These products offer the best value and outcomes considering various product features and price.

7+

Great

Competitive products within their group.

5+

Standard

But these products still offer reasonable value and have the basics sorted.

0+

Basic

Offering basic cover with limited features or higher pricing.

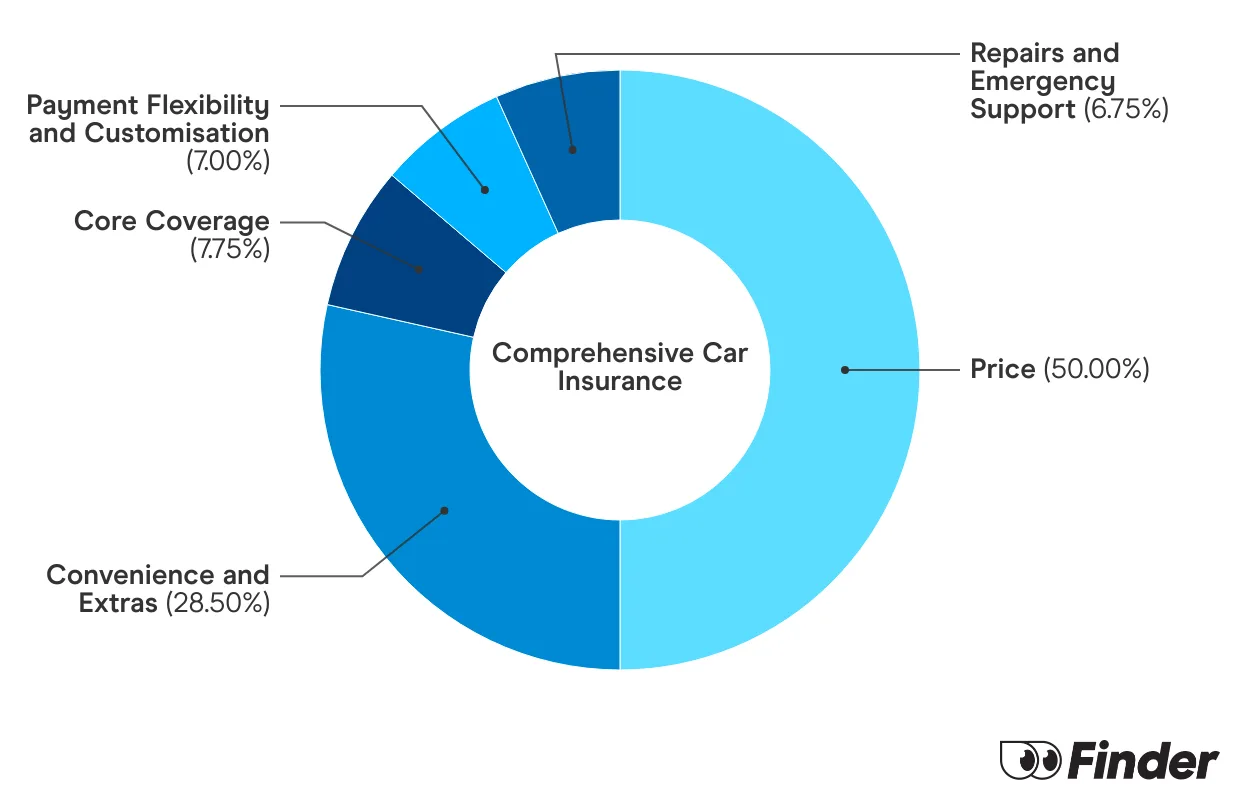

Finder Score for car insurance

We analyse over 30 car insurance products across insurance providers, and rate each one for price and features. We collect up to 36 quotes per product, for male and female drivers in New South Wales, Victoria, Queensland, South Australia, Tasmania and Western Australia. Quotes are collected for 20 year olds, 30 year olds and 60 year olds, assuming an excess of $850 for a 2020 Toyota Corolla 4 door sedan model, with an average 15,000 kms driven each year. While we are not allowed to display actual quotes, our Finder Score aims to serve as an indicative guide to how cost and feature competitive a product might be for you.

Our feature score assesses each product for more than 15 features across loss and damage coverage, repairs and assistance coverage, personal items coverage and policy coverage. Features we assess include but are not limited to legal liability, essential repairs, new car replacement, car hire events, roadside assistance, agreed or market value, windscreen damage and natural disaster coverage.

