Pay your closing balance in full by the due date to avoid interest and protect your credit score.

Carefully review all transactions and new charges to detect errors or fraudulent activity promptly.

Interest-free days begin on statement day one; pay your full closing balance to utilise them.

It's important to understand how to read your credit card statement. This way you can to keep track of your spending, make repayments on time, avoid fees and interest charges, and catch any dodgy transactions.

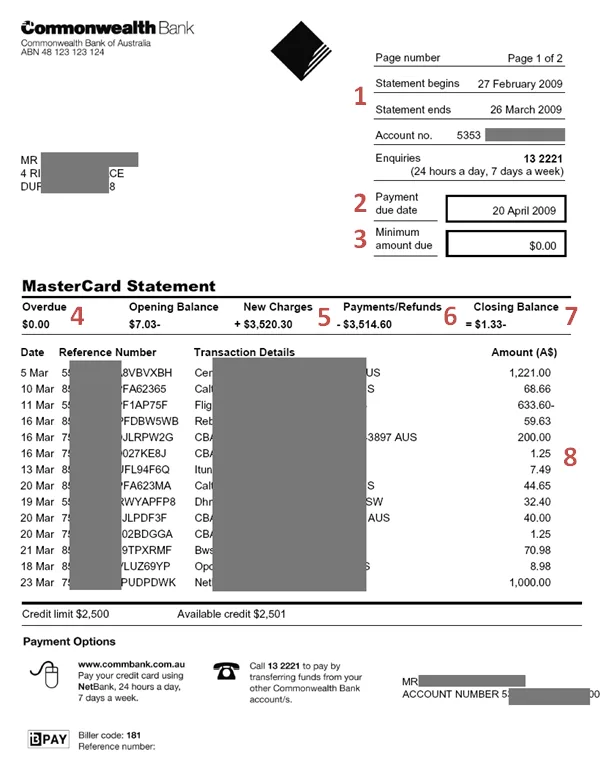

10 key features on your credit card statement

Below we've outlined the major features of a credit card statement.

Statement period

Payment due date

Minimum amount due

Overdue amount

New charges

Payments/refunds

Closing balance

Transactions

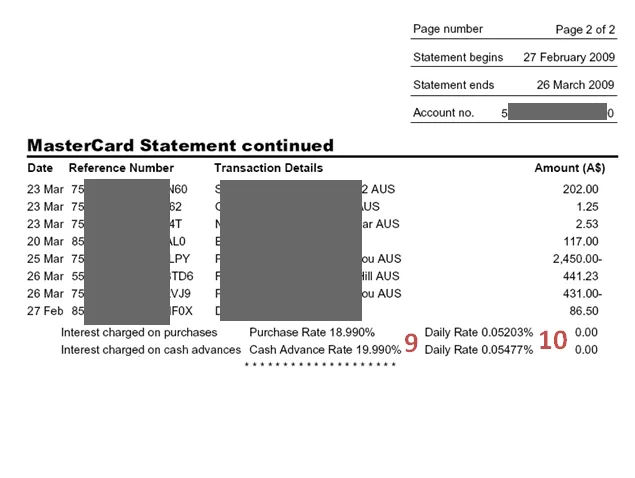

Daily rate (see second image down the page)

Reward points (see second image down the page)

1. Statement period

Your statement period is usually listed in the top right-hand corner of your statement. Statement periods are typically 30-day periods.

If a credit card offers interest-free days, these days start from day 1 of the statement period.

Cards can come with up 55 days interest-free. From day 1 of the statement period you have 55 days before interest is charged on your card spending. If you make a purchase on day 2 of the statement period you have 54 days interest free. On day 3, 53 days.

Example

Let's assume that your card provides up to 55 interest-free days and the statement period is from 27 February to 26 March. The interest-free period for this statement period would end on 23 April.

In this example, if you make a purchase on 27 February, you can make use of 55 interest-free days. If you make a purchase on 26 March, you get 28 interest-free days.

