These cards offer the best interest free options - either through a high number of interest free days or no interest on purchases, coupled with low fees.

7+

Great

Reasonable interest free options but may charge higher fees or have a lower number of interest free days.

5+

Standard

These cards may offer a lower number of interest free days or higher annual fees.

0+

Basic

While these cards may offer interest free days on new purchases, they may be more suited to other categories.

How can you get an interest-free credit card?

There are several ways to get 0% interest on your credit card:

0% interest monthly fee credit cards. You can get a credit card that offers a 0% interest rate permanently, but charges a monthly fee rather than an annual fee. Examples include the Wizitcard and the CommBank Neo. These cards have low credit limits and either charge a monthly fee, or require you to pay off your balance in full each month.

Credit cards with 0% introductory offers. Quite a few credit cards offer 0% interest on purchases as a special introductory offer. This is usually for 6 months, but some cards run for longer. After the intro period you'll be charged interest if you haven't paid off your balance in full each month.

Balance transfer offers. If you have multiple unpaid credit card balances and you're struggling to repay them, you can move the debts onto a new card with a 0% balance transfer offer. This is a special interest-free offer with a limited period, usually around 24 months.

Example: How much you can save with an interest-free card

Say you want to book a holiday for $3,000 and plan to pay $250 off the balance each month.

If you paid for it on a credit card with a 20.99% p.a. interest rate, it would take you just over a year (13.58 months) to pay off the balance and cost you around $397 in interest charges.

In comparison, if you had a credit card that offered 0% p.a. on purchases for 12 months and made the same $250 monthly repayments, you could pay off the holiday in 12 months with no interest charges.

What about credit cards with interest-free days?

Most credit cards offer a number of interest-free days for purchases. Basically, on the first day of your monthly credit card statement period you have up to 45 or even 55 days before interest is charged.

You have to pay the balance off before the interest-free days are up, or you get charged interest.

Pros and cons of interest-free credit cards

Pros

Save on interest costs. The obvious benefit of these cards is that you won't have to pay interest for the introductory period, or at all for monthly fee cards.

Pay off debt faster. By not paying interest on your balance, you'll be able to pay it off a lot faster because the amount won't be creeping up every month.

Cons

Revert rate. Some credit cards revert to a high interest rate after the interest-free offer ends.

Potentially higher fees. IF the card has a permanent 0% interest rate there will be a monthly fee. Over time, this fee will add up.

How can I get the best interest-free credit card?

Use the Finder Score. Use the table above and sort credit cards by Finder Score. We rank interest-free cards based on their features. The higher the score, the better the card.

Look for a card with a long 0% interest offer. Unless you've got some short-term purchases in mind, the longer the introductory period, the better. This gives you more time to make interest-free purchases and pay them back.

Factor in the cost of fees. Check if the card charges a monthly or annual fee (or both). Factor those in when looking at no-interest cards. Some cards also charge a fee if you don't pay your balance at the end of the month.

Keep an eye on the revert rate (if there is one). Cards with 0% interest rate offers revert to a higher rate once the intro period finishes. This can be above 20% in some cases. If you pay off your spending on time, you won't pay interest. But it's worth keeping an eye on.

Look at all the card's perks, features and benefits. Some credit cards, even 0% ones, can sometimes let you earn frequent flyer points or other rewards.

Our expert says: How to avoid interest on any credit card

"I've never paid a cent in credit card interest. And it's not because I have a 0% interest card. My credit card has a very high interest rate. But I pay it off on time each month and I never miss a payment. If you do this, any card is interest-free. Of course, if you can't pay off a card right away, a 0% card can really save you money. Just make a plan to pay it off. Don't forget and let the debt build up."

How do I find the right interest-free card for me?

I'm looking to make a big purchase and pay it off later. A card with a 0% introductory offer could give you 6 months or more before you have to pay the card off.

