Most credit cards charge a hefty 2–3.5% international transaction fee when you use it overseas while traveling or shopping online. But not these cards.

Many credit cards charge 2%+ all international transactions, which can quickly add up when you're travelling or shopping online. A card with no fees can save you hundreds of dollars.

The Bankwest Breeze Platinum Mastercard won the 2026 Finder Award for best travel credit card.

Check the annual fee and pay off your card in full each month to maximise your savings.

How do credit cards with no foreign transaction fees work?

A small selection of credit cards don't charge you the standard 2 to 3.5% fee when using the card overseas. Some cards charge the fee but give you a rebate.

This is a great benefit if you're using the credit card overseas while travelling, or even if you're just shopping online at non-Australian merchants.

Finder ranks the best no foreign transaction fee credit cards using the Finder Score, which considers fees but also benefits like interest-free days and complimentary travel insurance.

How much can I save with a 0% foreign transaction fee card?

If you spent $2,000 on a card with a 3% international transaction fee, it would cost you $60. A 0% fee card would save you $60 in one transaction.

Keep in mind that the cost of foreign transaction fees may not be obvious straight away, as they are added as separate transactions on your credit card account.

In 2024 the ACCC found that credit and debit cards can be cheaper than travel credit cards when making purchases overseas. Especially cards that don't charge international transaction fees.

Bankwest's Breeze Platinum Mastercard is Finder's winning Travel Credit Card at the 2026 Finder Credit Card Awards. The card combines 0% foreign transaction fees with a low annual fee.

Bankwest's Breeze Platinum Mastercard is Finder's winning Travel Credit Card at the 2026 Finder Credit Card Awards. The card combines 0% foreign transaction fees with a low annual fee.

How to compare no foreign transaction fee credit cards

0% fee conditions. Certain credit cards automatically waive foreign transaction fees when you make an international purchase. Others offer a rebate when you meet specific requirements.

Annual fees. Annual fees typically range from $0 to $400 or more for higher-end cards. You can weigh this fee against the value you'd get from 0% foreign transaction fees and any other card perks.

Interest rates. Interest rates on these cards range from around 10% to 28% for purchases. If you pay off your credit card as you go – or pay the total by the due date on your statement – you'll typically get interest-free days on your purchases. But if you end up carrying over a balance, a low rate credit card could be a more cost-effective option.

Overseas ATM withdrawal fees. Overseas ATM fees typically cost around $5 or between 2-3% of the total transaction. And that's not including any charges added by the overseas ATM operator.

💡 Tip: If you're planning to withdraw international currency from an overseas ATM, a multi-currency account such as Wise or the HSBC Everyday Global Account means avoiding cash advance fees. You can also check out Finder's guide to travel money for other options.

Want to use your credit card in Australia as well?

The range of credit cards that offer no foreign transaction fees means it's worth looking for other features that you want on your credit card. For example frequent flyer points, 0% interest rate offers, cashback bonuses or something else. The key is to find a card with features that add value when you're shopping in Australia and overseas.

Our expert says: You don't have to use a credit card when you travel

"I use a frequent flyer credit card when booking flights and hotels so I can earn points. But when I go overseas I use a travel card like Wise. This lets me load up money in a foreign currency pretty cheaply and spend it like a local. For me it's the best of both worlds."

When you're planning to use your card overseas spending, keep the following details in mind:

Daily cash withdrawal limits. Some credit card providers have a limit on the amount you can withdraw from an ATM using your credit card – and it could be lower than your available credit limit. Check your credit card account details through Internet or mobile banking, or call your provider for specific information on these limits.

Global ATM alliance networks. Many Australian credit card providers have ATM alliance networks that extend around the world and allow you to get cash out overseas without paying an ATM withdrawal fee. For example, a credit card from Westpac, St.George, BankSA or Bank of Melbourne gives you access to the Global ATM Alliance network, which includes Westpac NZ (New Zealand), Barclays (UK), Bank of America (US) and Deutsche Bank (Germany and Spain).

