Market Value vs Agreed Value car insurance

Agreed value car insurance means you can choose the value of your car, and market value is usually a cheaper premium. Which one is better?

When you take out a car insurance policy, you get to choose between insuring your car for market value or agreed value. Market value means the figure of what your car is worth is decided on the day that you make a claim, based on what your insurer estimates your car is worth — this could be in line with what you think it's worth, or you might get a nasty surprise. For those who love known outcomes, you can choose agreed value, where you and your insurer agree on a a specific amount. Sounds great, right, so what's the catch? Your premiums are likely to cost more for an agreed value policy.

We currently don't have that product, but here are others to consider:

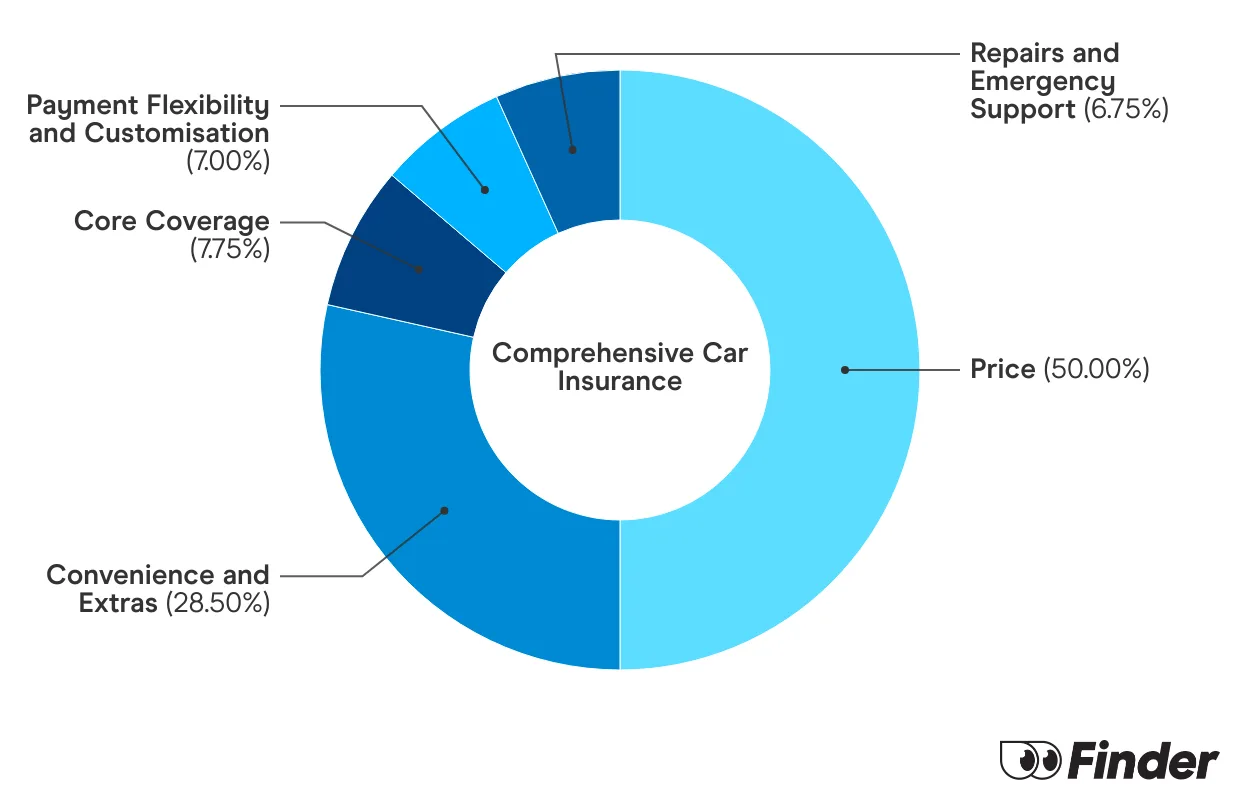

How we picked theseWe analyse over 30 car insurance products across insurance providers, and rate each one for price and features. We collect up to 36 quotes per product, for male and female drivers in New South Wales, Victoria, Queensland, South Australia, Tasmania and Western Australia. Quotes are collected for 20 year olds, 30 year olds and 60 year olds, assuming an excess of $850 for a 2020 Toyota Corolla 4 door sedan model, with an average 15,000 kms driven each year. While we are not allowed to display actual quotes, our Finder Score aims to serve as an indicative guide to how cost and feature competitive a product might be for you.

