A credit card's interest-free days let you spend money now and then pay it off a bit later without paying any interest.

The interest-free period starts on day 1 of your card's 30-day statement period. Making a purchase earlier in the statement period gives you more interest-free days.

Credit cards offer between 44 and 55 days interest-free, but it depends on the card.

What are interest-free days on a credit card?

Credit cards have statement periods that usually run for 30 days. Day 1 of a statement period is also day 1 of the card's interest-free period.

Let's say your credit card gives you 55 days interest free. This means you have 55 days from day 1 of the statement period before you get charged any interest on your card purchases.

Any purchases made on day 2 give you 54 days interest free. By day 3 you have 53 interest-free days left. If you make a purchase on day 30, the last day of the statement period, you have 25 days before interest is charged.

Once you hit the 55-day mark you can pay off all your spending and pay no interest. Or you'll get charged interest on any unpaid balance on the card.

Example: How to use the interest-free period on a credit card

Say you had a credit card that offers 55 interest-free days, with a statement period that starts on the 1st of each month and ends on the 30th. If you were making purchases in June, here's how it works:

1 June. First day of the statement.

30 June. Last day of the statement.

25 July. The 55 day interest-free period ends. This is also the payment due date for this statement period.

Now here's how your card spending breaks down over this statement period.

You make a $200 purchase on 1 June. You don’t have to pay any interest towards this purchase until 25th July, which gives you 55 interest-free days.

You make a $100 purchase on 20 June. This is the 20th day of your statement period, which means you get 35 days interest-free before a payment is due on 25th July.

You make a $150 purchase on 30 June. This is the last day of your statement period but the purchase won't attract any interest until 25th July, giving you an interest-free period of 25 days.

In this example, you would have a credit card balance of $450 from new purchases on your June statement. If you paid the total amount owed by the 25th July, you wouldn't be charged interest on your purchases.

You'd also get interest-free days for the next statement period.

Will I get a new 55-day interest-free period if I don't pay off my previous month's balance in full?

Usually, when you carry a balance over to your next statement period you won't be eligible for interest-free days for that statement period. To get the interest-free period back, you'll need to pay the total amount listed on your next 1-2 statements by the due date.

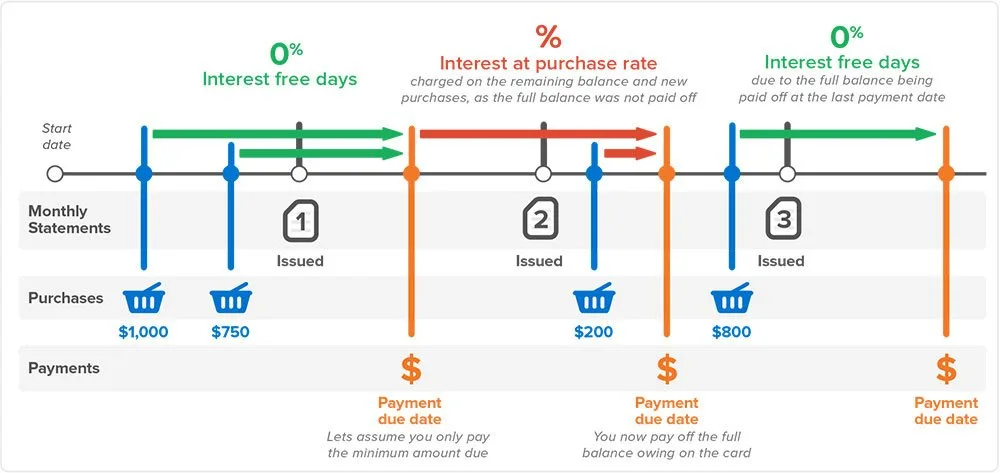

How do interest-free days work?

This visual example of interest-free days highlights the interest-free period (in green), when purchases are made, when the statement is issued and what happens if you pay less than the full amount for a billing cycle.

Key terms for interest-free days

Statement period or billing cycle. The statement period shows activity on your credit card account and usually runs for 30 days, or from when your last statement was issued to when the next one is issued.

Payment due date. This date is listed on your statement and tells you when you need to pay at least the minimum amount. If you want to get interest-free days, you'll usually have to pay the total balance by the due date.

Closing balance or payment closing balance. The total you need to pay by the due date on your statement if you want to get interest-free days for the next statement period. A "closing balance" is usually the total of what's owed on your account.