Exchange rates. Currency exchange rates will apply when you use an Australian credit card for a transaction in another currency. This rate can fluctuate daily, making it harder to work out the cost in Australian dollars (until it's added to your transaction list).

These cards offer lower currency conversion fees and relevant perks for travelers like insurance and ATM access.

7+

Great

Reasonable cards for travelers, however can potentially charge higher fees.

5+

Standard

While eligible to be used to travelers internationally, these cards may charge currency conversion, overseas ATM withdrawal and ongoing fees.

0+

Basic

These cards should be used for international purchases only in the event of an emergency.

The lowdown on Finder Score

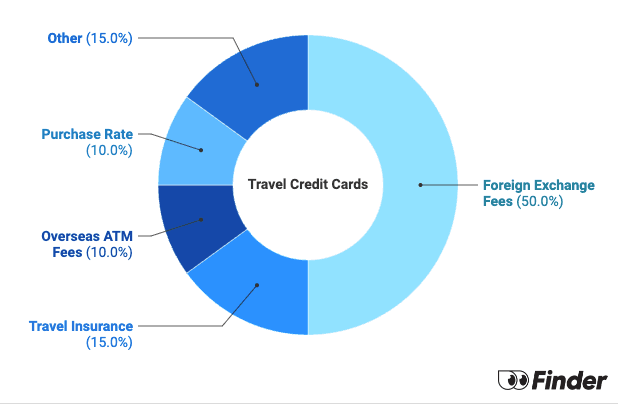

The Finder Score gives you a simple score out of 10, the higher the better. In the travel card category we examine 250+ credit cards and assess six features, assigning them scores out of 10.

We look at features like international transaction fees, travel insurance, annual fees and the purchase rate. Cards with 0% foreign transaction fees and other travel perks score higher.

The methodology is designed by our insights and editorial team. Commercial partnerships carry no weight, all products in the database are scored objectively.

The same card will receive a different score within each category, depending on the features being assessed.

Our intention is to enable informed financial decision-making quickly and easily. Please consider your own financial circumstances when making a decision.

9+ Excellent - These cards offer lower currency conversion fees and relevant perks for travellers like insurance and ATM access.

7+ Great - Reasonable cards for travellers, however can potentially charge higher fees. 5+ Satisfactory - While eligible to be used to travellers internationally, these cards may charge currency conversion, overseas ATM withdrawal and ongoing fees.

Less than 5–Basic - These cards should be used for international purchases only in the event of an emergency.

Finder Score metric assessment - Travel credit cards

Feature

Definition

Assessment

Weight

Foreign Exchange Fees

Fees charge on international transactions

Lower fees score higher

50%

Travel Insurance

Complimentary travel insurance

Full score for complimentary insurances

15%

Overseas ATM Fees

Fees charged by card provider to withdraw from international ATMs

Lower fees score higher

10%

Purchase Rate

Interest rate on new purchases

Lower rates score higher

10%

First-Year Fee

Annual fee charged in the first year of ownership

Lower fees score higher. $0 fee receives the maximum points.

7.5%

Ongoing Annual Fee

Annual fee charged from the second year onwards

Lower fees score higher. $0 fee receives the maximum points.

7.5%

Frequently asked questions

When you use a credit card to make a transaction in another currency, it will be converted back to Australian dollars based on the exchange rate that's applicable for your credit card. For example, if you spent US$100 and the exchange rate was US$0.67 to AUD$1, this transaction would show up on your credit card account as AUD$148.85 (to the nearest cent).

Sometimes when you're travelling, a business will give you the option of paying in the local currency or in Australian dollars. If you choose to pay in Australian dollars, the transaction will be processed using Dynamic Currency Conversion. This usually costs you a lot more than paying in the local currency.

