Car insurance with storm and hail cover

All comprehensive car insurance policies include coverage for storms and hail damage as standard.

If you have comprehensive car insurance, then yes, you will be covered for hail damage. In fact, you will be covered for all damage related to storms.

Keep in mind though, you will likely have to pay your standard excess when you make a claim for hair or storm damage.

If you have a third party fire and theft or third party property damage policy, you will not be covered for hail damage.

If your car has existing hail damage, it is still possible to get car insurance. Your insurer will likely just exclude your existing damage from the cover so you can’t make a claim to repair that. But any other damage that happens going forward will be covered.

When you’re filling in your quote form, your insurer will ask you if your car has any existing damage. At this point, you can submit the details of your existing hail damage. Based on your answers, the insurer will decide if they still want to offer you cover or not.

If you find this process confusing to do online then you might be better off calling the insurer to chat to them about your options.

Typically, no. You’re only covered by your insurer for damage that occurs after you’ve taken out a policy. Any damage that existed before that is usually listed as an exclusion and claims .

Do this as soon as possible. If your area has been hit badly by a hail storm, it's likely there'll be thousands of other people claiming too. The sooner you get in touch, the sooner they can get started on your claim.

Take photos of any damage to your car, as well as any damage in the surrounding area. Make notes about what happened, including the time and date.

Provide the detailed evidence you gathered after your car was damaged. Agree to meet with any experts or claims assessors your insurance company assigns. Don't make any repairs until you have your insurer's permission.

Depending on the insurer your claim options may be to submit online, via an app, mail or in-person. Your insurer will explain their preferred method.

Your insurer has 10 business days to respond with their decision or to let you know if they need more time. If they do need more time, they have to let you know what else they need from you, and to give you updates on how your claim is progressing.

Although your car insurance company has 10 business days to respond to your claim, don't be surprised if it takes a little longer. This is because, when a major hail storm hits, it's usually followed by a huge influx in claims – which leads to a backlog for insurers.

Never carry out repairs to the car without your insurer's authorisation. In some cases, to allow the car to be driven immediately after an accident, your insurer may agree to essential repairs.

If your claim is accepted, your car insurer may:

You can also contact the Insurance Council of Australia if you have any general inquiries about the claims process. It's likely the organisation will activate its risk and disaster response helpline - 1800 734 621 - to answer any questions people might have.

If you're unhappy with how your insurer is treating you, get in touch with the Australian Financial Complaints Authority (AFCA) on 1800 931 678.

"If your car has been damaged by a storm and you can’t drive it, you may not have to tough it out car-less while your repairs are happening. Many comprehensive car insurance policies include the use of a hire car while your car is out of action. Check the details of your product disclosure statement to know what you’re entitled to."

We currently don't have that product, but here are others to consider:

