These products offer the best value and outcomes considering various product features and price.

7+

Great

Competitive products within their group.

5+

Standard

But these products still offer reasonable value and have the basics sorted.

0+

Basic

Offering basic cover with limited features or higher pricing.

Compare car insurance for rideshare drivers

4 of 4 results

Compare other products

We currently don't have that product, but here are others to consider:

How we picked these

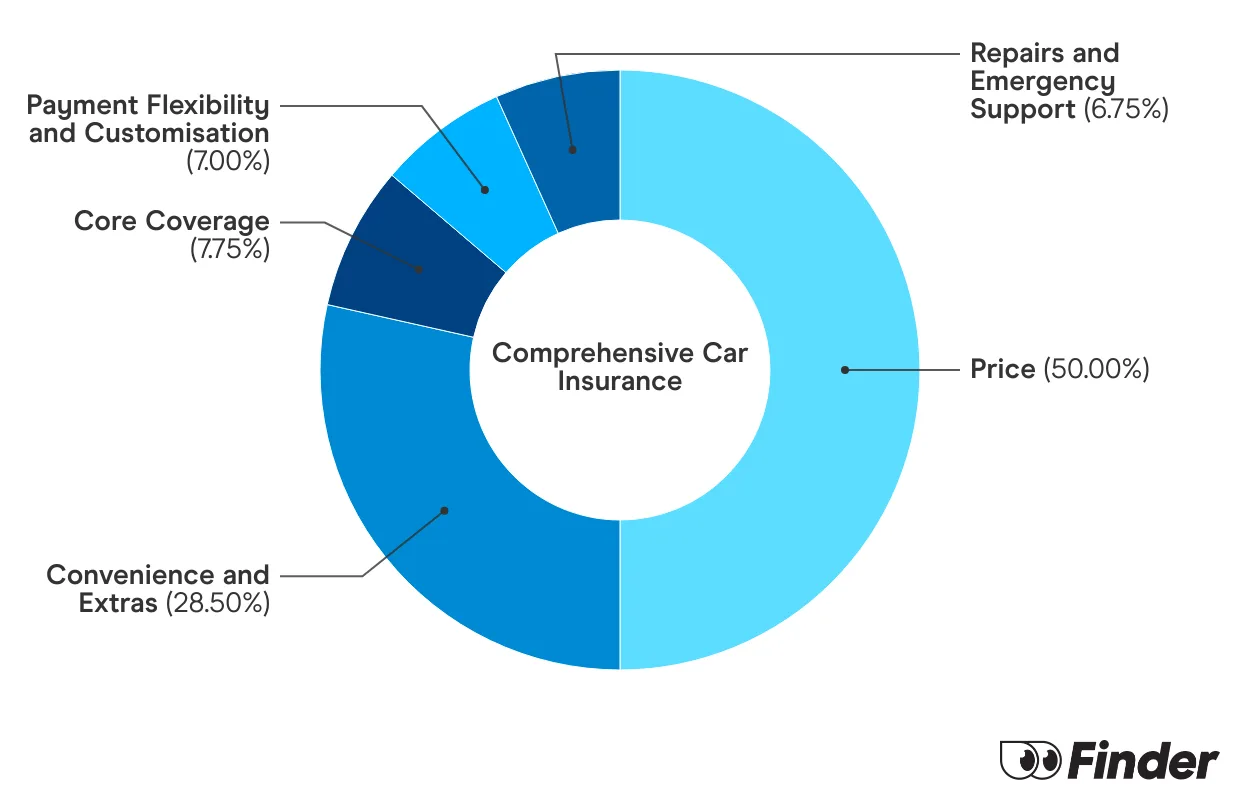

Finder Score for car insurance

We analyse over 30 car insurance products across insurance providers, and rate each one for price and features. We collect up to 36 quotes per product, for male and female drivers in New South Wales, Victoria, Queensland, South Australia, Tasmania and Western Australia. Quotes are collected for 20 year olds, 30 year olds and 60 year olds, assuming an excess of $850 for a 2020 Toyota Corolla 4 door sedan model, with an average 15,000 kms driven each year. While we are not allowed to display actual quotes, our Finder Score aims to serve as an indicative guide to how cost and feature competitive a product might be for you.