According to the ACCC, this is because overseas banks "usually add a mark-up to the exchange rate". And depending on your credit card, you could still be charged an international transaction fee.

It's often useful to have a couple of different ways to spend money when you're travelling. As well as a credit card, you may want to buy foreign currency before you go or take a debit card in case you end up needing cash. Another option is getting a prepaid travel card that lets you spend money in different currencies so you can avoid foreign transaction fees.

A good credit is always one that matches your needs. If you plan to travel overseas or shop internationally, a no foreign transaction fee credit card is really useful.

But if your main interest is earning frequent flyer points, spending locally while avoiding big fees or paying off existing credit card debt you are probably looking for a different type of card.

Richard Whitten is Finder’s Senior Money Editor, with over eight years of experience in home loans, property, credit cards and personal finance. His insights appear in top media outlets like Yahoo Finance, Money Magazine, and the Herald Sun, and he frequently offers expert commentary on television and radio, helping Australians navigate mortgages and property ownership. Richard started his career in education and textbook publishing in South Korea. He holds multiple industry certifications, including a Certificate IV in Mortgage Broking (RG 206) and Tier 1 and Tier 2 certifications (RG 146), as well as a Bachelor of Education from the University of Sydney and a Graduate Certificate in Communications from Deakin University.

See full bio

Richard's expertise

Richard

has written

764

Finder guides across topics including:

I don’t want this to come cross as naive or unrealistic. I do need the help of somebody who is far more informed and educated in this realm of things.

I’ve never taken credit, except for my school HECS, which is a system used in Australia for Uni goers who do not pay upfront. It’s a commonly used form of borrowing from the gov., and then repaying when one has a full time job. There is interest.

I’ve re payed a small amount.

Though, my current predicament is this. I received a Working/Holiday Visa for France. I’m from Australia. I’ve been with Commonwealth since 2009, I think, and before leaving for France, I got an ANZ travel card. All was well and good.

However. Now, I’m travelling and there is less than 10€ left in my bank account. I don’t have a form of income, since I was working in a restaurant and quit before travelling through Europe. I refuse to return to Australia, it’s too early, and I’ve not yet seen fashion week in Paris. So. What do you suggest? What are my options?

I searched for credit cards online, and figured 28 degrees was the best, though I haven’t applied since I have no form of current income, and I don’t want to cause any damage to my current score. I don’t know anyone who is willing to take the credit card under their name and share it with me.

What do you suggest? Would I be able to take any form of credit with Commonwealth or ANZ since I already have 2 cards with them? Or, am I able to, in some way, receive a loan from a company?

I appreciate any response, though I hope it’s not a dead-end.

By the way, I’m a 23 year old female, if that is of any importance.

Thank you, deeply.

Rose

Finder

JacobMarch 13, 2014Finder

Hi, Rose.

I’m sorry to be the bearer of bad news, but without a form of income, you’re stuck in a tight spot.

When I was in Europe, I was in a similar situation to yourself. I had a credit card with St.George and I went to apply for a credit limit increase. They had been my banking institution since birth. Although I was employed full time on a working visa (teaching English as part of a government program), they could not offer me anything since I did not have an Australian taxable income which could be verified by the bank.

I hope this helps and best of luck. I hope you make it to fashion week.

Regards.

Jacob.

ReineMarch 4, 2014

How much would it cost me to withdraw £1000 ($. 2000) from my ANZ credit card while in the UK?

Finder

JacobMarch 5, 2014Finder

Hi, Reine.

Thanks for your question.

ANZ currently charge a foreign currency conversion fee (overseas transaction fee) of 3% of the total value of the transaction when carrying out a transaction in a currency other than Australian dollars. This applies to Visa, MasterCard and American Express cards. There will also be a international ATM withdrawal fee, which is currently $5 charged by ANZ, and a local ATM operator fee charged by the ATM owner. The local ATM fee will be advised at the time of the transaction.