I want to cover a small amount of monthly spending and I want to pay off my spending in full each month. You could consider a card like the CommBank Neo. Just keep an eye on any fees, and remember these cards have quite low credit limits (around $1,000).

I have a large credit card debt and the monthly interest charges are killing me. You might want to look at a balance transfer credit card.

Frequently asked questions

Yes, you still need to pay at least the minimum amount required by the due date on each statement. This is usually around 2-3% of your account's closing balance, and the exact amount will be listed on your statement.

As an example, if you spent $3,000 on a credit card with a 3% minimum repayment amount, you'd need to repay at least $90 by the due date on your statement. Paying more than the minimum amount also helps you avoid ongoing debt and costs. You can use Finder's credit card repayment calculator to help figure out how much to pay each month and what's affordable for you.

If you don't pay at least the minimum amount listed on each monthly statement by the due date, some of the issues you could face include:

Late payment fees. If you miss a payment or make it after the statement's due date, you could be charged a late payment fee. Typically, it will cost around $10 to $30 on a standard credit card, or more on a charge card.

Cancelled promotional interest rates. The interest-free promotion may be cancelled if you don't make your minimum required payments. This penalty varies depending on the card, so make sure you check the terms of your offer.

Bad credit. Payment history is included on your credit report, which means late payments (or more extreme default accounts) could lower your credit score.

If you're struggling to make a repayment on time, contact your credit card provider as soon as possible so they can discuss repayment options based on your individual circumstances.

A 0% purchase rate offer lasts for an introductory period when you first get the new card. During this time, you won't be charged interest on your credit card purchases as long as you pay the minimum amount listed on each statement.

In comparison, a credit card with interest-free days gives you a period of time in each statement period when you can make purchases without being charged interest. Usually, you need to pay the total amount owed on each statement to be eligible for interest-free days.

For the length of the promotional 0% purchase rate period, standard interest-free days aren't necessary. If your card comes with interest-free days (for example, up to 55 days), you'll be able to take advantage of them when the promotional period ends.

With a 0% purchase rate credit card offer, the promotional 0% interest rate is available for a fixed time period. For example, let's say you get a card offering no interest for 12 months on purchases from when you activate the card.

If you make a purchase on the day you get (and activate) your card, you will have 12 months to pay it off before any interest is charged. If you make another purchase after 3 months, you will have 9 months remaining for the 0% interest period, and if you make a purchase 11 months after getting the card, you'll only have 1 month interest-free for that purchase. After that, the 12-month 0% interest offer will end and the standard purchase rate will apply to new purchases.

If you repay the total amount listed on your statement by the due date, you'll typically get an interest-free period for purchases. There is also a small range of credit cards in Australia that charge no interest ever, with a flat monthly fee instead, including:

CommBank Neo

Wizitcard

Yes, many Australian banks and lenders offer 0% interest credit cards, but they are usually for a set period – such as an introductory offer on purchases for 12 months, or on balance transfers for a year or two. The lender's ultimate goal is for you to keep the card after the 0% interest period and eventually start paying interest so they can turn a profit.

A 0% card is the same as any other form of credit, so it can impact your credit score if you miss payments or if you carry high balances from month to month, after the promotional period, and you're paying interest. Managing the card responsibly can benefit your credit score. For a deeper look at how credit cards can impact your finances, check out this guide on how credit cards work.

Interest-free credit cards can be a smart choice if you repay your balance within the promotional period, avoiding interest charges. They also give you the opportunity to build your credit rating and demonstrate that you can manage your debts.

