Contents insurance covers only the items inside your home, like your furniture, your TV, appliances and more.

Contents insurance is ideal for renters, students or property owners who don't need building cover.

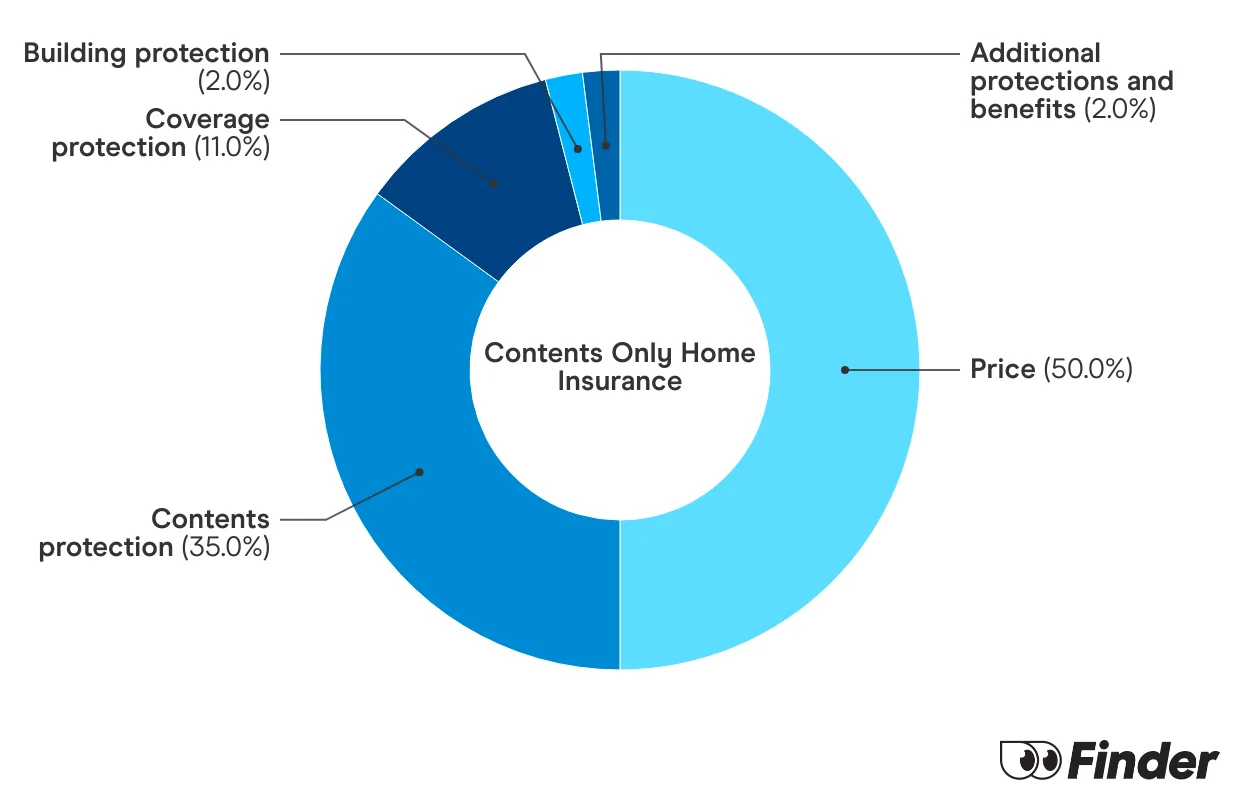

Customising your cover is key to getting the most value out of your policy.

What is contents insurance?

Contents insurance is a type of home insurance that covers the items inside your home, such as your TV, furniture or art, without providing any cover for the actual building.

You can buy contents insurance as a standalone policy or bundle it with building/home insurance.

Usually, contents insurance is highly customisable. You may be able to add cover for items you take outside of the home as well as for high-value items.

What does contents insurance cover?