In many cases, standard car insurance can cover 4x4s. You generally only need to consider specialised 4WD insurance if you want to go off-road or have modified your vehicle. In that case, you’ll need to get the okay from your insurer before you start adventuring.

What is covered by specialised off-road 4WD car insurance?

Specialised off-road car insurance policies are often largely equivalent to comprehensive car insurance with a few additional features. This may include:

Full cover anywhere in Australia

Comprehensive cover of accessories and modifications

Extended personal effects cover, to include items even while they are not necessarily inside the vehicle

Cover while your vehicle is in transit, including being loaded or unloaded from boats or trains

Includes cover of off-road recovery costs, for recovering an undriveable vehicle

Trailer cover, often included automatically and sometimes as an extra

Before you can get a quote, you’ll generally need to discuss it with an insurer and do a more in-depth application.

This is not only because of modifications, but also because you generally need to explicitly mention to insurers that you’ll be taking it off road, what kind of driving you do and how frequently you do it.

What additional options are there?

The optional add-ons available will vary by insurer. If you go with a regular car insurer, you can expect to see the following add-ons:

Additional hire vehicle cover: Lets you get a replacement vehicle if you are unable to drive your vehicle due to damage from an insured event.

Excess free windscreen or window glass cover: Replacement of windscreen or window glass with no excess, following an insured event.

Optional roadside assistance: This won’t help off road, but can still be a useful optional extra to consider.

If you opt for a specialised 4x4 insurer, the optional add-ons are a bit more tailored to off-road activities, such as:

Additional off-road recovery costs: Lets you choose an additional cover amount for off-road recovery, like getting stuck somewhere.

Higher benefit limits for hire car cover: This is because it’ll cost you more to hire a replacement 4x4.

Cover for modifications and accessories: You’ll have to list what modifications and accessories you have and the insurer will let you know if they’re happy to cover you.

Transit cover: Cover for while your vehicle is being transported, like on a boat.

Finding the best car insurance for 4x4 off-roading

Given off-roading comes with its own set of risks, it’s wise to consider insurance that accounts for this. You might like to look for policies that will:

Cover you for beach and off-road driving. A regular car insurer may only cover you for while you’re on the road.

Additional off-road recovery costs: A regular insurer may only cover recovery costs for accidents that occurred on an actual road.

Accept your car modifications and cover them for a higher benefit limit: If you’ve put a decent chunk of money into modifying your vehicle, a specialised 4x4 insurer can help you make sure these modifications are properly insured.

FAQs

Yes, insuring a 4x4 can be more expensive than insuring a standard vehicle due to its off-road capabilities and potentially higher repair costs. That said, rates vary based on the model, usage, age of the car and the insurer.

Like any insurance, the cost varies from person to person and depends largely on what car you drive, your driving history, age, location and more. It's best to compare costs from multiple policies to get an idea of what an average cost could look like and find the best car insurance for your needs.

Yes, comprehensive car insurance typically covers damage to your 4x4, including off-road incidents, as long as the vehicle is being used within the policy terms. You should check if off-road cover is included in your policy.

The underwriter for Club 4x4 insurance is QBE Insurance (Australia) Limited. Club 4x4 specialises in insuring 4x4 vehicles and off-road activities.

The cheapest 4x4s to tax and insure are typically smaller, less powerful models like the Suzuki Jimny. These vehicles have lower running costs and are often cheaper to repair, therefore they're cheaper to insure.

Peta Taylor is a publisher at Finder, working across all of insurance. She's been analysing product disclosure statements and publishing articles for over 2 years. Peta is passionate about demystifying complex insurance products to help users make well educated decisions with confidence. Peta is part of Finder's insurance awards team and works alongside editorial and insights experts to bring users the best insurance products every year.

See full bio

Alexandra Koster was Finder's publisher for car, home and pet insurance. She has a Tier 1 certification in General Insurance, as well as a Bachelor of Arts in Film and Cultural Studies from the University of Sydney. Her hobbies include reading Product Disclosure Statements and deciphering complicated insurance lingo to help people save on their insurance so that they can spend their money on better things – like dogs.