You have to make the minimum payment by the payment due date. You can pay off the entire balance, or more than the minimum, before the due date.

But you have to pay at least the minimum repayment by this date. If you don't make this payment on time your credit score will be affected and you may have to pay a fee.

Note. If you're just struggling to repay that month, you can also request an extension. Most banks offer financial hardship assistance, so contact your card issuer directly to discuss your options.

3. Minimum amount due (or minimum payment)

When using a credit card, you must pay a minimum amount each month. The minimum repayment is usually between 2-3% of your outstanding balance.

You should aim to pay off more than the minimum if you can. Because you will get charged interest on your unpaid card balance. The longer it takes you to pay off your balance, the more interest you pay.

4. Overdue

If you've paid your bill late or paid less than the minimum, the amount you're yet to repay will be detailed in the "overdue" section of your statement.

Overdue credit card bills collect fees and interest that increases your debt. It can also hurt your credit score. Overdue statements are a red flag to lenders and could reduce your chance of getting loans and cards in the future.

5. New charges

This is a summary of the total amount of money charged to the card during the statement period. Look at the new charges to make sure the total amount matches up with the transactions that you've made. This can help ensure there aren't any errors on your statement (such as fraudulent transactions or double charges).

6. Payments/Refunds

This is the total of all the payments you have made towards the card, along with any refunds, during the statement period. Some refunds can take a few weeks to process.

7. Closing balance

This amount refers to how much you owe on your credit card account in total. If you pay more than you owe, this figure goes into negative.

While you're only obligated to pay the minimum payment each month, you should aim to pay as close to the closing balance as possible. If you pay the closing balance in full, you can avoid interest.

8. Transactions

This list details all the transactions you've made on that card during that statement period. It should include the date of the transaction, its reference code, the type of transaction and the dollar amount.

It's wise to look over your transaction history to make sure that you haven't been charged incorrectly or fraudulently in the previous statement period.

9. Daily rate

While banks usually present the interest rate as an annual percentage, it's actually charged on your transactions on a daily basis. So you can use the daily rate to see how much your balance is collecting in interest each day, including your purchases, balance transfers and cash advances. Most transactions, aside from cash advances, usually don't start accruing interest until after the statement period ends, though.

10. Reward points

You can expect these details only if you use a rewards credit card or frequent flyer credit card. If you do, your statement should inform you of points earned during the statement period, the total number of points in your account, and points redeemed during this period.

Expert insight: What if I see unexpected charges on my card?

"Scams are increasingly common and sophisticated, often using phishing emails and fake websites to steal personal information. When you spot an unrecognised transaction on your credit card statement, first double-check the details and contact the merchant if necessary. If the transaction is still unrecognised, report it to your card issuer immediately and dispute the charge. To prevent such incidents, secure your card information, use strong passwords, enable transaction alerts, and only provide card details to trusted websites. Regularly reviewing your credit card statements helps catch any discrepancies early and maintain financial security."

How to manage errors on your credit card statement

While your credit card statement should usually be accurate, there are some instances where you might spot an error. This could be a fraudulent transaction or a mistake from a merchant.

If you do spot an error on your credit card statement, contact your card provider to report and resolve the issue.

Unfortunately, the answer to this is no. However, by doing so you can look forward to clutter-free space and you can also do your bit to save the environment. Most banks issue electronic credit card statements, so this might be an easier way to manage your statements.

Credit card providers in Australia issue statements on a monthly basis. Make sure you contact your bank if you haven't received your credit card statement around the time you usually would in the month.

This might be because you have an outstanding balance in your account from the previous billing cycle. Bear in mind that you have to pay your account’s closing balance in full before each due date if you wish to take advantage of your card’s interest-free days.

All transactions are listed within one statement. As the primary cardholder, you're liable for any transactions made with any additional cards. This is why it's important to check your statement and keep track of all transactions being made.