Minimum monthly payments. This is the minimum you need to pay by the due date on your statement to avoid late fees and a late payment listing on your credit report. You usually can't get interest-free days for purchases if you only pay this amount.

Purchase rate. The interest rate charged on purchases. Interest-free days help you avoid this interest charge.

Is a credit card with interest-free days worth it?

Most credit cards in Australia offer interest-free days on purchases. It might not be the most important feature to you, but it does give you more flexibility in how you spend.

Let's say you have a $2,000 purchase coming up. Paying cash would take a big chunk out of your savings but payday is still 2 weeks away.

In this case, interest-free days would be really helpful. You could make the $2,000 purchase today and wait a few weeks before you have to pay the purchase off.

How to make interest-free days work for you

Understand how the interest-free days and your statement period work. The interest-free period starts when your statement period starts. You don't get 55 days from the start of every single purchase. If you make a big purchase on day 30 of the statement period you have far fewer interest-free days.

Time big purchases carefully. If you have big purchases coming up and want to maximise your interest-free days, make the purchase at the start of your statement period. This gives you more time before you have to pay it off.

Choose your credit card carefully. Interest-free days are a great card feature. But don't forget to look at the card's annual fee, purchase rate and any perks or benefits, like rewards or frequent flyer points.

Finder survey: How long have Australians had their current interest-free credit card?

Response

5+ yrs

37.5%

2 yrs

27.94%

1 year

13.24%

3 yrs

13.24%

Less than 1 year

4.41%

4 yrs

3.68%

Source: Finder survey by Pure Profile of 1113 Australians, December 2023

Frequently asked questions

The humm90 Mastercard offers up to 110 days interest-free on all purchases (excludes cash advances). This is the highest number of interest-free days currently available on a credit card in Australia according to the Finder database. In comparison, most other credit cards offer between 44 and 55 days interest-free. These are also other cards that offer extended interest-free finance options with specific retail partners.

Additional cards linked to your primary card follow the same billing cycle as the primary card and offer just as many interest-free days on purchases.

You usually need to repay the full closing balance that's listed on your statement by the due date to get interest-free days. In most cases, you also need to pay the full balance for the previous statement, as well as the statement issued at the end of that period.

If you set up an instalment plan for part of your balance, you will usually have to pay the required instalment repayment, as well as the rest of your monthly account balance, to remain eligible for interest-free days. These details are shown on your credit card statement. If you're unsure, contact your provider to check whether you can still get interest-free days when you have an instalment plan.

Some credit cards let you make interest-free purchases when you have a balance transfer, as long as you pay the entire purchase balance for your statement. These details will typically be shown on your statement. For example, NAB has an "interest-free days payment" amount that you can pay to still get interest-free days while you carry a balance transfer debt. And Westpac has a "Monthly Payment Balance" that shows the amount you need to pay to get interest-free days on purchases. But other cards only offer interest-free days for purchases when you pay the account's entire closing balance, including any balance transfer debt. So it's important to check these details and plan your repayments to make sure it's manageable.

Buy now pay later services let you make a purchase and pay it off in installments. Like with a credit card, if you make the payments on time there should be few if any extra costs (some BNPL companies charge a monthly account fee). But if you miss the payments then you pay late fees. Like interest, these fees can really start to add up.

Richard Whitten is Finder’s Senior Money Editor, with over eight years of experience in home loans, property, credit cards and personal finance. His insights appear in top media outlets like Yahoo Finance, Money Magazine, and the Herald Sun, and he frequently offers expert commentary on television and radio, helping Australians navigate mortgages and property ownership. Richard started his career in education and textbook publishing in South Korea. He holds multiple industry certifications, including a Certificate IV in Mortgage Broking (RG 206) and Tier 1 and Tier 2 certifications (RG 146), as well as a Bachelor of Education from the University of Sydney and a Graduate Certificate in Communications from Deakin University.

See full bio

Richard's expertise

Richard

has written

698

Finder guides across topics including:

Amy is an experienced journalist with over 16 years of experience, contributing to major publications like Money Magazine, The Sydney Morning Herald, and ABC News Australia. Specialising in personal finance, she frequently appeared in media outlets and on radio. Amy holds a Bachelor of Arts in Journalism and Drama from Griffith University and earned RG146 certifications in Tier 1 Generic Knowledge and Tier 2 General Advice Deposit Products, ensuring her expertise is grounded in current financial regulations. Amy was Finder's Senior Writer for Credit Cards from 2016 to 2024.