See full bio

we were told on the grape vine 4×4 insurance will cover 5wheeler’s we do not take our vechile off road

Finder

JamesFebruary 23, 2022Finder

Hi John,

I would strongly encourage you to speak with your insurer directly before you get behind the wheel so that you know all the types of driving your insurance will cover you for.

Australian Unity car insurance, underwritten by Allianz, offers two levels of cover, the freedom to choose your own repairer and an easy 24-hour claims service.

With a higher-than-average price but no particularly impressive benefits, Allianz was outperformed by many other car insurers in the 2024 Finder Insurance Awards.

Explore our analysis and see how you can find the best car insurance for your needs.

Important information about this website

Finder is a comparison service. We do not compare every product or every provider in the market.

We make money through commercial arrangements with some of the providers on this site. Products marked 'Sponsored', 'Promoted', 'Featured' or 'Advertisement' appear as a result of a commercial arrangement.

Our editorial content, product reviews and any 'Top Pick' designations are prepared independently of these commercial arrangements.

The default order of products in our tables can be influenced by commercial arrangements. You can re-sort or filter using the controls above each table.

Some content on this site may be generated or supported by AI tools. You should verify details directly with the provider.

Finder is one of Australia's leading comparison websites. We are committed to our readers and stand by our editorial principles.

Our comparison service does not include every product or every provider in the market. Some product issuers offer their products under multiple brands or through associated companies. Where we can, we identify the underlying issuer so you can compare like with like, but you should always check with the provider directly to confirm which brand you are dealing with.

Finder is a comparison website and an intermediary. We are not a product issuer and we do not provide personal financial or credit advice. When you click a link to a product, or apply for a product through our site, you deal directly with the product issuer. We may receive a referral fee, commission or other payment from the issuer if you click through, apply or take out a product. We describe these arrangements in more detail under 'How we make money' below.

Product features, fees, terms and eligibility criteria are set by the product issuer and may change. We rely on information supplied by issuers when we present product details on our site. Before you apply for or take out any product, you should confirm the details directly with the issuer.

We earn revenue from Finder in four principal ways:

Referral fees and commissions. When you click a product link, complete an enquiry form or apply for a product through our site, we may receive a referral fee, commission or other payment from the product issuer. We may also receive payment based on the volume of leads or conversions we send to an issuer.

Sponsored placements. Products marked 'Sponsored', 'Promoted', 'Featured' or 'Advertisement' appear as a result of a commercial arrangement between Finder and the issuer. These labels always indicate a paid placement. We do not use them for editorial choices.

Display advertising. Banner advertising, newsletter advertising and similar display ads on our site are paid by advertisers.

Content sponsorship. Some articles, videos and social media posts are sponsored by an issuer and are clearly labelled as such.

Our editorial opinions, product reviews and any 'Top Pick' designations are prepared independently of these commercial arrangements. A 'Top Pick' is an editorial choice made by our writers and editors based on the criteria described on each comparison page. A 'Top Pick' is not a personal recommendation and does not mean the product is appropriate for your circumstances.

If you would like to know whether we have a commercial arrangement with a specific product issuer, please contact us.

When products are grouped in a table or list, the default order can be influenced by commercial arrangements we have with product issuers. In some categories, sponsored or featured products appear in the top positions of the table by default, and are always labelled as such.

Other factors that influence default order include price, fees and features, and (where relevant) our editorial view of the product.

You can re-sort every comparison table using the controls above the table. You can filter by product features that matter to you. The order you see after re-sorting or filtering is not influenced by commercial arrangements.

Some content on this site is generated or supported by artificial intelligence tools, including our AI-powered assistant FinderBot. AI-generated content may contain errors. Please verify important information directly with the product issuer before making a financial decision. For more information about FinderBot, see the FinderBot Terms of Use and FinderBot Privacy Collection Notice.

Please read our website terms of use and privacy policy for more information about our services and our approach to privacy.

We update our data regularly, but information can change between updates. Confirm details with the provider you're interested in before making a decision.

Our goal is to create the best possible product, and your thoughts, ideas and suggestions play a major role in helping us identify opportunities to improve.

we were told on the grape vine 4×4 insurance will cover 5wheeler’s we do not take our vechile off road

Hi John,

I would strongly encourage you to speak with your insurer directly before you get behind the wheel so that you know all the types of driving your insurance will cover you for.

Best wishes,

James