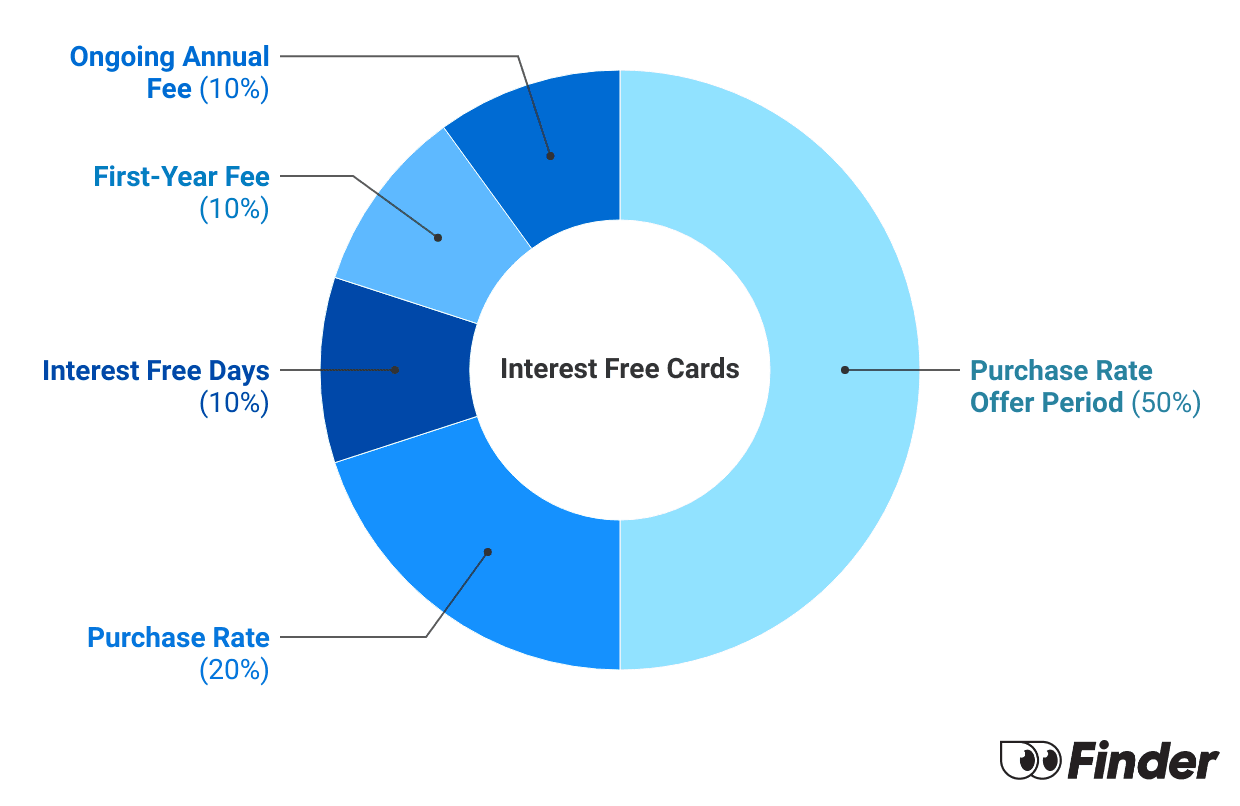

How Finder Score works for interest-free cards

Every month we carefully analyse over 250 credit card products and assess the features and benefits of each card. We assign a Finder Score out of 10 for each feature, and adjust the scores depending on the category.

To be included for the interest-free score, credit cards must:

Be available to general consumers

Have 0% interest rate (ongoing or offers) on new purchases

Credit card scores are category-specific (e.g. cashback, frequent flyer), meaning the same card will receive a different score within each category.

The score process is run by our insights and editorial team, independent of any commercial partnerships. Remember that Finder Score is just one factor to consider. Look at other aspects like fees, features, benefits and risks to make sure a product is suitable for you.