Our feature score assesses each product for more than 15 features across loss and damage coverage, repairs and assistance coverage, personal items coverage and policy coverage. Features we assess include but are not limited to legal liability, essential repairs, new car replacement, car hire events, roadside assistance, agreed or market value, windscreen damage and natural disaster coverage.

Agreed value policies tend to cost more for 2 reasons:

Pros:

Cons:

"When picking between agreed or market value, it's good to know how the second hand car market is for your car model. For example, when the production of cars was low during lockdowns, second hand cars were selling well above the normal price because new cars were so hard to come by. This made the market value of cars pretty high, which meant that selecting this cover could actually be more expensive than agreed value. However, this can change with the market. If you want to know for sure what your car is insured for, agreed value is the way to go. Personally, the market value of my car would cover what's remaining on my loan so I've gone with market value cover. "

Pros:

Cons:

The right policy for you depends on your situation and you should always consider the benefits and drawbacks of each policy in line with your own needs.

In a general sense: agreed value can be a great idea if you want to know the exact level of cover you have, and it gives you peace of mind knowing what that payout figure is if you have to make a claim. Market value can be a great idea if you want to keep your premiums affordable and the payout would cover your loan in the event of a claim.

If you’re having trouble deciding, try considering the following situations:

Compare policies from Australian brands

ALDI car insurance offers comprehensive car insurance with really solid benefit limits.

Drivers who text are 10 times more likely to crash yet a large number of Australians still do it.

Although Kogan’s cover is strong, its premiums were the second most expensive out of 30 car insurance brands we compared.

ahm offers a decent level of coverage but might not suit drivers on a tighter budget.

With 5% off for seniors, budget-friendly policies, and some uncommon benefits, Australian Seniors is worth considering.

ANZ car insurance is typically more expensive than average, but it does have some generous benefits.

Australian Unity car insurance, underwritten by Allianz, offers two levels of cover, the freedom to choose your own repairer and an easy 24-hour claims service.

APIA car insurance is issued by AAI Limited and offers 3 levels of cover, a range of discounts and a lifetime guarantee on repairs.

With a higher-than-average price but no particularly impressive benefits, Allianz was outperformed by many other car insurers in the 2024 Finder Insurance Awards.

With strong cover and reasonably-priced policies, AAMI performed well in the 2024 Finder Awards. However, some popular benefits are missing and cheaper options are available.

Can an insurer write-off and cancel the licence on a vehicle without advising the owner?

After hitting a kangaroo, we checked car, all well safety wise, bar both headlight glass broken lights still good. bonnet bent but still locks , tracks straight , stops straight.so drove over 300 kms home. The repair cost was within a few hundred dollars of their write-off amount. We were still contesting their payout amount & driving the car, as vast distances are involved.

On the 1/03/2018 in the mail, we were informed by Department of transport that on 21 /02/2018 the licence had been cancelled, and unbeknown to us, we had been driving a unregistered vehicle.

We did agree to have the car repaired at no extra cost to the insurer on the 1/03 /2018 after a phone conversation with the insurer, Cash Settlement to be made, vehicle to be left REGISTERED. We keep salvage of said vehicle.

Is there anything we can do to have the insurer have the car registered so we can have it repaired? We are 900 kms from a major city , to licence a written-off vehicle we will need to have the car carried to an inspection point that is accredited by dept. of transport to pass inspection , as there is no accredited repairers for written off vehicles anywhere near us.

Hi John,

Thanks for reaching out to Finder.

I’m sorry to hear that you were taken by surprise that your vehicle was registered as a repairable write-off and that the registration was cancelled. The Motor Vehicles Regulations 2010 didn’t specifically state whether the insurer needs to notify the owner before it gives notice to the Registrar in relation to the vehicle’s assessment. They are, however, mandated to notify the Register within 7 days from when the determination is made by them to write off the vehicle. Time constraint could be a factor why you weren’t informed beforehand. You can ascertain the exact reason from your insurer directly. You can also call VicRoads on 13 11 71 to discuss your concern about the vehicle written-off process.

As to re-registering your car, you need to have it repaired and assessed as roadworthy during the VIV inspection first before you can register it again. You can reach out to VicRoads Vehicle Fitness Section on 1300 360 745 to discuss the technical requirement of the VIV inspection. You might also find VicRoads’ written-off vehicles FAQs informative.

Now, regarding the repair costs and settlement, it’s a good idea to have those in writing just in case you will need them along the process. Moreover, you can also seek professional advice on the matter.

I hope this information helps.

Cheers,

Liezl