something else — there's a pick for you. Remember, the below should be used as a guide only and you should always read the product disclosure statement (PDS) to know if it's right for you.

We currently don't have that product, but here are others to consider:

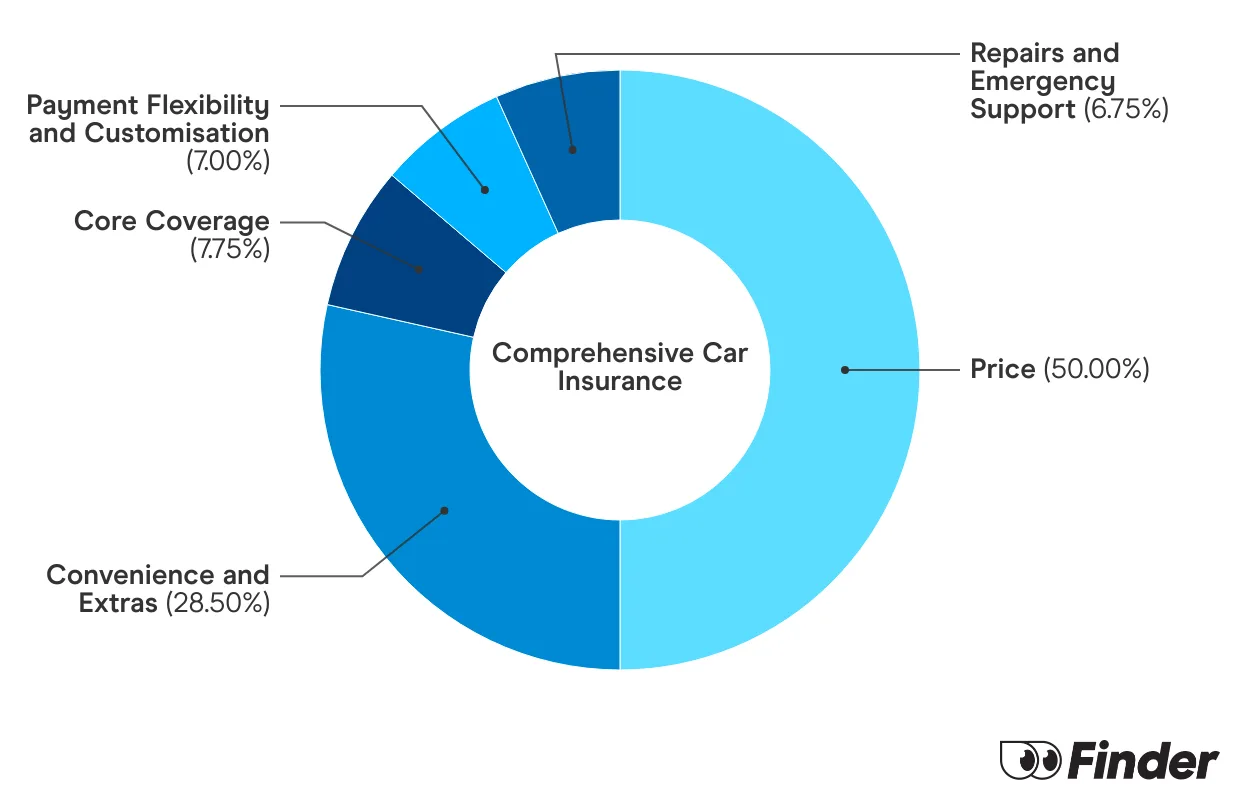

How we picked theseWe analyse over 30 car insurance products across insurance providers, and rate each one for price and features. We collect up to 36 quotes per product, for male and female drivers in New South Wales, Victoria, Queensland, South Australia, Tasmania and Western Australia. Quotes are collected for 20 year olds, 30 year olds and 60 year olds, assuming an excess of $850 for a 2020 Toyota Corolla 4 door sedan model, with an average 15,000 kms driven each year. While we are not allowed to display actual quotes, our Finder Score aims to serve as an indicative guide to how cost and feature competitive a product might be for you.

Our feature score assesses each product for more than 15 features across loss and damage coverage, repairs and assistance coverage, personal items coverage and policy coverage. Features we assess include but are not limited to legal liability, essential repairs, new car replacement, car hire events, roadside assistance, agreed or market value, windscreen damage and natural disaster coverage.

To give you an idea of how much comprehensive car insurance might cost, we've broken down prices by different ages. However, the best car insurance for you may be determined by more than cost.

Keep in mind, costs differ based on your individual circumstances.

The providers listed in the table below were the top 5 cheapest of the providers we researched and reflect the estimated annual cost based on the profile used. Keep in mind, your own cost will vary depending on your personal circumstances and it's always best to compare a range of providers.

| Brand | State | Quote |

|---|---|---|

| Bingle | NSW | $1,074.39 |

| Qantas | NSW | $1,212.97 |

| Budget Direct | NSW | $1,273.62 |

| Coles | NSW | $1,305.87 |

| ING | NSW | $1,411.89 |

| Youi | VIC | $1,126.51 |

| Bingle | VIC | $1,487.74 |

| Budget Direct | VIC | $1,562.13 |

| Coles | VIC | $1,607.82 |

| ING | VIC | $1,665.09 |

| Bingle | QLD | $947.21 |

| ING | QLD | $1,041.2 |

| Budget Direct | QLD | $1,093.26 |

| Coles | QLD | $1,129.69 |

| Allianz | QLD | $1,206.44 |

ALDI car insurance offers comprehensive car insurance with really solid benefit limits.

ahm offers a decent level of coverage but might not suit drivers on a tighter budget.

RACQ offers strong benefits and service, but drivers can expect to pay higher premiums and a joining fee.

With 5% off for seniors, budget-friendly policies, and some uncommon benefits, Australian Seniors is worth considering.

ANZ car insurance is typically more expensive than average, but it does have some generous benefits.

Australian Unity car insurance, underwritten by Allianz, offers two levels of cover, the freedom to choose your own repairer and an easy 24-hour claims service.

APIA car insurance is issued by AAI Limited and offers 3 levels of cover, a range of discounts and a lifetime guarantee on repairs.

Coles car insurance is a budget-friendly option for young people, but older drivers may be able to find cheaper cover elsewhere.

With a higher-than-average price but no particularly impressive benefits, Allianz was outperformed by many other car insurers in the 2024 Finder Insurance Awards.

Explore our analysis and see how you can find the best car insurance for your needs.