Aim for significant bonus points typically over 100,000 by meeting initial spend requirements to maximise card value.

High annual fees and purchase rates mean rewards must outweigh costs; pay balances promptly to avoid interest.

Match your card to desired rewards like frequent flyer programs or gift cards based on your spending habits.

The best rewards credit card offers in June 2026

The best rewards credit card on the market in June, based on its Finder Score, is the American Express Platinum Card. It has a score of 9.9 and offers new AMEX customers up to 200,000 bonus points. Unlike many cards with big bonus points offers, you don't have to wait over 12 months to get all the points either. It does have an annual fee that's over $1,000 though. The ANZ's Rewards Black Credit Card also has a strong points offer (180,000 ANZ Rewards Points), with a much lower annual fee. But you have to hold the card for over 15 months to get all those points.

Updated June 2026 by Finder's senior money editor, Richard Whitten.

What is a rewards credit card?

Rewards credit cards let you earn points for every dollar you spend. Some cards also offer hundreds of thousands of bonus points if you spend a certain amount after opening the card.

You can get rewards points with a reward program like CommBank Awards, ANZ Rewards or AMEX Membership Rewards. And there are supermarket rewards points like Flybuys and Everyday Rewards that function in a similar way (and you can earn Flybuys with a Coles credit card).

How can I use these points?

You can redeem rewards points in different ways:

Cashbacks and gift cards

Hotels, flights and accommodation

Retail goods like cosmetics, electronics and homewares

Frequent flyer points (usually at a rate of 2:1 or 3:1).

Some cards offer cashback instead of points. Some cards offer both.

You can redeem the points via your bank or reward program's store (for example, the NAB Rewards Store).

Do you need a rewards credit card?

Rewards credit cards are suited to bigger spenders, frequent flyers and people who shop a lot. You get rewarded because you're spending money. These cards are not budget or entry level credit cards because the rates and annual fees are higher.

Pros

Points for spending. The most obvious perk of these cards is that you earn rewards of your choice, for money you were going to spend anyway. Why not get a reward for spending?

Bonus points offers. New cards usually offer a bunch of bonus points when you spend a certain amount in the first few months. These points offers should have a dollar value that's greater than the cost of the card's annual fee.

Perks. Rewards credit cards often come with extra perks like complementary travel insurance, purchase insurance, concierge services and lifestyle and entertainment offers.

Cons

Higher rates. To pay for the points and perks, these cards typically charge higher ongoing interest rates than other cards. But if you pay off your balance in full each month there's no interest.

Annual fee. Rewards cards come with an annual fee that can cost several hundred dollars.

Temptation to overspend. The promise of rewards points can lead you to spend more than you usually would.

Rewards limitations. Some rewards cards cap how many points you can earn.

Many rewards credit cards in Australia earn points that you can redeem for different types of rewards, including gift cards, retail items, credit on your account, travel or point transfers to other loyalty programs. These flexible rewards programs include:

A Finder survey of 1,017 Australian consumers found that Australian shoppers really love Woolworths Everyday Rewards and Coles Flybuys Points. 66% of us collect Everyday Rewards and 63% are in the Flybuys program. This is followed by Qantas Points (35%) and Velocity Points (29%). The actual credit card rewards programs offered by AMEX and major banks are much less popular. 12% collect CommBank Awards points followed by ANZ (8%), Westpac Rewards (6%) and Amex Membership Rewards (5%).

Source:Finder Consumer Sentiment Tracker

Frequent flyer rewards

If you're a member of a frequent flyer program, you can use a credit card to earn more Qantas or Velocity Points or miles in 2 ways:

1. Frequent flyer points per $1 spent

Credit cards that directly partner with a frequent flyer program let you earn frequent flyer points on your spending.

2. Reward point transfers to frequent flyer programs

Some rewards credit cards let you transfer points to different frequent flyer programs. This gives you more flexibility because you're not locked into one program.

It's also a way to earn points with programs that don't have co-branded cards in Australia, including Singapore Airlines KrisFlyer, Cathay Pacific Asia Miles and Emirates Skywards.