Most items within your home will be covered by your contents insurance. Although they vary slightly between insurance brands, the following are some common inclusions:

While contents insurance can cover many things, it’s important to keep an eye on sub-limits. For example, jewellery may be covered but it may have a limit of up to $5,000. This means if your jewellery exceeds this cost, you can’t claim back more than $5,000. That’s worth keeping in mind if you’ve got an expensive ring or watch that you plan to insure.

When am I covered?

Contents insurance kicks in when your belongings are damaged in a specific way. These are called insured events. Take a look at the events below so you know when you'll be covered. Keep in mind, every insurer is different and ‘insured events’ can vary between providers. It’s always best to read your product disclosure statement (PDS) to know exactly what you’re covered for.

⚠️ You won't be covered for general wear and tear, including chips, scratches and dents.

Who needs contents insurance?

Anyone who keeps expensive or valuable items in their home should consider contents insurance. As contents insurance only covers items within a home, not the building, contents insurance is highly recommended for:

Renters: Renters are not responsible for protecting the structure of the building they live in. This responsibility is on the landlord or the owner of the building who will most likely have landlord or building insurance.

Those who own an apartment: If you own the apartment you live in, as the physical structure of the building and common areas are typically covered by a strata insurance policy.

Property owners: Those who own a dwelling will need home and contents insurance to protect their personal belongings and the physical structure of their home.

Sum insured vs total replacement: what’s the difference?

When you begin browsing contents insurance policies, you’ll notice insurers give you the option to have your covered as either sum insured or total replacement.

Under sum insured contents insurance, you will be responsible for setting the amount you want your items to be covered for. Total replacement is where the insurer agrees to cover the full cost of replacing your contents with new items of equivalent quality and standard.

There is no “better” option of the two, so the choice you make will come down to what you’re more comfortable with. It is worth noting that sum insured policies do carry the risk of underinsurance, as items depreciate in value. On the other hand, you may face a higher premium with total replacement, as insurers take on a larger financial risk in this scenario.

How much does contents insurance cost?

We got quotes from 14 different home insurers and found that policies can start from $23 a month.

When you get a quote from an insurer, it will probably vary from these prices because it's entirely based on the value of your stuff. But at least you get an idea, right?

Here's the rest of the research so you can see how different insurers stack up against each other on a monthly and annual basis.

We rounded all the quotes to the nearest dollar. The customer profile had no previous claims and a $500 excess.

Learn more about our methodology

Quotes were obtained for the same three-bedroom New South Wales home in Baulkham Hills owned by a family of two.

Homeowning family of two who moved into their property in January 2019.

Quotes were obtained in February 2026 and were for contents insurance only.

Three-bedroom, one story freestanding house on flat ground with brick veneer walls, terracotta tiled roof, no verandas and built in 1980.

Windows secured by deadlocks, with no security devices.

How much contents insurance do I need?

This is entirely dependent on how much stuff you have and how valuable it is. Between different types of furniture, appliances and other sentimental items, no two people have the same set of belongings. To get the most accurate estimate of how much contents insurance you need, we recommend:

Going from room to room, listing and valuing every time. This helps prevent you from becoming overwhelmed.

Remember: Contents insurance covers everything from simple cosmetics and toiletries to expensive furniture and artwork. Try not to overlook anything.

How can I get the most out of contents insurance?

Contents insurance comes with heaps of cool benefits. Some are included as standard, while others you can pick and choose. Take a look at some examples below.

Lots of policies will pay out if an insured event ruins the food in your home. For example, a burst pipe cuts the power and everything in your freezer is ruined.

Motor burnout

This option covers you for loss or damage to electric motors, commonly found in appliances like fridges, freezers or washing machines.

Vet's expenses

Some policies will pay a benefit if your pet suffers an injury as the result of an insured event.

Specified items

Contents insurance sets a limit for the amount you can claim per item. If you have any high-value items, be sure to specify them.

How to save on contents insurance

For the level of protection you get, contents insurance is pretty affordable. But there are still ways to cut the cost of cover and score a serious bargain.