I hope this helps. Have a good trip.

dennisFebruary 22, 2014

Don’t you just love the fact regardless of the amount,all these parasites give you a lousy 4or 5 % over twelve months,but charge you 3% in a blink of an eye to give you your money which they have been using to make more money from in the first place.Their is no limit to a gluttons hunger?

Finder

JacobFebruary 24, 2014Finder

Hi Dennis,

These types of comments/questions aimed at encouraging discussion among users belong in our forum. Please feel free to post away.

Cheers,

Jacob

BenJanuary 28, 2014

Was

Wondering what the conversion fee is when exchanging aus dollar to indoisian rupiah

Finder

ShirleyJanuary 29, 2014Finder

Hi Ben,

Thanks for your comment.

You can see the currency conversion fee of each credit card in our reviews. When you’re reading a review, please refer to the ‘Foreign Currency Conversion Fee’ row in the product table.

Cheers,

Shirley

NaughtyNannyJanuary 22, 2014

I applied for a Bankwest Platinum on this site for overseas travel and was rejected, their letter stated I was a bad credit risk. I believe this is now a black mark against me. I own my own home drive a current year ford ranger 4×4, own a 35 grand boat and am a self funded retiree. I have had a 28 degree MasterCard with a 10 grand limit for 15 years which was excellent for overseas travel. The only reason i left them was because i could not identify myself on the phone after clearing myself on the automation pin change (I made a mistake and hung up on myself) To say that I am a bad debt risk after not doing a legislated credit check is both very bad for them and scandalous against me. Be wary of what you apply for anywhere.

Compare introductory credit card offers that give you bonus rewards points, 0% p.a. balance transfers, interest-free periods and waived annual fees when you sign up for a new card.

Compare the best Qantas frequent flyer credit cards based on bonus point offers, points per $1 spent, rates, fees and other features so you can find a card that works for you.

Calculate how much you're paying in interest based on your current credit card repayments and discover how much you should pay each month to meet your financial goal.

Important information about this website

Finder makes money from featured partners, but editorial opinions are our own.

Finder is one of Australia's leading comparison websites. We are committed to our readers and stand by our editorial principles.

We try to take an open and transparent approach and provide a broad-based comparison service. However, you should be aware that while we are an independently owned service, our comparison service does not include all providers or all products available in the market.

Some product issuers may provide products or offer services through multiple brands, associated companies or different labeling arrangements. This can make it difficult for consumers to compare alternatives or identify the companies behind the products. However, we aim to provide information to enable consumers to understand these issues.

We make money by featuring products on our site. Compensation received from the providers featured on our site can influence which products we write about as well as where and how products appear on our page, but the order or placement of these products does not influence our assessment or opinions of them, nor is it an endorsement or recommendation for them.

Products marked as 'Top Pick', 'Promoted' or 'Advertisement' are prominently displayed either as a result of a commercial advertising arrangement or to highlight a particular product, provider or feature. Finder may receive remuneration from the Provider if you click on the related link, purchase or enquire about the product. Finder's decision to show a 'promoted' product is neither a recommendation that the product is appropriate for you nor an indication that the product is the best in its category. We encourage you to use the tools and information we provide to compare your options.

Where our site links to particular products or displays 'Go to site' buttons, we may receive a commission, referral fee or payment when you click on those buttons or apply for a product.

When products are grouped in a table or list, the order in which they are initially sorted may be influenced by a range of factors including price, fees and discounts; commercial partnerships; product features; and brand popularity. We provide tools so you can sort and filter these lists to highlight features that matter to you.

Please read our website terms of use and privacy policy for more information about our services and our approach to privacy.

We update our data regularly, but information can change between updates. Confirm details with the provider you're interested in before making a decision.

How likely would you be to recommend Finder to a friend or colleague?

0

1

2

3

4

5

6

7

8

9

10

Very UnlikelyExtremely Likely

Required

Thank you for your feedback.