But rewards points usually convert to frequent flyer points at a rate of 2:1 or even 3:1. So 100,000 rewards points might only get you 50,000 Qantas Points.

Cashback credit cards

These credit cards give you a way to get cash rewards for your spending, either in the form of credit back on your account or vouchers you can spend.

Some cashback credit cards give you a set percentage of your regular spending as cashback on your account (capped to a max amount), while other cards have introductory offers that provide a one-time account credit or voucher when you meet the spend requirements.

Our expert says: Choose rewards that work for you

"Before you even compare credit cards, why not look at the rewards programs out there? Work out what you actually want. If you specifically want Qantas Points you might be better off with a card that earns Qantas Points directly. But if you're interested in gift cards and retail items, look at the rewards stores for different reward programs and see what's on offer."

Here's what you need to look at when comparing rewards credit cards:

How can I earn points? How many points will you earn per dollar spent? A bonus points offer can give you a huge amount of value when you get a new card. Some cards have caps on how many points you can earn.

What's the value of the rewards? What is 1,000 points actually worth? Every rewards program is different. If you need 12,000 points to get a $50 gift card and your credit card has an earn rate of 1 point per $1 spent. You would need to spend $12,000 before you could redeem the $50 gift card.

What will the card cost me? The annual fee is the biggest reward card cost. Some rewards credit cards offer no annual fee for the first year or ongoing. The value of the rewards you redeem should be higher than the cost of the annual fee to make it worthwhile. Don't forget the card's interest rate either. You can avoid interest charges by paying your balance in full each statement period.

What are eligible purchases on a rewards card? Most everyday spending is eligible to earn points, including groceries, petrol, retail items and travel. Transactions that don't usually earn points include cash advances, BPAY payments and spending with government bodies.

How much do you need to spend to get rewards?

To give you an idea of the potential value of rewards, we've compared the amount of points you need to redeem a $100 gift card through major rewards programs that are linked to credit cards.

Fees, points and redemption values correct as of January 2026.

Based on this table, the minimum spend required for a $100 gift card (or equivalent) is $10,000 with American Express Membership Rewards or Flybuys if your credit card offers 2 points per $1 spent.

How we calculate Rewards Credit Card Finder Scores

These cards offer the best ongoing earn rates and sign up offers, coupled with attractive annual fees and perks.

7+

Great

Reasonable rewards cards but may offer slightly lower ongoing or signup offers.

5+

Standard

These cards may offer lower ongoing and sign up points, but could also offer fewer perks or higher annual fees.

0+

Basic

Entry level rewards cards, that offer consumers basic sign up offers and ongoing earn rates.

How the Rewards Card Finder Score works

9+ Excellent - These cards offer the best ongoing earn rates and sign up offers, coupled with attractive annual fees and perks.

7+ Great - Reasonable rewards cards but may offer slightly lower ongoing or signup offers.

5+ Satisfactory - These cards may offer lower ongoing and sign up points, and fewer perks, but probably have lower annual fees.

Less than 5 – Basic - Entry level rewards cards, that offer consumers basic sign up offers and ongoing earn rates.

We analyse 100+ rewards credit cards and look at 6 key features to create our Finder Scores.

For the rewards card category, points from rewards programs are converted to a dollar value, by determining the number of points required to purchase a grocery store gift card, or a direct dollar value conversion, within the rewards program store.

To qualify for the rewards score, credit cards must:

Offer signup or ongoing rewards points affiliated to a rewards program.

Be available to general consumers.

Our aim is to help your with financial decision-making, but please consider your own financial circumstances. While we may make money from commercial partnerships, they have no weight in our methodology. The database is scored objectively and reviewed by our editorial team.