Shop around. It’s our job to compare the differences between policies and their pricing and let me tell you, there’s some pretty insane price differences for almost identical coverage. It’s always worth comparing at least 5 providers to make sure you’re not being ripped off.

Look for discounts. Insurance companies often run deals to attract new customers. You can usually get up to 15% off a new contents policy. Check them out here.

Bundle cover. Some insurance brands will reduce the cost of your premium if you have more than one type of cover. Consider bundling your car insurance to save more cash.

Pay annually. You'll usually get a discount if you pay annually rather than monthly. Some insurers will also give you a discount if you buy online rather than over the phone.

Raise your excess. Choosing a higher excess will reduce the cost of your premium, but make sure the excess is affordable. There's no point pricing yourself out when it comes to claim time.

Don't be shy. Ask the insurer if there's any way you can get a better deal. They might be able to tell you about an offer that's running or give you a price cut.

What isn't covered by contents insurance?

Contents insurance helps in heaps of different situations, but it won't cover everything. Here are some common exclusions to be aware of:

Contents insurance covers most of your belongings kept inside the home. You don't need to insure the building since that's the landlord's responsibility.

It'll also cover some semi-permanent features – like air-con units, ovens and carpets – as long as you paid for them.

Landlord insurance covers both the fixtures and fittings inside your property, including built-in wardrobes, shelving units, ceiling fans and kitchen countertops.

You can also add cover for malicious damage and tenant default.

These products offer a balance between low pricing and more features.

7+

Great

Competitive products within their group.

5+

Standard

Usually these products would either have fewer benefits or higher pricing.

0+

Basic

Offering basic cover with limited features or higher pricing.

Finder Score - Home Insurance

We crunch eligible home insurance products in Australia to see how they stack up. We rank over 50 products on 16 different features, including price. We end up with a single score out of 10 that helps you compare home insurance a bit faster. We assess home and contents, building only and contents only products individually.

You know we can’t give you a straightforward answer. The “best” contents insurance policy for you is one that provides adequate coverage at a price range within your budget.

Contents insurance covers a wide range of items within your home, including carpets, electrical appliances, furniture, plants, clothing, jewellery and much more. Every insurer offers varying levels of cover, so ensure you read through the PDS carefully before signing up to a policy.

This is tricky to answer, as it will depend on your personal circumstances and the items you need covered. According to our research, the annual cost of a contents insurance policy ranges from $300 to $500 for items worth a combined $50,000. This is why it’s important to shop around and obtain at least 3 quotes before purchasing a policy.

Absolutely. Whether you’re covering essential or sentimental items, contents insurance can ensure you’re covered when disaster strikes. Events like break-ins or accidental damage are a lot more common than you think, so it’s always better to be safe than sorry. Contents insurance can give you one less thing to worry about during life’s most unforeseen moments.

There is no definitive answer to this question, but it’s recommended you revisit your contents insurance policy at least once a year, generally around renewal time. This can ensure you are adequately covered and not at risk of being underinsured, as the cost to replace items changes.

If the contents belongs to the renter, then the renter will pay for the contents insurance. Landlords can opt to take out contents insurance but it’d only cover their own belongings, like the oven or the dishwasher, if they’ve provided that in the house. Their policy won’t cover your belongings, only your own policy can do that.

Most policies require you to pay an excess when you make a claim. However, many insurers allow you to adjust your excess to vary your premium amount, so contact your insurer to find out the minimum excess available.

Yes, it's still possible to have your claim paid even if you haven't kept receipts. The insurer will ask you to show proof of ownership, which you may be able to do by providing photographs of the items in your house, warranty cards, instruction manuals, valuation certificates, original packaging, credit card statements and, in some cases, serial numbers. Contact your insurer for details of what they will accept as proof of ownership if you are unable to provide receipts.

If you live in a granny flat, and don't own it, then contents insurance could be the right way to go. You won't need cover for the building since the owner or landlord should have that part covered.