Our feature score assesses each product for more than 15 features across loss and damage coverage, repairs and assistance coverage, personal items coverage and policy coverage. Features we assess include but are not limited to legal liability, essential repairs, new car replacement, car hire events, roadside assistance, agreed or market value, windscreen damage and natural disaster coverage.

Depending on your answers to our car insurance quiz, we upweight the relevant price score or feature score to generate a dynamic Finder Score. Finder Score, Price Score and Feature Score are only to be used as indicative guides and are not product recommendations.

Finder survey: Do Australians find it hard to get car insurance that covers rideshare drivers?

Response

No

50%

Yes

50%

Source: Finder survey by Pure Profile of 1006 Australians, December 2023

Rideshare insurance pricing

We got quotes from a few popular car insurers to see what a quote for a rideshare driver could look like. Keep in mind, the below costs are only for the driver profile we used and your own costs will differ based on your age, car, suburb and driving experience.

Provider

~Annual cost

QBE

$3,351.95

Kogan

$3,640.70

Bingle

$3,597.64

To get these quotes, we used the following details:

35yr old male

Sydney based postcode

Drives a 2019 Toyota Corolla

Drives up to 15 hours for a rideshare service

These quotes were sourced in February 2026.

Why is rideshare car insurance important for rideshare drivers?

If you haven't told your insurer that you're an Uber driver or other rideshare driver, it may refuse to cover you for any accidents that occur while you're working.

Many insurers still don't cover ridesharing. For example, popular insurers such as Budget Direct, Qantas, Coles and Huddle do not cover your car at any time for ridesharing. Others, such as ANZ, will only cover you if you drive less than 32 hours per week.

Rideshare car insurance requirements for different services

Rideshare platforms typically offer some kind of liability cover, but in most cases, you'll need to take out your own individual car insurance policy too. Here are the insurance requirements of each rideshare company in Australia.

Uber

What insurance do I need?

Compulsory third party insurance (CTP)

Third party property damage insurance (TPPD)

Driving requirements

You must

Be listed as a driver on your insurance certificate

Be over 21 years old

Have a full valid licence in the state you're driving in

DiDi

What insurance do I need?

Compulsory third party insurance (CTP)

Third party damage or comprehensive insurance cover

Driving requirements

You must

Have a full driver's licence

Have a vehicle insurance certificate

GoCatch

What insurance do I need?

Compulsory third party insurance (CTP)

Third party damage or comprehensive insurance cover

Driving requirements

You must

Have all the necessary insurance documents

Have a police check

Have a vehicle inspection

Have an unrestricted Australian driver's licence

Shebah

What insurance do I need?

Compulsory third party insurance (CTP)

Comprehensive car insurance

Driving requirements

You must

Be at least 21 years old

Have a smartphone

Speak English

Hold an unrestricted Australian driver's licence

Have or set up an ABN

Have access to a 4-door car in good condition

Rydo

What insurance do I need?

Compulsory third party insurance (CTP)

Third party property damage insurance (TPPD)

Insurance must be from a company operating within Australia

Driving requirements

You must

Have a current driver's licence

Have a criminal background check

How do I find the right rideshare car insurance cover?

Watch out for a cap on hours you can drive

A small number of rideshare insurance policies will only cover you if you drive less than a specified amount per week, often around 32 hours (we've outlined these in the table above). If you're ridesharing for more than that, opt for a provider with no limit.

Decide what level of cover you want

You are required by most rideshare services to have CTP and third party property insurance. This doesn't cover you for damage to your own car though; if you want cover for that, you should get a comprehensive car insurance policy.

Decide what you want covered

All comprehensive rideshare insurance policies should cover you for damage to your own car (usually up to the market value), other people's cars and property, floods, hail, fires and storms. However, features such as a hire car after an accident and windscreen cover, are sometimes optional. (Good to know: you won't be covered for ridesharing a hire car with most insurers but you can still use the vehicle for personal use).

Compare quotes

It's simple to apply for car insurance quotes online, so get multiple policies for a better idea of how much rideshare car insurance costs.

"Don't just assume that your car insurance will cover you for ridesharing – lots don't. You will need to contact them and let them know. Fortunately, there are a handful that do. It's worth getting a quote from each of them to see who is cheapest."

Gary Ross Hunter

Insurance editor

"Moving across to an insurer that offers rideshare cover isn't hard. The switching process is simple once you've found a replacement policy that meets your rideshare needs. I reviewed more than a dozen policies – most insurers charge no more than $40 in cancellation fees."