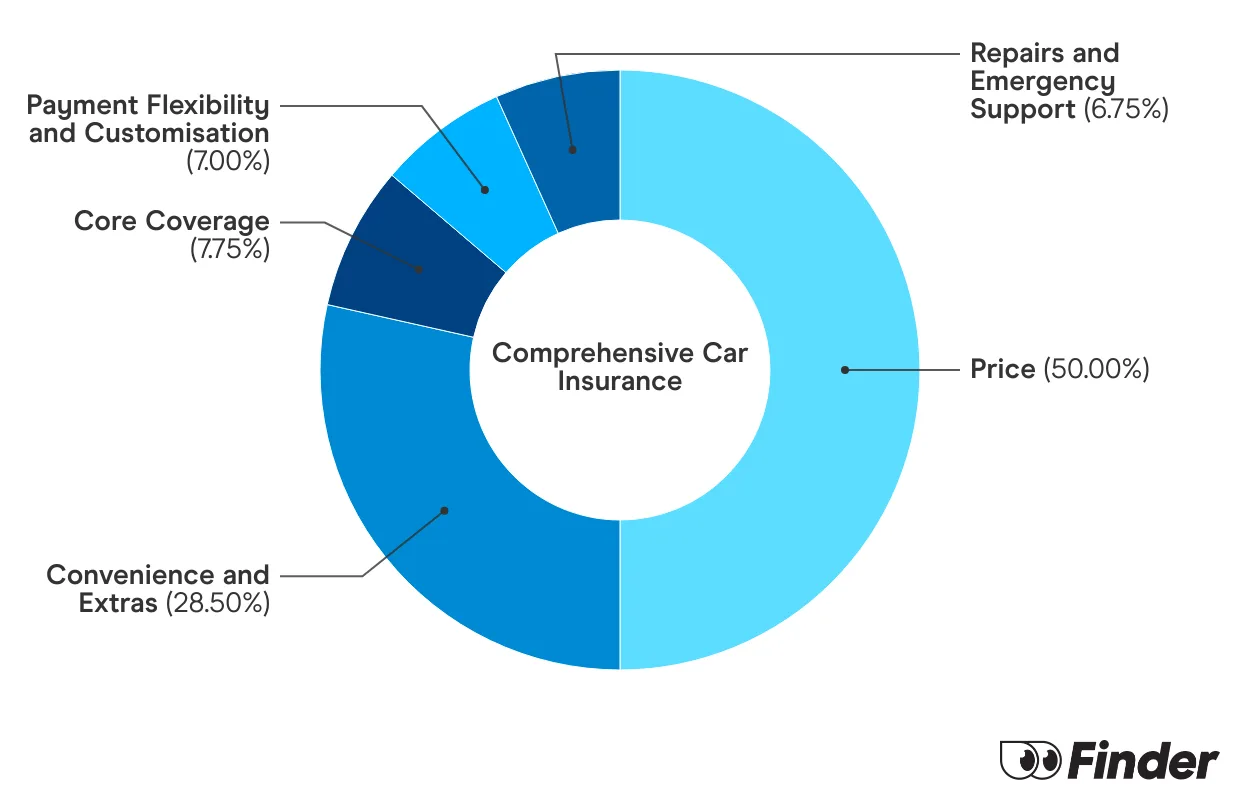

How we picked theseWe analyse over 30 car insurance products across insurance providers, and rate each one for price and features. We collect up to 36 quotes per product, for male and female drivers in New South Wales, Victoria, Queensland, South Australia, Tasmania and Western Australia. Quotes are collected for 20 year olds, 30 year olds and 60 year olds, assuming an excess of $850 for a 2020 Toyota Corolla 4 door sedan model, with an average 15,000 kms driven each year. While we are not allowed to display actual quotes, our Finder Score aims to serve as an indicative guide to how cost and feature competitive a product might be for you.

Our feature score assesses each product for more than 15 features across loss and damage coverage, repairs and assistance coverage, personal items coverage and policy coverage. Features we assess include but are not limited to legal liability, essential repairs, new car replacement, car hire events, roadside assistance, agreed or market value, windscreen damage and natural disaster coverage.

ALDI car insurance offers comprehensive car insurance with really solid benefit limits.

ahm offers a decent level of coverage but might not suit drivers on a tighter budget.

RACQ offers strong benefits and service, but drivers can expect to pay higher premiums and a joining fee.

With 5% off for seniors, budget-friendly policies, and some uncommon benefits, Australian Seniors is worth considering.

ANZ car insurance is typically more expensive than average, but it does have some generous benefits.

Australian Unity car insurance, underwritten by Allianz, offers two levels of cover, the freedom to choose your own repairer and an easy 24-hour claims service.

APIA car insurance is issued by AAI Limited and offers 3 levels of cover, a range of discounts and a lifetime guarantee on repairs.

Coles car insurance is a budget-friendly option for young people, but older drivers may be able to find cheaper cover elsewhere.

With a higher-than-average price but no particularly impressive benefits, Allianz was outperformed by many other car insurers in the 2024 Finder Insurance Awards.

Explore our analysis and see how you can find the best car insurance for your needs.