Feature

Definition

Assessment

Weight

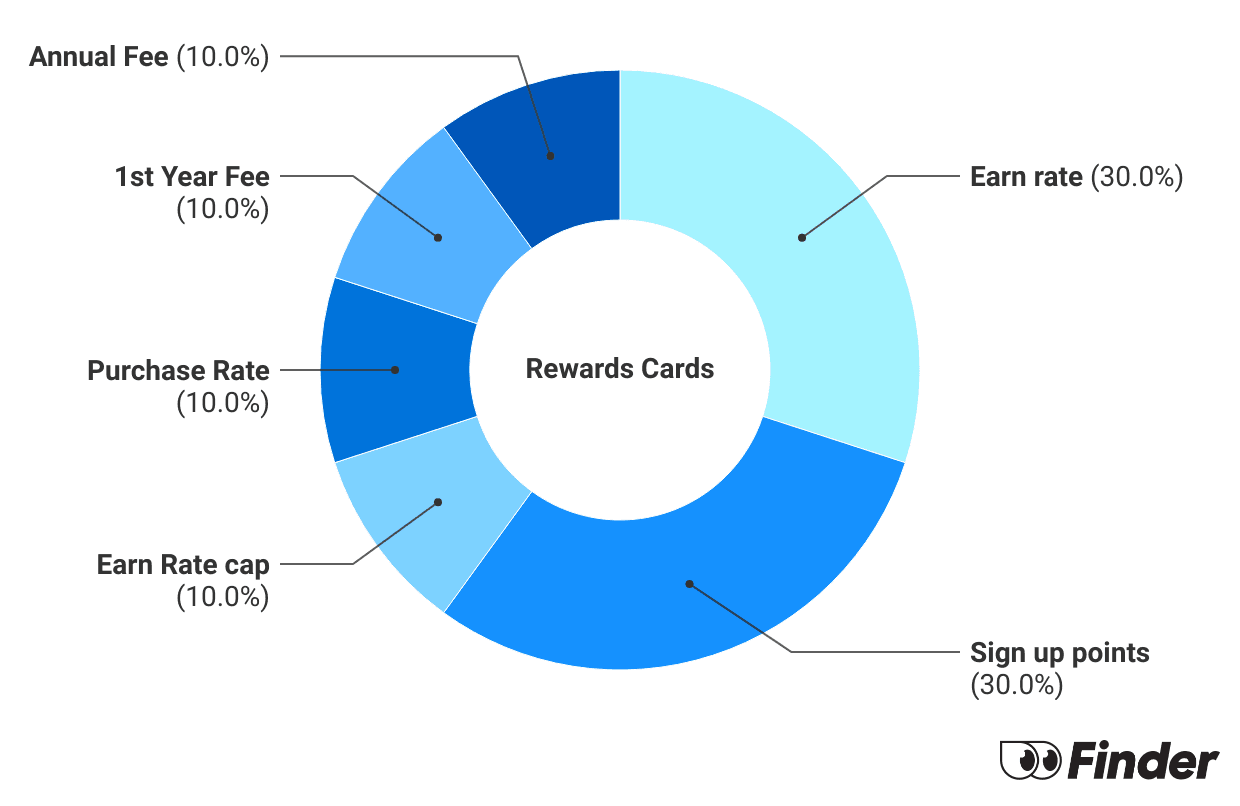

Earn Rate

Points earned for every dollar spent on eligible purchases

Points awarded per dollar. Points are converted to a dollar value

30%

Sign-Up Points

Bonus points earned for signing up and meeting spending requirements

Total bonus points offered. Points are converted to a dollar value

30%

Purchase Rate

Interest rate on new purchases

Lower rates receive higher scores (up to 23.99% max)

10%

Earn Rate cap

Maximum points earned in a billing cycle before a lower earn rate applies

Finder's database shows that the American Express Platinum Business has the biggest bonus points offer, with up to 350,000 Membership Rewards Bonus Points when you spend $12,000 in the first 3 months. That's enough for $1,350 worth of travel with Webjet based on details listed on the American Express website.

It's unlikely but does depend on the rewards program and credit card provider. For example CommBank, Westpac, St.George and Virgin Money all list BPAY payments as ineligible to earn rewards.

While other credit card issuers (such as ANZ) doesn't specifically list BPAY transactions as ineligible for points, that doesn't mean you will earn points. Or that you'll be able to use a credit card for a BPAY payment. Check the terms and conditions or ask your provider for details specific to your card.

