These products offer a balance between low pricing and more features.

7+

Great

Competitive products within their group.

5+

Standard

Usually these products would either have fewer treatments covered or higher pricing.

0+

Basic

Offering basic cover with limited features or higher pricing.

FINDER REWARDS EXCLUSIVE

Health Insurance - Hospital & Extras

ENDS SOON

Get $500 from Finder

Join HBF with eligible Hospital & Extras cover via Finder and earn a $500 digital Visa card. Eligible new members may also receive up to 14 weeks free on eligible Hospital & Extras policies from HBF. Offer ends on or before 30 June 2026.

T&Cs and eligibility apply.

Join HBF with eligible hospital cover via Finder and earn a $200 digital Visa card. Eligible new members may also receive 6 weeks free on eligible hospital-only policies from HBF. Offer ends on or before 30 June 2026.

T&Cs and eligibility apply.

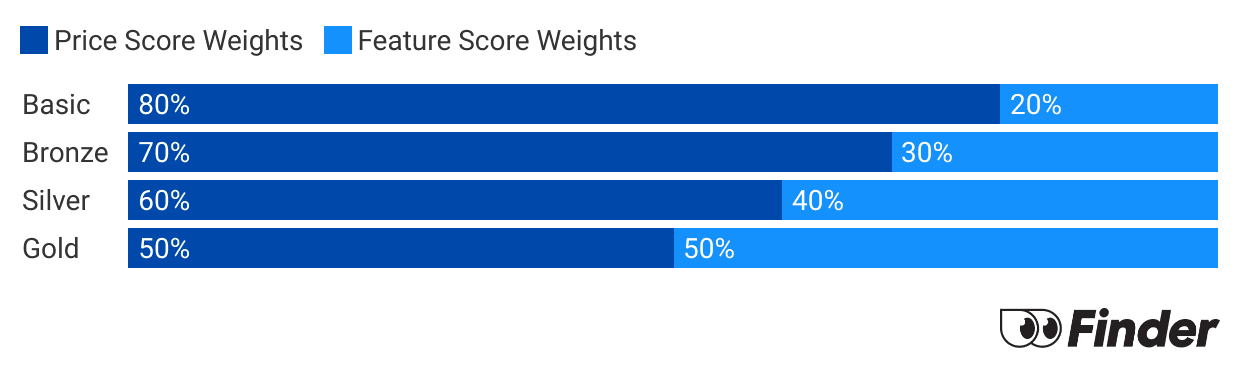

Each month we analyse over 10,000 hospital and extras insurance products and rate each one on price and features. What we end up with is a nice round number out of 10 that helps you compare products a bit faster.

Before we start scoring, we need to make sure we're comparing like-for-like. Just as it doesn't make sense to compare a toy car with a Porche, it doesn't make sense to compare basic policies to top-tier gold policies. Each policy is given a price score and feature score. These are then combined to determine each policies's Finder Score. Read our full methodologies of how we calculated Finder Score for hospital cover and extras cover.

What do Australians think of HBF health insurance?

4.18/5 overall for Customer Satisfaction - higher than the average of 4.13

4.57/5 for Trust - higher than the average of 4.46

4.2/5 for Customer Service - higher than the average of 4.17

HBF App: Download from the App Store or Google Play to claim via the app

myHBF: Claim online through HBF"s digital portal, myHBF

On the spot: Swipe your member card or tap your digital member card when paying

At a branch: Visit your nearest HBF branch

Mail: Return a claim form by mail to HBF, GPO Box 1440, Perth WA 6845

Complaints info

HBF has a fantastic record on complaints. We regularly analyse Ombudsman complaints data to see which health funds receive more or less complaints compared to their market share. The most recent State of the Health Funds Report data has HBF with 8.10% of market, but accounted for only 2.20% of complaints received. That's better than all the major health funds by a really wide margin.

Congratulations, HBF!

HBF is the most awarded health insurance provider in the Finder Product Awards since 2022. In 2025, HBF was highly commended in the Core Extras Health Insurance category.

Health Insurance - Bronze Hospital - Highly Commended 2024<

Health Insurance - Gold Hospital - Highly Commended 2024<

Winner for Best Fund 2023

Winner for Best Health Insurance - Basic Hospital 2023

Winner for Best Health Insurance - Medium Extras 2023

Finalist for Best Health Insurance - Silver Hospital 2023

Finalist for Best Health Insurance - Bronze Hospital 2023

FAQs

HBF offers a range of hospital and extras policies that cover various medical treatments, procedures, and expenses. The specific will depend on which policy you take out.

No. HBF and HCF are separate entities.

HBF stands for the Hospital Benefit Fund. It was initially founded in 1941 as the Metropolitan Health Fund but has since evolved to become HBF.

Nicola Middlemiss is a journalist with nearly a decade of experience in personal finance and insurance. She has contributed to Domain, Yahoo Finance, Money Magazine and Insurance Business Australia, offering in-depth insights into commercial insurance in the Australian market. Nicola holds a Bachelor’s degree in English from the University of Leeds and a Tier 1 General Insurance (General Advice) certification, which complies with ASIC standards.

See full bio

Nicola's expertise

Nicola

has written

249

Finder guides across topics including:

Personal finance

Personal insurance, including car, health, home, life, pet and travel insurance

Private health insurance provides coverage beyond Medicare. It can make in-hospital healthcare more convenient and everyday healthcare costs more affordable. Learn more.

This guide looks at the reasons people switch, and what it means for your waiting periods. You can also compare new options with over 30 Australian health funds.

Australians don’t need private health insurance. However, a health insurance policy can cover some treatments that Medicare does not. You’ll also get faster treatment, plus tax benefits.

Learn how to get cheap health insurance and what you can expect for your money.

Important information about this website

Finder makes money from featured partners, but editorial opinions are our own.

Finder is one of Australia's leading comparison websites. We are committed to our readers and stand by our editorial principles.

We try to take an open and transparent approach and provide a broad-based comparison service. However, you should be aware that while we are an independently owned service, our comparison service does not include all providers or all products available in the market.

Some product issuers may provide products or offer services through multiple brands, associated companies or different labeling arrangements. This can make it difficult for consumers to compare alternatives or identify the companies behind the products. However, we aim to provide information to enable consumers to understand these issues.

We make money by featuring products on our site. Compensation received from the providers featured on our site can influence which products we write about as well as where and how products appear on our page, but the order or placement of these products does not influence our assessment or opinions of them, nor is it an endorsement or recommendation for them.

Products marked as 'Top Pick', 'Promoted' or 'Advertisement' are prominently displayed either as a result of a commercial advertising arrangement or to highlight a particular product, provider or feature. Finder may receive remuneration from the Provider if you click on the related link, purchase or enquire about the product. Finder's decision to show a 'promoted' product is neither a recommendation that the product is appropriate for you nor an indication that the product is the best in its category. We encourage you to use the tools and information we provide to compare your options.

Where our site links to particular products or displays 'Go to site' buttons, we may receive a commission, referral fee or payment when you click on those buttons or apply for a product.

When products are grouped in a table or list, the order in which they are initially sorted may be influenced by a range of factors including price, fees and discounts; commercial partnerships; product features; and brand popularity. We provide tools so you can sort and filter these lists to highlight features that matter to you.

Please read our website terms of use and privacy policy for more information about our services and our approach to privacy.

We update our data regularly, but information can change between updates. Confirm details with the provider you're interested in before making a decision.