Car Insurance Renewal

Time for your car insurance renewal? Here’s everything you need to know.

If your car insurance policy is set to expire soon, it's a good time to think about renewing.

Whether you’re looking for a better deal or thinking about how you can renew, we’ve made an easy guide to navigate the important details.

You’ll likely get a renewal notice a few weeks before your policy is due to end. How you go about renewing policy will depend on the options available with your insurer and how you originally took out cover.

You’re going to want to find out how much your premiums are going up before you decide to renew.

Depending on the type and age of your car, your claims history, and whether or not you have a no claims discount, your new premium could be a lot more expensive than you expected. If you no longer feel like you’re getting the best bang for your buck, it might be time to find a new provider.

Our research found that there was a variation in average annual costs of almost $400 for comprehensive car insurance when looking at 37 different Australian insurers. Finding a good deal can save you a lot of money, but it’s important to understand what your current policy covers so you can easily compare apples to apples when you shop around.

If you’ve missed premium payments or violated the terms of your car insurance policy, there’s a chance your renewal will be declined. In that case, you have a few options to help you get coverage:

We currently don't have that product, but here are others to consider:

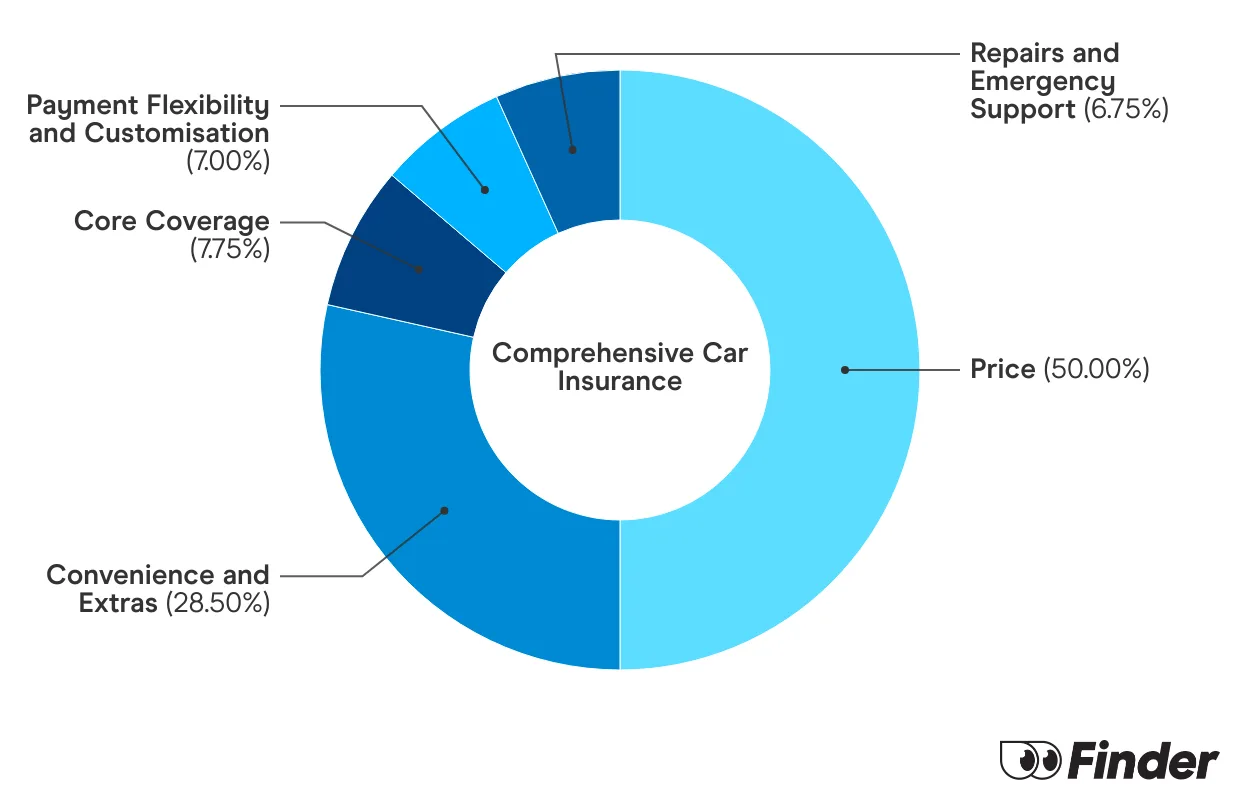

How we picked theseWe analyse over 30 car insurance products across insurance providers, and rate each one for price and features. We collect up to 36 quotes per product, for male and female drivers in New South Wales, Victoria, Queensland, South Australia, Tasmania and Western Australia. Quotes are collected for 20 year olds, 30 year olds and 60 year olds, assuming an excess of $850 for a 2020 Toyota Corolla 4 door sedan model, with an average 15,000 kms driven each year. While we are not allowed to display actual quotes, our Finder Score aims to serve as an indicative guide to how cost and feature competitive a product might be for you.

Our feature score assesses each product for more than 15 features across loss and damage coverage, repairs and assistance coverage, personal items coverage and policy coverage. Features we assess include but are not limited to legal liability, essential repairs, new car replacement, car hire events, roadside assistance, agreed or market value, windscreen damage and natural disaster coverage.

Here's a guide to getting affordable car insurance that will still cover the essentials.

How to stay up to date with your car insurance and avoid any hassle.

Read our guide to getting car insurance if you are an older driver looking for cover.

RACQ offers strong benefits and service, but drivers can expect to pay higher premiums and a joining fee.

With 5% off for seniors, budget-friendly policies, and some uncommon benefits, Australian Seniors is worth considering.

Find out what car insurance options are available for rideshare drivers, including Ubers.

Coles car insurance is a budget-friendly option for young people, but older drivers may be able to find cheaper cover elsewhere.

This article runs through the ins and outs of choosing a good third party property damage car insurance policy.

With a higher-than-average price but no particularly impressive benefits, Allianz was outperformed by many other car insurers in the 2024 Finder Insurance Awards.

Explore our analysis and see how you can find the best car insurance for your needs.

My son’s car renewal insurance has been declined, is there another insurer we can use for insurance.

Hi Susan,

I’m sorry to hear that.

You can compare a range of insurance providers here.

Before applying, please remind your son to read a policy’s Product Disclosure Statement (PDS) so that he’s aware of what he’s covered for, along with any exclusions or restrictions.

I hope this helps.

Regards,

James