These products offer a balance between low pricing and more features.

7+

Great

Competitive products within their group.

5+

Standard

Usually these products would either have fewer treatments covered or higher pricing.

0+

Basic

Offering basic cover with limited features or higher pricing.

Key takeaways

IVF treatment costs often exceed $8,000 per cycle, but Medicare and Gold tier health insurance can reduce expenses.

Gold tier hospital cover typically includes inpatient IVF services, anaesthetist fees and doctor fees after a 12 month waiting period.

Gold tier policies usually cost around $300 per month.

Health insurance for IVF and other fertility treatments

We researched Finder partners to compare the hospital policies that offer cover for IVF and reproductive services (for example other treatments such as GIFT.) The options below have a 12 month waiting period.

Finder survey: Why do people have hospital insurance?

Response

Female

Male

For pregnancy cover

3.07%

1.04%

Source: Finder survey by Pure Profile of 1006 Australians, December 2023

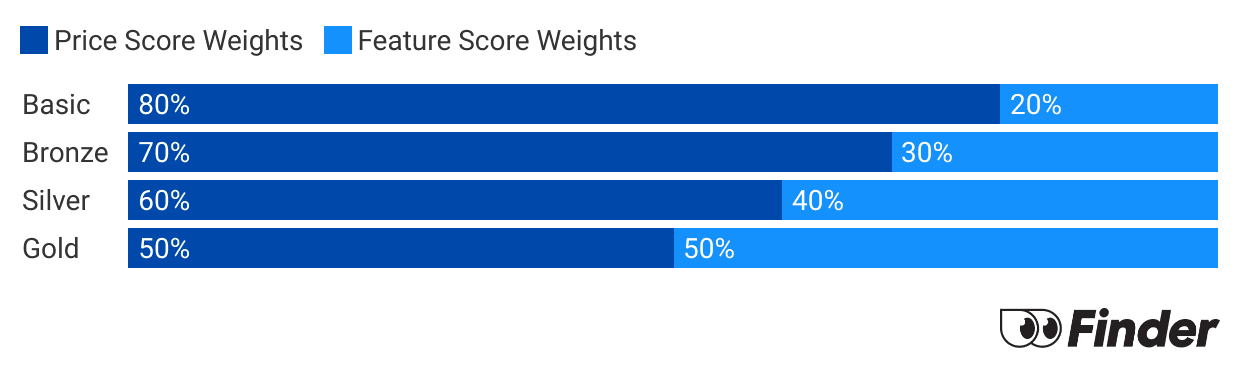

Finder Score - Hospital cover health insurance

Each month we analyse our hospital insurance products and rate each one on price and features. What we end up with is a nice round number out of 10 that helps you compare hospital cover a bit faster.

Before we start scoring, we need to make sure we're comparing like-for-like. Just as it doesn't make sense to compare a bicycle with a Ferrari, it doesn't make sense to compare basic hospital policies to top-tier Gold policies. Each policy is given a price score and feature score. These are then combined to determine each policies's Finder Score.

All prices are based on a single individual with less than $105,000 income and living in Sydney.

"My partner and I went through IVF for our first child. We found the treatment was split into two buckets, your IVF specialists costs and the day surgery for the egg retrieval. The whole cycle cost $12,000, the Medicare Rebate offered us the most back at $5000. Insurance did give us a small rebate back of around $1000 but we mostly got the cover for pregnancy should we be successful as both treatments are covered under a Gold Tier policy. There's a 12 month wait period too, so you have to plan early!"

As long as you have a referral from your GP, Medicare will cover a portion of your IVF for as many cycles, or rounds of treatment, as you need. Most IVF centres are privately run and you will have most of your treatment in their private outpatient facilities and, to a lesser extent, their private day hospitals.

Even though it takes place in a private clinic, Medicare will give you a rebate for many aspects of your IVF treatment even if you don't have private health insurance. By the time it's all said and done, your rebates per IVF cycle will be about 50% of the total cost.

How much does Medicare pay for IVF?

All of the services covered by Medicare are listed in the Medicare Benefits Schedule (MBS). The MBS describes the individual inpatient and outpatient services they cover, along with a dollar amount that equals what Medicare will pay for that service in a public facility. This is called the schedule fee.

But since you’ll be in a private facility, they will only pay a portion of the schedule fee, and even then, only for some services (for example, Medicare will help pay for a doctor to collect your eggs, but they won’t pay anything for you to freeze them).

You’ll be responsible the entire cost of services Medicare doesn’t cover, a portion of the cost of services that Medicare only partially covers, and any additional fees or premiums the clinic decides to charge.

How does private health insurance cover IVF?

Even though Medicare covers a decent chunk of your costs, private health insurance can be an important source of additional cover. Here's where it can help:

Your inpatient services. You know those services that Medicare only covers a portion of? Your private hospital cover will take care of that remaining amount, as long as it is Medicare-approved and you’re being treated as an inpatient (plus it covers related costs like anaesthesia, doctor's fees, accommodation fees and prescriptions that aren't part of the pharmaceutical benefits scheme.