Our goal is to create the best possible product, and your thoughts, ideas and suggestions play a major role in helping us identify opportunities to improve.

Morning,

I don’t want this to come cross as naive or unrealistic. I do need the help of somebody who is far more informed and educated in this realm of things.

I’ve never taken credit, except for my school HECS, which is a system used in Australia for Uni goers who do not pay upfront. It’s a commonly used form of borrowing from the gov., and then repaying when one has a full time job. There is interest.

I’ve re payed a small amount.

Though, my current predicament is this. I received a Working/Holiday Visa for France. I’m from Australia. I’ve been with Commonwealth since 2009, I think, and before leaving for France, I got an ANZ travel card. All was well and good.

However. Now, I’m travelling and there is less than 10€ left in my bank account. I don’t have a form of income, since I was working in a restaurant and quit before travelling through Europe. I refuse to return to Australia, it’s too early, and I’ve not yet seen fashion week in Paris. So. What do you suggest? What are my options?

I searched for credit cards online, and figured 28 degrees was the best, though I haven’t applied since I have no form of current income, and I don’t want to cause any damage to my current score. I don’t know anyone who is willing to take the credit card under their name and share it with me.

What do you suggest? Would I be able to take any form of credit with Commonwealth or ANZ since I already have 2 cards with them? Or, am I able to, in some way, receive a loan from a company?

I appreciate any response, though I hope it’s not a dead-end.

By the way, I’m a 23 year old female, if that is of any importance.

Thank you, deeply.

Rose

Hi, Rose.

I’m sorry to be the bearer of bad news, but without a form of income, you’re stuck in a tight spot.

When I was in Europe, I was in a similar situation to yourself. I had a credit card with St.George and I went to apply for a credit limit increase. They had been my banking institution since birth. Although I was employed full time on a working visa (teaching English as part of a government program), they could not offer me anything since I did not have an Australian taxable income which could be verified by the bank.

I hope this helps and best of luck. I hope you make it to fashion week.

Regards.

Jacob.

How much would it cost me to withdraw £1000 ($. 2000) from my ANZ credit card while in the UK?

Hi, Reine.

Thanks for your question.

ANZ currently charge a foreign currency conversion fee (overseas transaction fee) of 3% of the total value of the transaction when carrying out a transaction in a currency other than Australian dollars. This applies to Visa, MasterCard and American Express cards. There will also be a international ATM withdrawal fee, which is currently $5 charged by ANZ, and a local ATM operator fee charged by the ATM owner. The local ATM fee will be advised at the time of the transaction.

I hope this helps. Have a good trip.

Don’t you just love the fact regardless of the amount,all these parasites give you a lousy 4or 5 % over twelve months,but charge you 3% in a blink of an eye to give you your money which they have been using to make more money from in the first place.Their is no limit to a gluttons hunger?

Hi Dennis,

These types of comments/questions aimed at encouraging discussion among users belong in our forum. Please feel free to post away.

Cheers,

Jacob

Was

Wondering what the conversion fee is when exchanging aus dollar to indoisian rupiah

Hi Ben,

Thanks for your comment.

You can see the currency conversion fee of each credit card in our reviews. When you’re reading a review, please refer to the ‘Foreign Currency Conversion Fee’ row in the product table.

Cheers,

Shirley

I applied for a Bankwest Platinum on this site for overseas travel and was rejected, their letter stated I was a bad credit risk. I believe this is now a black mark against me. I own my own home drive a current year ford ranger 4×4, own a 35 grand boat and am a self funded retiree. I have had a 28 degree MasterCard with a 10 grand limit for 15 years which was excellent for overseas travel. The only reason i left them was because i could not identify myself on the phone after clearing myself on the automation pin change (I made a mistake and hung up on myself) To say that I am a bad debt risk after not doing a legislated credit check is both very bad for them and scandalous against me. Be wary of what you apply for anywhere.