Each year the Finder Credit Card Awards recognises Australia's top credit cards, with expert analysis of rates, fees and offers based on 12 months' worth of data.

In 2026 the ANZ Rewards Black Credit Card once again took out the top spot in the rewards credit card category with its very compelling offer. The card's high earn rate and hefty bonus points sign-up offer and other benefits made it a strong winner this year.

Every rewards program is different, but here's a general guide to the process of redeeming points:

Log into your account

Browse the rewards and choose one you want

Check that you have enough points or can use points plus pay

Confirm the details and follow the prompts to complete your redemption

Anyone aged over 18 can apply for a credit card when they meet the bank or lender's eligibility criteria. This typically includes:

Minimum income requirement. This can range from $35,000 per year for a basic rewards card to over $100,000 for a premium card. Even when there is no specific minimum income amount listed, your income will need to be enough to manage at least the minimum credit limit, account fees and interest charges.

New cardholder status. Many introductory offers require you to be a new cardholder that hasn't held a similar card (or one from the same brand) in the past 12-18 months.

Residency status. Some lenders require you to be a citizen or permanent resident, while others allow visa holders and temporary residents to apply as well.

Credit history. All credit cards require you to have a good credit history and not be an undischarged bankrupt or have any judgements against you.

If you're eligible to apply, you'll also be required to provide documents including payslips and proof of identification. The provider will then assess the details you provide to determine whether you'll be approved based on their criteria and responsible lending requirements.

With most credit card bonus points offers, you need to spend a certain amount in the first few months or over another period of time. It's important to only spend what you can afford to pay off so you don't end up with interest charges that take value away from the points.

Here are examples of different ways to meet the minimum spend requirements.

Booking travel

Buying major household items (e.g. a lounge or fridge)

Buying a new laptop, tablet, phone or other tech

Pre-paying your health insurance or other bills

Paying for car services or repairs

Seasonal shopping (e.g. school holidays, Christmas)

Paying for everyday expenses (e.g. groceries, fuel, subscriptions)

Bonus points are typically added to your account within 1-12 weeks of when you meet the spend requirement. But it depends on the offer. You can check the fine print or call the credit card company to find out when points will be added to your account.

It's worthwhile if you get more value from rewards than what you're paying for the account. This makes rewards cards more suited to people who already use a credit card regularly and/or can repay what they spend each month.

When comparing your options, ask the following questions:

How much is the annual fee? Reward and frequent flyer credit card annual fees can quickly outweigh the value of rewards, even if you're getting thousands of bonus points.

What are the potential interest costs? Estimate how much you could end up paying if you carry a balance on the card to decide if the risk is worth it for you. For example, if a credit card had a 19.99% p.a. purchase rate, a minimum spend requirement of $3,000 in 3 months to get bonus points and it took you 6 months to pay that amount off, you'd be charged around $177 in interest.

How much are the points worth? Look at the value of the points based on what rewards you want to redeem. For example, if 100,000 bonus points was worth $500 in digital gift cards, that could help justify a card's annual fee. It's worth looking at a few reward options for any card offering bonus points. You can also calculate the dollar value of your points.

When do you want to use your points? The time it takes for you to earn enough points for your ideal reward could be a few weeks. But it could be a lot longer if you're saving up points per $1 spent or waiting for a particular reward to become available (especially flight rewards). So it can be helpful to have a timeframe in mind, then work out how many points you'd realistically earn through the card.

Depending on the card and rewards program, the points could be transferred to another person, converted into a statement credit or cancelled.

You can find details for your rewards program by looking at the terms and conditions, or by asking the provider. They should also let you know what options are available when they're notified of someone's death.

Richard Whitten is Finder’s Senior Money Editor, with over eight years of experience in home loans, property, credit cards and personal finance. His insights appear in top media outlets like Yahoo Finance, Money Magazine, and the Herald Sun, and he frequently offers expert commentary on television and radio, helping Australians navigate mortgages and property ownership. Richard started his career in education and textbook publishing in South Korea. He holds multiple industry certifications, including a Certificate IV in Mortgage Broking (RG 206) and Tier 1 and Tier 2 certifications (RG 146), as well as a Bachelor of Education from the University of Sydney and a Graduate Certificate in Communications from Deakin University.