You can buy contents insurance online or by contacting an insurer over the phone.

There are two ways to look at this. Firstly, if something happens to your pet as the result of an insured event, some providers may cover their injuries, up to a certain limit. Secondly, if your pet causes damage to your contents, this isn’t covered. For example, your dog eats your expensive jewellery or ruins your carpet - that won’t be covered.

Yes, to a certain value. Insurers put a cap on the amount you can claim per piece of jewellery. If your ring is worth more than that, don't worry. You can list the item on your insurance policy, with its value, and have peace of mind that it's properly covered.

If you want cover for items when they’re outside of the home, you’ll need to add portable contents insurance to your policy. You can cover things like your bicycle, expensive jewellery and handbags. Typically, you can’t cover things like your mobile phone.

Nicola Middlemiss is a journalist with nearly a decade of experience in personal finance and insurance. She has contributed to Domain, Yahoo Finance, Money Magazine and Insurance Business Australia, offering in-depth insights into commercial insurance in the Australian market. Nicola holds a Bachelor’s degree in English from the University of Leeds and a Tier 1 General Insurance (General Advice) certification, which complies with ASIC standards.

See full bio

Nicola's expertise

Nicola

has written

256

Finder guides across topics including:

Personal finance

Personal insurance, including car, health, home, life, pet and travel insurance

Peta Taylor is a publisher at Finder, working across all of insurance. She's been analysing product disclosure statements and publishing articles for over 2 years. Peta is passionate about demystifying complex insurance products to help users make well educated decisions with confidence. Peta is part of Finder's insurance awards team and works alongside editorial and insights experts to bring users the best insurance products every year.

See full bio

Find out more about watch insurance and how to get cover.

Important information about this website

Finder makes money from featured partners, but editorial opinions are our own.

Finder is one of Australia's leading comparison websites. We are committed to our readers and stand by our editorial principles.

We try to take an open and transparent approach and provide a broad-based comparison service. However, you should be aware that while we are an independently owned service, our comparison service does not include all providers or all products available in the market.

Some product issuers may provide products or offer services through multiple brands, associated companies or different labeling arrangements. This can make it difficult for consumers to compare alternatives or identify the companies behind the products. However, we aim to provide information to enable consumers to understand these issues.

We make money by featuring products on our site. Compensation received from the providers featured on our site can influence which products we write about as well as where and how products appear on our page, but the order or placement of these products does not influence our assessment or opinions of them, nor is it an endorsement or recommendation for them.

Products marked as 'Top Pick', 'Promoted' or 'Advertisement' are prominently displayed either as a result of a commercial advertising arrangement or to highlight a particular product, provider or feature. Finder may receive remuneration from the Provider if you click on the related link, purchase or enquire about the product. Finder's decision to show a 'promoted' product is neither a recommendation that the product is appropriate for you nor an indication that the product is the best in its category. We encourage you to use the tools and information we provide to compare your options.

Where our site links to particular products or displays 'Go to site' buttons, we may receive a commission, referral fee or payment when you click on those buttons or apply for a product.

When products are grouped in a table or list, the order in which they are initially sorted may be influenced by a range of factors including price, fees and discounts; commercial partnerships; product features; and brand popularity. We provide tools so you can sort and filter these lists to highlight features that matter to you.

Please read our website terms of use and privacy policy for more information about our services and our approach to privacy.

We update our data regularly, but information can change between updates. Confirm details with the provider you're interested in before making a decision.

How likely would you be to recommend Finder to a friend or colleague?

0

1

2

3

4

5

6

7

8

9

10

Very UnlikelyExtremely Likely

Required

Thank you for your feedback.

Our goal is to create the best possible product, and your thoughts, ideas and suggestions play a major role in helping us identify opportunities to improve.

The information provided by Frankie is general in nature and has been prepared without considering your objectives, financial situation or needs. Frankie may make mistakes so it's important that you review the information before deciding. By messaging Frankie, you agree to our Terms and have read our Privacy Policy.