See full bio

Amy's expertise

Amy

has written

494

Finder guides across topics including:

Do any of the 55 days interest free credit cards require a monthly minimum spend?

There’s information about cash advances and making payments but I’d like to know if any credit cards require a minimum amount is spent each billing period (particularly if you plan to pay the balance by the due date?).

Finder

AmyMarch 20, 2023Finder

Hi Jenny,

Credit cards don’t require you to spend a minimum amount each month. So you could spend between $0 up to your available credit limit in a billing cycle. Just keep in mind there is a minimum repayment amount, which will be shown on each statement. I hope that helps.

NicoleJanuary 25, 2016

Is paying telstra, synergy, Alinta gas , western power also a cash advance or can I use my credit card

Finder

DebbieJanuary 27, 2016Finder

Hi Nicole,

Thanks for your inquiry.

If these falls under bill payments then typically they may be considered as cash advances. I suggest that you speak to your credit card provider directly to confirm whether the payments for the mentioned services or utility providers are considered as cash advances. You can also revisit your cardholder agreement with your credit card provider to learn more about their terms.

To know more which credit card transactions fall on cash advances, kindly refer to our guide on cash advances.

I hope this helps.

Cheers,

Debbie

HayleyNovember 18, 2015

Hi,

If my statement closes on say the 30th October and I owe $100 on my credit card which is due 15th November, if I pay the $100 off on the 10th November and then proceed to spend another $50 on my credit card that same day, is my balance considered cleared on the 15th November and that $50 goes to next months billing cycle or will I be charged interest on that new $50 now?

Finder

JonathanNovember 20, 2015Finder

Hi Hayley, thanks for your inquiry!

To allow us to assist you further could you provide us with a specific bank please?

Cheers,

Jonathan

HayleyNovember 20, 2015

Hi Jonathan,

ANZ – Platinum rewards

Finder

JonathanNovember 22, 2015Finder

Hi Hayley, thanks for your response.

Even if you had cleared your $100 outstanding balance, your entire balance (including the $50) would have to be cleared before your payment due date in order to receive interest-free days on your purchases.

I hope this helps.

Cheers,

Jonathan

BenApril 7, 2015

Hi

Iv just got a mortgage and want to utilize a credit card with my monthly day to day spending so I can pay my weekly income straight off the mortgage. I then want to redraw from my mortgage to pay off my credit card each month.

Can I get a card which will allow me to make both purchases and cash withdrawals which will be interest free over a 1 month period?

Finder

JonathanApril 8, 2015Finder

Hi Ben,

Thanks for your inquiry.

Please refer to the following link for a list of 0% purchase cards. As of this time, there are no interest-free rates on cash advances, although there are low rate cash advance cards available.

You can press the “Go to Site” button of your preferred credit card to proceed with your application. You can also contact the provider if you have specific questions. A gentle reminder, please ensure to read through the relevant product disclosure statement and terms and conditions to ensure that you got everything covered before you apply.

Cheers,

Jonathan

MariaSeptember 30, 2014

My question is:

If I paid in full one period, it supposes I am not going to be charged with interest for that period (which is reflected in my next statement). My bank charged me interest anyway the next period. I asked the bank and they replied that only if I pay in full every period I am not getting charged with interest.

Is that correct?

Thanks…

Maria

Finder

ElizabethOctober 1, 2014Finder

Hi Maria,

Thanks for your question.

This is correct. Only by paying your balance in full each month are you able to avoid interest on purchases each statement period.

A credit card cash advance is when you withdraw money or get a “cash equivalent” like gift cards – and it typically attracts high rates and fees.

Important information about this website

Finder makes money from featured partners, but editorial opinions are our own.

Finder is one of Australia's leading comparison websites. We are committed to our readers and stand by our editorial principles.

We try to take an open and transparent approach and provide a broad-based comparison service. However, you should be aware that while we are an independently owned service, our comparison service does not include all providers or all products available in the market.

Some product issuers may provide products or offer services through multiple brands, associated companies or different labeling arrangements. This can make it difficult for consumers to compare alternatives or identify the companies behind the products. However, we aim to provide information to enable consumers to understand these issues.

We make money by featuring products on our site. Compensation received from the providers featured on our site can influence which products we write about as well as where and how products appear on our page, but the order or placement of these products does not influence our assessment or opinions of them, nor is it an endorsement or recommendation for them.