See full bio

Richard's expertise

Richard

has written

772

Finder guides across topics including:

How do i add my Woolworths Rewards card to my iphone wallet?

Finder

RichardOctober 1, 2025Finder

Hi Susie,

It looks like you can use this link on the Woolworths website and enter your card and mobile numbers.

SandyAugust 29, 2024

I would like a card with points accumulated when i use to shop at groceries and points to put towards my trips when i fly?

Finder

AngusSeptember 16, 2024Finder

Hi Sandy, If your goal is to earn points with grocery shopping, then a good approach is to get a credit card that earns airline points and is also partnered with a major supermarket – that way, you can earn points from paying with the card, and also convert your supermarket loyalty points into additional airline points. Qantas is partnered with Woolworths/Everyday Rewards, while Virgin/Velocity is partnered with Coles/Flybuys, so exploring cards that earn with either of those airlines could help you earn more points. Have fun exploring!

RonJanuary 7, 2018

Can I use diners club rewards with Emirates?

Finder

RenchJanuary 7, 2018Finder

Hi Ron,

Thanks for your inquiry.

Yes, the Diners Club Rewards program also allows you to transfer your reward points to 17 airline and travel loyalty programs, including Virgin Australia’s Velocity frequent flyer program, Emirates Skywards, Etihad Guest, and Hilton Honors.

I spend and pay off in full about 25K per month of normal spending on my Citi Signature card which since the 1st July 2017 have at best halved their reward points which I use for Qantas flights.

What is the best card now for me to get the most points for my spend per month, ie who is dollar for dollar and uncapped

Finder

HaroldJuly 28, 2017Finder

Hi Kym,

Thank you for your inquiry.

While we cannot recommend what is best for you, we can offer you general information. You can check the list of frequent flyer credit cards featured on our website to learn more.

I hope this information has helped.

Cheers,

Harold

MazJune 28, 2017

Since the rules for the credit card reward points that you earn are changing as of the 1st July 2017, what would be the best rewards card that you can earn points for make payments to the ATO? Currently have a Westpac Altitude Rewards card and this is changing from 1st of July 2017 where you no longer receive points for ATO payments.

Well-known among frequent flyers and point chasers, this controversial strategy involves taking advantage of bonus point offers on different credit cards.

Credit card rewards and other loyalty programs have the potential to offer you extra value for your spending – here’s how to work out if you are getting it.

Use your credit card to earn up to 2 Flybuys points per $1 spent on everyday expenses and redeem a variety of flight and shopping rewards.

Important information about this website

Finder is a comparison service. We do not compare every product or every provider in the market.

We make money through commercial arrangements with some of the providers on this site. Products marked 'Sponsored', 'Promoted', 'Featured' or 'Advertisement' appear as a result of a commercial arrangement.

Our editorial content, product reviews and any 'Top Pick' designations are prepared independently of these commercial arrangements.

The default order of products in our tables can be influenced by commercial arrangements. You can re-sort or filter using the controls above each table.

Some content on this site may be generated or supported by AI tools. You should verify details directly with the provider.

Finder is one of Australia's leading comparison websites. We are committed to our readers and stand by our editorial principles.

Our comparison service does not include every product or every provider in the market. Some product issuers offer their products under multiple brands or through associated companies. Where we can, we identify the underlying issuer so you can compare like with like, but you should always check with the provider directly to confirm which brand you are dealing with.

Finder is a comparison website and an intermediary. We are not a product issuer and we do not provide personal financial or credit advice. When you click a link to a product, or apply for a product through our site, you deal directly with the product issuer. We may receive a referral fee, commission or other payment from the issuer if you click through, apply or take out a product. We describe these arrangements in more detail under 'How we make money' below.

Product features, fees, terms and eligibility criteria are set by the product issuer and may change. We rely on information supplied by issuers when we present product details on our site. Before you apply for or take out any product, you should confirm the details directly with the issuer.