Rebecca Pike is Finder’s money editor, with over 7 years of experience in mortgages and personal finance. A frequent TV and radio commentator, she frequently appears on Sunrise and 7News, Today and 9News, as well as Sky News, Channel 10 and across radio and print. Rebecca previously served as Editor of Mortgage Professional Australia. She has a Master’s degree in Journalism as well as ASIC-recognised certifications in Tier 1 Generic Knowledge and Tier 2 General Advice Deposit Products, which comply with ASIC guidelines.

See full bio

Rebecca's expertise

Rebecca

has written

285

Finder guides across topics including:

Richard Whitten is Finder’s Senior Money Editor, with over eight years of experience in home loans, property, credit cards and personal finance. His insights appear in top media outlets like Yahoo Finance, Money Magazine, and the Herald Sun, and he frequently offers expert commentary on television and radio, helping Australians navigate mortgages and property ownership. Richard started his career in education and textbook publishing in South Korea. He holds multiple industry certifications, including a Certificate IV in Mortgage Broking (RG 206) and Tier 1 and Tier 2 certifications (RG 146), as well as a Bachelor of Education from the University of Sydney and a Graduate Certificate in Communications from Deakin University.

See full bio

Richard's expertise

Richard

has written

776

Finder guides across topics including:

Hi, My Visa CC statement just arrived by post yet my online closing balance shows a lot less, which one should I pay?

Cheers, John

Finder

JonathanApril 15, 2015Finder

Hi John, thanks for your inquiry!

Your online statement will generally be the most accurate/ updated record and more reliable to pay to. It may be useful to check the payment records on the postal record and compare that to the online statement. There is a possibility that your credit card has had some pending or new transactions between the time your postal statement was mailed and when you have received it.

Cheers,

Jonathan

JaswantAugust 13, 2013

How can I know my credit card statement?

Finder

JacobAugust 14, 2013Finder

Hi Jaswant.

You will receive a statement a month after opening the account. If you want to keep track of purchases before a statement is sent out to you in the mail. You can check and manage your account online through your lender’s online banking facility.

Thanks for your question.

ChristopherJuly 20, 2013

Do the things you purchase end up on your credit card statement?

Finder

JacobJuly 20, 2013Finder

Hi Christopher. Thanks for your question. Your credit card statement will show you all your transactions for the month. This includes purchases and cash advances. Statements come in the mail but you elect to receive them electronically. Jacob.

MarshaMay 30, 2013

Is the opening balance the one you pay?

Finder

JacobMay 30, 2013Finder

HI Marsha. Thanks for your question. You will need to pay all balances eventually if you want to get out of debt. But typically, the opening balance will have the card’s annual fee (if applicable) and any transactions you’ve made in the first month. You will need to make at least the minimum monthly repayment to stop your account from going in to arrears. Jacob.

Compare credit cards that give you an outcome within 60 seconds of when you submit your application online and find out how to increase your chances of getting this type of "instant" credit card approval.

Compare the best Qantas frequent flyer credit cards based on bonus point offers, points per $1 spent, rates, fees and other features so you can find a card that works for you.

When you apply for a credit card online, you could receive a response within 60 seconds. Find out how you to find a card that you're eligible for and increase your chances of approval.

Find out how you can keep your overseas spending costs down by comparing credit cards with no foreign transaction fees and no currency conversion fees.

Important information about this website

Finder is a comparison service. We do not compare every product or every provider in the market.

We make money through commercial arrangements with some of the providers on this site. Products marked 'Sponsored', 'Promoted', 'Featured' or 'Advertisement' appear as a result of a commercial arrangement.

Our editorial content, product reviews and any 'Top Pick' designations are prepared independently of these commercial arrangements.

The default order of products in our tables can be influenced by commercial arrangements. You can re-sort or filter using the controls above each table.

Some content on this site may be generated or supported by AI tools. You should verify details directly with the provider.

Finder is one of Australia's leading comparison websites. We are committed to our readers and stand by our editorial principles.