James Martin

Editor for Insurance

"If you’re unsure if your insurer offers coverage for ridesharing, it’s always best to check. It’s usually pretty straightforward; you can give them a call, go online and ask their live chat or just use “command+f” to search the PDS for “rideshare”. If it’s still not made clear, it could mean you won’t be covered and it’s time to start looking elsewhere."

Peta Taylor

Associate publisher

What does rideshare car insurance cover if I have an accident?

CTP insurance can provide cover for death or injury to a third party.

A third party property damage policy can cover damage to another driver's vehicle or property.

If you have a comprehensive rideshare car insurance policy in place, you'll also be covered for damage to your own vehicle (as well as others).

There are a few injuries and accidents where rideshare car insurance won't cover you. For example, certain personal injuries, such as broken bones, or cover if you can't work. This is where your rideshare platform's injury insurance can help.

Key takeaways

Driving for rideshare services like Uber requires specific rideshare car insurance as standard policies do not cover commercial passenger transport. Failure to inform your insurer can void your policy and lead to denied claims.

All major rideshare services in Australia mandate at least compulsory third party insurance (CTP) and third party property damage (TPPD) cover. For damage to your own vehicle comprehensive rideshare car insurance is necessary.

When selecting rideshare insurance drivers should check for caps on driving hours, decide on the desired level of cover and compare quotes from multiple providers to find the most suitable and cost-effective option.

Becoming a rideshare driver will likely increase car insurance premiums due to higher risks and vehicle usage. However a percentage of car insurance costs proportional to business use can be claimed as a tax deduction.

Why you can trust Finder's car insurance experts

You pay nothing. Finder is free to use. And you pay the same as going direct. No markups, no hidden fees.

You save time. We spend 100s of hours researching car insurance so you can sort the gold from the junk faster.

You can trust us. We say it like it is. We aren't owned by an insurer and our opinions are our own.

Frequently asked questions

If you drive for Uber, Lyft or another ridesharing service then yes, you will need rideshare car insurance. An ordinary car insurance policy only covers private use of your vehicle and doesn't cover you if you use your car to carry passengers for profit.

The exact process varies between insurers, but you'll typically be able to select the ridesharing option during the application process when asked if you use your car for business purposes.

You don't need a special business car insurance policy to drive for Uber. You simply need to select that you will use your car for business purposes when you take out car insurance. Insurers will ask you this during the application process.

Yes, if you drive for Uber or any other rideshare company, you'll need to tell your car insurance provider. If you don't, your car insurance policy might be void and any claims you make will be denied. Many insurers automatically exclude transporting passengers for money with a personal car insurance policy unless you let them know.

Yes, you should be able to claim tax deductions on your car insurance. However, you can only deduct the percentage proportional to how much you used the vehicle for work (e.g. business use). Keep a logbook of how much you worked to make calculating this easier. There are other business expenses you can claim, such as the following:

Fuel expenses

Your rideshare platform's fees

Car registration

Repair and maintenance costs

Cleaning costs

Parking fees

Depreciation on your car's purchase price if you are the owner of the car

Rental fees if you lease or rent the car

Tolls that were not covered by your rideshare platform

Mobile and internet expenses if you use your phone for ridesharing

Make sure you keep receipts and bank records related to these expenses so that you can claim a percentage of them come tax time.

The cost of this policy addition will depend on how frequently you rideshare as well as where you live, the type of car and your driving history.

Your CTP insurance covers medical and liability costs sustained by passengers in vehicle accidents while you're driving. Uber's insurance policy can also cover passenger medical and liability costs where your own insurance won't. You will need to pay the excess that applies to this cover.

Yes. A rideshare car insurance policy typically also covers you for the private use of your car.

Yes, driving for Uber or any other rideshare company will likely increase your car insurance costs. There are more risks involved so your premiums are likely to increase. These risks can include potential legal fees if you're involved in a crash or a passenger opening the door and causing an accident. You're also using the car more often, so there's a greater chance of an accident occurring. You might pay a higher premium, but if something happens, you'll be covered.

Uber drivers in Australia must have compulsory third party (CTP) insurance for their state or territory of residence and a minimum of third party property damage insurance, with the driver listed as a policyholder or named insured driver.

If you do not inform your insurer that you use your vehicle for rideshare services, your car insurance policy might be void and any claims you make could be denied. Many personal car insurance policies automatically exclude transporting passengers for payment.