We earn revenue from Finder in four principal ways:

Referral fees and commissions. When you click a product link, complete an enquiry form or apply for a product through our site, we may receive a referral fee, commission or other payment from the product issuer. We may also receive payment based on the volume of leads or conversions we send to an issuer.

Sponsored placements. Products marked 'Sponsored', 'Promoted', 'Featured' or 'Advertisement' appear as a result of a commercial arrangement between Finder and the issuer. These labels always indicate a paid placement. We do not use them for editorial choices.

Display advertising. Banner advertising, newsletter advertising and similar display ads on our site are paid by advertisers.

Content sponsorship. Some articles, videos and social media posts are sponsored by an issuer and are clearly labelled as such.

Our editorial opinions, product reviews and any 'Top Pick' designations are prepared independently of these commercial arrangements. A 'Top Pick' is an editorial choice made by our writers and editors based on the criteria described on each comparison page. A 'Top Pick' is not a personal recommendation and does not mean the product is appropriate for your circumstances.

If you would like to know whether we have a commercial arrangement with a specific product issuer, please contact us.

When products are grouped in a table or list, the default order can be influenced by commercial arrangements we have with product issuers. In some categories, sponsored or featured products appear in the top positions of the table by default, and are always labelled as such.

Other factors that influence default order include price, fees and features, and (where relevant) our editorial view of the product.

You can re-sort every comparison table using the controls above the table. You can filter by product features that matter to you. The order you see after re-sorting or filtering is not influenced by commercial arrangements.

Some content on this site is generated or supported by artificial intelligence tools, including our AI-powered assistant FinderBot. AI-generated content may contain errors. Please verify important information directly with the product issuer before making a financial decision. For more information about FinderBot, see the FinderBot Terms of Use and FinderBot Privacy Collection Notice.

Please read our website terms of use and privacy policy for more information about our services and our approach to privacy.

We update our data regularly, but information can change between updates. Confirm details with the provider you're interested in before making a decision.

Our goal is to create the best possible product, and your thoughts, ideas and suggestions play a major role in helping us identify opportunities to improve.

How do i add my Woolworths Rewards card to my iphone wallet?

Hi Susie,

It looks like you can use this link on the Woolworths website and enter your card and mobile numbers.

I would like a card with points accumulated when i use to shop at groceries and points to put towards my trips when i fly?

Hi Sandy, If your goal is to earn points with grocery shopping, then a good approach is to get a credit card that earns airline points and is also partnered with a major supermarket – that way, you can earn points from paying with the card, and also convert your supermarket loyalty points into additional airline points. Qantas is partnered with Woolworths/Everyday Rewards, while Virgin/Velocity is partnered with Coles/Flybuys, so exploring cards that earn with either of those airlines could help you earn more points. Have fun exploring!

Can I use diners club rewards with Emirates?

Hi Ron,

Thanks for your inquiry.

Yes, the Diners Club Rewards program also allows you to transfer your reward points to 17 airline and travel loyalty programs, including Virgin Australia’s Velocity frequent flyer program, Emirates Skywards, Etihad Guest, and Hilton Honors.

You can learn more about Diners Club Rewards program.

Best regards,

Rench

I spend and pay off in full about 25K per month of normal spending on my Citi Signature card which since the 1st July 2017 have at best halved their reward points which I use for Qantas flights.

What is the best card now for me to get the most points for my spend per month, ie who is dollar for dollar and uncapped

Hi Kym,

Thank you for your inquiry.

While we cannot recommend what is best for you, we can offer you general information. You can check the list of frequent flyer credit cards featured on our website to learn more.

I hope this information has helped.

Cheers,

Harold

Since the rules for the credit card reward points that you earn are changing as of the 1st July 2017, what would be the best rewards card that you can earn points for make payments to the ATO? Currently have a Westpac Altitude Rewards card and this is changing from 1st of July 2017 where you no longer receive points for ATO payments.

Hi Maz,

Thanks for your comment.

Please read more about the credit cards that let you earn points when making payments to the ATO. Compare the credit cards that earn points for tax payments and after you’re done comparing, select the “Go to Site” button to be redirected to the bank’s website to apply.

I hope this helps.

Regards,

Jhezelyn