Our comparison service does not include every product or every provider in the market. Some product issuers offer their products under multiple brands or through associated companies. Where we can, we identify the underlying issuer so you can compare like with like, but you should always check with the provider directly to confirm which brand you are dealing with.

Finder is a comparison website and an intermediary. We are not a product issuer and we do not provide personal financial or credit advice. When you click a link to a product, or apply for a product through our site, you deal directly with the product issuer. We may receive a referral fee, commission or other payment from the issuer if you click through, apply or take out a product. We describe these arrangements in more detail under 'How we make money' below.

Product features, fees, terms and eligibility criteria are set by the product issuer and may change. We rely on information supplied by issuers when we present product details on our site. Before you apply for or take out any product, you should confirm the details directly with the issuer.

We earn revenue from Finder in four principal ways:

Referral fees and commissions. When you click a product link, complete an enquiry form or apply for a product through our site, we may receive a referral fee, commission or other payment from the product issuer. We may also receive payment based on the volume of leads or conversions we send to an issuer.

Sponsored placements. Products marked 'Sponsored', 'Promoted', 'Featured' or 'Advertisement' appear as a result of a commercial arrangement between Finder and the issuer. These labels always indicate a paid placement. We do not use them for editorial choices.

Display advertising. Banner advertising, newsletter advertising and similar display ads on our site are paid by advertisers.

Content sponsorship. Some articles, videos and social media posts are sponsored by an issuer and are clearly labelled as such.

Our editorial opinions, product reviews and any 'Top Pick' designations are prepared independently of these commercial arrangements. A 'Top Pick' is an editorial choice made by our writers and editors based on the criteria described on each comparison page. A 'Top Pick' is not a personal recommendation and does not mean the product is appropriate for your circumstances.

If you would like to know whether we have a commercial arrangement with a specific product issuer, please contact us.

When products are grouped in a table or list, the default order can be influenced by commercial arrangements we have with product issuers. In some categories, sponsored or featured products appear in the top positions of the table by default, and are always labelled as such.

Other factors that influence default order include price, fees and features, and (where relevant) our editorial view of the product.

You can re-sort every comparison table using the controls above the table. You can filter by product features that matter to you. The order you see after re-sorting or filtering is not influenced by commercial arrangements.

Some content on this site is generated or supported by artificial intelligence tools, including our AI-powered assistant FinderBot. AI-generated content may contain errors. Please verify important information directly with the product issuer before making a financial decision. For more information about FinderBot, see the FinderBot Terms of Use and FinderBot Privacy Collection Notice.

Please read our website terms of use and privacy policy for more information about our services and our approach to privacy.

We update our data regularly, but information can change between updates. Confirm details with the provider you're interested in before making a decision.

Our goal is to create the best possible product, and your thoughts, ideas and suggestions play a major role in helping us identify opportunities to improve.

Hi, My Visa CC statement just arrived by post yet my online closing balance shows a lot less, which one should I pay?

Cheers, John

Hi John, thanks for your inquiry!

Your online statement will generally be the most accurate/ updated record and more reliable to pay to. It may be useful to check the payment records on the postal record and compare that to the online statement. There is a possibility that your credit card has had some pending or new transactions between the time your postal statement was mailed and when you have received it.

Cheers,

Jonathan

How can I know my credit card statement?

Hi Jaswant.

You will receive a statement a month after opening the account. If you want to keep track of purchases before a statement is sent out to you in the mail. You can check and manage your account online through your lender’s online banking facility.

Thanks for your question.

Do the things you purchase end up on your credit card statement?

Hi Christopher. Thanks for your question. Your credit card statement will show you all your transactions for the month. This includes purchases and cash advances. Statements come in the mail but you elect to receive them electronically. Jacob.

Is the opening balance the one you pay?

HI Marsha. Thanks for your question. You will need to pay all balances eventually if you want to get out of debt. But typically, the opening balance will have the card’s annual fee (if applicable) and any transactions you’ve made in the first month. You will need to make at least the minimum monthly repayment to stop your account from going in to arrears. Jacob.