Yes, a comprehensive rideshare insurance policy typically covers you for both ridesharing activities and personal use of your vehicle. Some providers, such as Suncorp, specifically mention 24/7 coverage.

Yes, your Compulsory Third Party (CTP) insurance generally covers compensation claims if you cause injury or death to your passengers in a car accident. Some rideshare policies may also offer additional personal accident benefits.

CTP (Compulsory Third Party) insurance is mandatory across Australia and protects drivers against the financial impact of causing injury or death in a motor vehicle accident, including coverage for any passengers. It is a legal requirement for vehicle registration and the minimum insurance requirement for all major rideshare providers.

Sources

Was this content helpful to you?

Thank you for your feedback!

To make sure you get accurate and helpful information, this guide has been edited by

James Martin

as part of our

fact-checking process.

Gary Ross Hunter has over 6 years of expertise writing about insurance, including life, health, home, and car insurance. Having reviewed hundreds of product disclosure statements and published over 800 articles, he loves simplifying complex insurance topics for everyday readers. Gary has contributed to major outlets like Yahoo Finance, The Sydney Morning Herald, and news.com.au, and holds a Bachelor of Arts (Honours) in English Literature from the University of Glasgow, along with a Tier 2 General Advice certification, ensuring his work adheres to ASIC’s RG146 standards.

See full bio

Gary Ross's expertise

Gary Ross

has written

577

Finder guides across topics including:

This article runs through the ins and outs of choosing a good third party property damage car insurance policy.

Important information about this website

Finder makes money from featured partners, but editorial opinions are our own.

Finder is one of Australia's leading comparison websites. We are committed to our readers and stand by our editorial principles.

We try to take an open and transparent approach and provide a broad-based comparison service. However, you should be aware that while we are an independently owned service, our comparison service does not include all providers or all products available in the market.

Some product issuers may provide products or offer services through multiple brands, associated companies or different labeling arrangements. This can make it difficult for consumers to compare alternatives or identify the companies behind the products. However, we aim to provide information to enable consumers to understand these issues.

We make money by featuring products on our site. Compensation received from the providers featured on our site can influence which products we write about as well as where and how products appear on our page, but the order or placement of these products does not influence our assessment or opinions of them, nor is it an endorsement or recommendation for them.

Products marked as 'Top Pick', 'Promoted' or 'Advertisement' are prominently displayed either as a result of a commercial advertising arrangement or to highlight a particular product, provider or feature. Finder may receive remuneration from the Provider if you click on the related link, purchase or enquire about the product. Finder's decision to show a 'promoted' product is neither a recommendation that the product is appropriate for you nor an indication that the product is the best in its category. We encourage you to use the tools and information we provide to compare your options.

Where our site links to particular products or displays 'Go to site' buttons, we may receive a commission, referral fee or payment when you click on those buttons or apply for a product.

When products are grouped in a table or list, the order in which they are initially sorted may be influenced by a range of factors including price, fees and discounts; commercial partnerships; product features; and brand popularity. We provide tools so you can sort and filter these lists to highlight features that matter to you.

Please read our website terms of use and privacy policy for more information about our services and our approach to privacy.

We update our data regularly, but information can change between updates. Confirm details with the provider you're interested in before making a decision.

How likely would you be to recommend Finder to a friend or colleague?

0

1

2

3

4

5

6

7

8

9

10

Very UnlikelyExtremely Likely

Required

Thank you for your feedback.

Our goal is to create the best possible product, and your thoughts, ideas and suggestions play a major role in helping us identify opportunities to improve.

The information provided by Frankie is general in nature and has been prepared without considering your objectives, financial situation or needs. Frankie may make mistakes so it's important that you review the information before deciding. By messaging Frankie, you agree to our Terms and have read our Privacy Policy.

You pay nothing. Finder is free to use. And you pay the same as going direct. No markups, no hidden fees.

You pay nothing. Finder is free to use. And you pay the same as going direct. No markups, no hidden fees.

You save time. We spend 100s of hours researching car insurance so you can sort the gold from the junk faster.

You save time. We spend 100s of hours researching car insurance so you can sort the gold from the junk faster.

You can trust us. We say it like it is. We aren't owned by an insurer and our opinions are our own.

You can trust us. We say it like it is. We aren't owned by an insurer and our opinions are our own.