Feature

Definition

Assessment

Weight

Interest-Free Days

Number of days for no interest or fees on new purchases

Longer periods earn more points, up to market maximum. 0% purchase rate cards are assigned a default 30 days

10%

Purchase Rate Offer Period

Number of months for interest-free purchase rate

Higher the number of months, better the score

50%

First-Year Fee

Annual fee charged in the first year of ownership

Lower fees score higher. $0 fee receives the maximum points

10%

Ongoing Annual Fee

Annual fee charged from the second year onwards

Lower fees score higher. $0 fee receives the maximum points

Sarah is the author of How to Raise Rich Kids. With over 20 years of experience in property, finance and investment journalism, she is a trusted expert whose insights regularly appear across television, radio and print media, including Sunrise, Channel 7 News, Bloomberg and Yahoo! Finance. She has previously served as managing editor for Your Investment Property and Australian Broker. Her expert advice has been shared in the media over 4,000 times. Sarah holds a Bachelor’s degree in Communications and a Tier 1 Generic Knowledge certification, which complies with ASIC standards.

See full bio

Sarah's expertise

Sarah

has written

237

Finder guides across topics including:

Hi Faisal,

Credit cards can only be issued to people aged 18 and older if they meet the eligibility requirements. Some credit cards also allow people under 18 to be added as a secondary cardholder, but usually they need to be 16 or over. If you want a card for someone of a different age, you could consider debit cards for children or other prepaid cards that sometimes have lower age requirements. I hope that helps.

HayleyNovember 20, 2016

Hi,

I am needing an amount of $6800 and will be able to pay it back over a year. I will not be using the card for anything else but this one off overseas payment. What would be the best thing for me to do?

AnndyNovember 21, 2016

Hi Hayley,

Thanks for reaching out.

If you are looking for a credit card for overseas payment, you may want to consider reading our overseas transaction fees guide and find credit cards that may not charge foreign currency conversion fees.

You may also want to consider cards with 0% purchase interest rate. These cards allow you to save on interest payments during the promotional period in case you don’t intend to pay your balance in full at the end of the billing period.

Cheers,

Anndy

davidFebruary 15, 2016

if i pay out the balance in the interest free period can i then cancel the card with no fees.

Finder

JonathanFebruary 15, 2016Finder

Hi David, thanks for your inquiry!

Yes this is generally accepted across balance transfer credit cards. Once you have repaid your outstanding balance you can cancel the credit card anytime.

Cheers,

Jonathan

sharonSeptember 8, 2015

Good morning, I read with interest the balance transfer credit cards with no interest for a period of time. I, like many people have that problem of having not paid my CC on the due date and now have a big balance. I currently have an ANZ Platinum CC, can I apply for a balance transfer with no interest?

Thank you

Finder

JonathanSeptember 8, 2015Finder

Hi Sharon,

Thanks for your inquiry.

Balance transfers can be a great way to repay an outstanding credit balance interest-free. You may like to compare balance transfer offers and cards.Select ‘Go to Site’ to head over to their website to apply. Please ensure to read through the relevant product disclosure statement and terms and conditions to ensure that you got everything covered before you apply to the card.

Cheers,

Jonathan

BillyJune 12, 2015

Hi, I’m looking for a credit card to allow me to pay bills between payments from work. Would use it very little only when my funds are a bit tight. Any recommendations? Suggestions

Credit cards with high annual fees and rates usually come with extra features such as concierge services, complimentary insurance, and rewards programs. If you are after a credit card to use as a backup for your finances, some of these no frills options may be of interest.

You can select the “Go to Site” button of your preferred credit card to proceed with your application. You can also contact the provider if you have specific questions. A gentle reminder, please ensure to read through the relevant product disclosure statement and terms and conditions to ensure that you got everything covered before you apply.

I hope this has helped.

Thanks,

Sally

Important information about this website

Finder makes money from featured partners, but editorial opinions are our own.

Finder is one of Australia's leading comparison websites. We are committed to our readers and stand by our editorial principles.

We try to take an open and transparent approach and provide a broad-based comparison service. However, you should be aware that while we are an independently owned service, our comparison service does not include all providers or all products available in the market.

Some product issuers may provide products or offer services through multiple brands, associated companies or different labeling arrangements. This can make it difficult for consumers to compare alternatives or identify the companies behind the products. However, we aim to provide information to enable consumers to understand these issues.