Products marked as 'Top Pick', 'Promoted' or 'Advertisement' are prominently displayed either as a result of a commercial advertising arrangement or to highlight a particular product, provider or feature. Finder may receive remuneration from the Provider if you click on the related link, purchase or enquire about the product. Finder's decision to show a 'promoted' product is neither a recommendation that the product is appropriate for you nor an indication that the product is the best in its category. We encourage you to use the tools and information we provide to compare your options.

Where our site links to particular products or displays 'Go to site' buttons, we may receive a commission, referral fee or payment when you click on those buttons or apply for a product.

When products are grouped in a table or list, the order in which they are initially sorted may be influenced by a range of factors including price, fees and discounts; commercial partnerships; product features; and brand popularity. We provide tools so you can sort and filter these lists to highlight features that matter to you.

Please read our website terms of use and privacy policy for more information about our services and our approach to privacy.

We update our data regularly, but information can change between updates. Confirm details with the provider you're interested in before making a decision.

How likely would you be to recommend Finder to a friend or colleague?

0

1

2

3

4

5

6

7

8

9

10

Very UnlikelyExtremely Likely

Required

Thank you for your feedback.

Our goal is to create the best possible product, and your thoughts, ideas and suggestions play a major role in helping us identify opportunities to improve.

The information provided by Frankie is general in nature and has been prepared without considering your objectives, financial situation or needs. Frankie may make mistakes so it's important that you review the information before deciding. By messaging Frankie, you agree to our Terms and have read our Privacy Policy.

Do any of the 55 days interest free credit cards require a monthly minimum spend?

There’s information about cash advances and making payments but I’d like to know if any credit cards require a minimum amount is spent each billing period (particularly if you plan to pay the balance by the due date?).

Hi Jenny,

Credit cards don’t require you to spend a minimum amount each month. So you could spend between $0 up to your available credit limit in a billing cycle. Just keep in mind there is a minimum repayment amount, which will be shown on each statement. I hope that helps.

Is paying telstra, synergy, Alinta gas , western power also a cash advance or can I use my credit card

Hi Nicole,

Thanks for your inquiry.

If these falls under bill payments then typically they may be considered as cash advances. I suggest that you speak to your credit card provider directly to confirm whether the payments for the mentioned services or utility providers are considered as cash advances. You can also revisit your cardholder agreement with your credit card provider to learn more about their terms.

To know more which credit card transactions fall on cash advances, kindly refer to our guide on cash advances.

I hope this helps.

Cheers,

Debbie

Hi,

If my statement closes on say the 30th October and I owe $100 on my credit card which is due 15th November, if I pay the $100 off on the 10th November and then proceed to spend another $50 on my credit card that same day, is my balance considered cleared on the 15th November and that $50 goes to next months billing cycle or will I be charged interest on that new $50 now?

Hi Hayley, thanks for your inquiry!

To allow us to assist you further could you provide us with a specific bank please?

Cheers,

Jonathan

Hi Jonathan,

ANZ – Platinum rewards

Hi Hayley, thanks for your response.

Even if you had cleared your $100 outstanding balance, your entire balance (including the $50) would have to be cleared before your payment due date in order to receive interest-free days on your purchases.

I hope this helps.

Cheers,

Jonathan

Hi

Iv just got a mortgage and want to utilize a credit card with my monthly day to day spending so I can pay my weekly income straight off the mortgage. I then want to redraw from my mortgage to pay off my credit card each month.

Can I get a card which will allow me to make both purchases and cash withdrawals which will be interest free over a 1 month period?

Hi Ben,

Thanks for your inquiry.

Please refer to the following link for a list of 0% purchase cards. As of this time, there are no interest-free rates on cash advances, although there are low rate cash advance cards available.

You can press the “Go to Site” button of your preferred credit card to proceed with your application. You can also contact the provider if you have specific questions. A gentle reminder, please ensure to read through the relevant product disclosure statement and terms and conditions to ensure that you got everything covered before you apply.

Cheers,

Jonathan

My question is:

If I paid in full one period, it supposes I am not going to be charged with interest for that period (which is reflected in my next statement). My bank charged me interest anyway the next period. I asked the bank and they replied that only if I pay in full every period I am not getting charged with interest.

Is that correct?

Thanks…

Maria

Hi Maria,

Thanks for your question.

This is correct. Only by paying your balance in full each month are you able to avoid interest on purchases each statement period.

Hope this has helped.

Thanks,

Elizabeth