We make money by featuring products on our site. Compensation received from the providers featured on our site can influence which products we write about as well as where and how products appear on our page, but the order or placement of these products does not influence our assessment or opinions of them, nor is it an endorsement or recommendation for them.

Products marked as 'Top Pick', 'Promoted' or 'Advertisement' are prominently displayed either as a result of a commercial advertising arrangement or to highlight a particular product, provider or feature. Finder may receive remuneration from the Provider if you click on the related link, purchase or enquire about the product. Finder's decision to show a 'promoted' product is neither a recommendation that the product is appropriate for you nor an indication that the product is the best in its category. We encourage you to use the tools and information we provide to compare your options.

Where our site links to particular products or displays 'Go to site' buttons, we may receive a commission, referral fee or payment when you click on those buttons or apply for a product.

When products are grouped in a table or list, the order in which they are initially sorted may be influenced by a range of factors including price, fees and discounts; commercial partnerships; product features; and brand popularity. We provide tools so you can sort and filter these lists to highlight features that matter to you.

Please read our website terms of use and privacy policy for more information about our services and our approach to privacy.

We update our data regularly, but information can change between updates. Confirm details with the provider you're interested in before making a decision.

Our goal is to create the best possible product, and your thoughts, ideas and suggestions play a major role in helping us identify opportunities to improve.

i need a credit card for all ages

Hi Faisal,

Credit cards can only be issued to people aged 18 and older if they meet the eligibility requirements. Some credit cards also allow people under 18 to be added as a secondary cardholder, but usually they need to be 16 or over. If you want a card for someone of a different age, you could consider debit cards for children or other prepaid cards that sometimes have lower age requirements. I hope that helps.

Hi,

I am needing an amount of $6800 and will be able to pay it back over a year. I will not be using the card for anything else but this one off overseas payment. What would be the best thing for me to do?

Hi Hayley,

Thanks for reaching out.

If you are looking for a credit card for overseas payment, you may want to consider reading our overseas transaction fees guide and find credit cards that may not charge foreign currency conversion fees.

You may also want to consider cards with 0% purchase interest rate. These cards allow you to save on interest payments during the promotional period in case you don’t intend to pay your balance in full at the end of the billing period.

Cheers,

Anndy

if i pay out the balance in the interest free period can i then cancel the card with no fees.

Hi David, thanks for your inquiry!

Yes this is generally accepted across balance transfer credit cards. Once you have repaid your outstanding balance you can cancel the credit card anytime.

Cheers,

Jonathan

Good morning, I read with interest the balance transfer credit cards with no interest for a period of time. I, like many people have that problem of having not paid my CC on the due date and now have a big balance. I currently have an ANZ Platinum CC, can I apply for a balance transfer with no interest?

Thank you

Hi Sharon,

Thanks for your inquiry.

Balance transfers can be a great way to repay an outstanding credit balance interest-free. You may like to compare balance transfer offers and cards.Select ‘Go to Site’ to head over to their website to apply. Please ensure to read through the relevant product disclosure statement and terms and conditions to ensure that you got everything covered before you apply to the card.

Cheers,

Jonathan

Hi, I’m looking for a credit card to allow me to pay bills between payments from work. Would use it very little only when my funds are a bit tight. Any recommendations? Suggestions

Hi Billy,

Thanks for your question.

If you are only planning on using your credit card sporadically, you may wish to consider low interest rate credit cards or no annual fee or a low income credit card.

Credit cards with high annual fees and rates usually come with extra features such as concierge services, complimentary insurance, and rewards programs. If you are after a credit card to use as a backup for your finances, some of these no frills options may be of interest.

You can select the “Go to Site” button of your preferred credit card to proceed with your application. You can also contact the provider if you have specific questions. A gentle reminder, please ensure to read through the relevant product disclosure statement and terms and conditions to ensure that you got everything covered before you apply.

I hope this has helped.

Thanks,

Sally