Other prescriptions. If you need any prescriptions as an outpatient, and these aren't part of the pharmaceutical benefits scheme, your private extras policy will cover a percentage of those.

Any inpatient services related to complications. If you come down with a complication due to IVF, such as ovarian hyperstimulation syndrome (OHSS) and you need hospitalised, your insurance will cover you in a private hospital with the doctor you choose.

Childbirth. This isn't technically part of your IVF treatment, but if you use private health insurance for IVF, then you'll most likely also have pregnancy cover. By the time you're ready to give birth, this lets you choose your own obstetrician and hospital, and gives you your own private room.

How much does IVF cost?

A standard IVF cycle can cost anywhere from $9,000 for a normal IVF cycle to $14,000 if you need to have your ovulation induced and you're using a frozen egg (that’s before any refunds or private cover). These rates include consultations, treatments, medications and fees.

The following tables estimate your out-of-pocket costs for one IVF cycle using data from provider IVF Australia.

Cost of IVF before hitting the Medicare Safety Net Threshold

Treatment

Total Cost

Medicare rebate

Estimated out-of-pocket costs

Normal IVF cycle

$9,974

$4,788

$5,051

Frozen embryo transfer (FET)

$3,797

$1,391

$2,354

Ovulation Induction (OI)

$700

$0

$700

Cost of IVF after hitting the Medicare Safety Net Threshold

Since IVF isn't always successful the first time around, you may end up going through multiple cycles and that will push your costs even higher. If you end up having multiple cycles in the same calendar year, Medicare may increase your rebate for the rest of the year if your total out-of-pocket expenses have reached a point called the Medicare Safety Net Threshold (MSNT).

Treatment

Total Cost

Medicare rebate

Estimated out-of-pocket costs

Normal IVF cycle

$9,974

$5,344

$4,484

Frozen embryo transfer (FET)

$3,797

$1,498

$2,259

Ovulation Induction (OI)

$700

$0

$700

Source: IVF Australia. Based on prices from 17 Aug 2018

What inpatient IVF procedures does private insurance cover?

The table below lists the three most common IVF procedures that you could have as an inpatient (usually at your private IVF clinic's day hospital). Private health insurance will pay the amount in the right-most column plus a percentage of any anaesthesia and doctor's fees, per IVF cycle, up to your benefit limit.

Some women have had up to 8+ cycles before falling pregnant, so these contributions from private health insurance can really add up, especially when you combine them with any of the other forms of cover private health offers.

IVF service

Medicare Item Number

Description

Medicare Schedule Fee

Amount covered by Medicare in a private setting

Amount covered by your private insurance

Egg collection

13212

The doctor collects mature eggs during your menstrual cycle, usually when you're sedated.

$365.50

$274.15

$91.35

Transferring embryo to uterus

13215

The doctor places the fertilised egg into your uterus. There is usually no pain or sedation required.

$114.60

$85.95

$28.65

Preparing frozen embryos

13218

For those using fertilised eggs from a previous menstrual cycle, this is the extra prep work needed to get you ready, including thawing the embryo and manipulating your hormones to mimic a menstrual cycle.

$818.35

$613.80

$204.55

Source: MBS Online, 4 June 2021

What are the other types of fertility treatments?

Although it is the most well-known, IVF isn't the only form of fertility treatment available. Here are some of the others.

Intrauterine Insemination (IUI). IUI, sometimes called artificial insemination, is much less invasive than IVF because the fertilisation happens inside your body rather than outside of it. Doctors or nurses collect sperm from your partner or a donor, isolate the strong sperm and then put in your body.

Gamete Intra Fallopian Transfer (GIFT). GIFT is similar to IVF, except that after the eggs are removed and combined with the sperm outside of your body, they are implanted into your fallopian tubes to fertilise inside your body. Reaching the fallopian tubes requires surgery and is becoming less and less common as the success rates of IVF continue to increase.

Zygote Intra Fallopian Transfer (ZIFT). ZIFT is a combination of IVF and GIFT. As with IVF, the eggs are fertilised outside of the body but unlike IVF and more like GIFT, the fertilised egg (sometimes called a zygote) is placed into the fallopian tube via surgery as opposed to the uterus. As with GIFT, ZIFT is becoming less and less common.

Intracytoplasmic Sperm Injection (ICSI). ICSI is a form of IVF that is most commonly used to help overcome male infertility. The difference is that with normal IVF, the egg is combined with hundreds of thousands of sperm and everything is left to fertilise as normal (albeit outside of the body). With ICSI, a single sperm cell is injected with precision into the egg for fertilisation. The fertilised egg is then implanted into the uterus as per normal IVF.

What isn’t covered by Medicare or private health insurance?

Neither Medicare nor private health insurance will cover the following procedures related to IVF:

Ovulation induction. This is where you take medication to encourage egg growth in your ovaries. Not all women will need this.

Freezing and storing embryos or sperm. You only need to have these done if you plan on having IVF at a later date, but want to preserve viable eggs and/or sperm beforehand.

Questions you should ask before choosing an IVF clinic

If you're considering IVF or other fertility treatment, here are are some questions you should ask any potential clinic:

What credentials and training do their staff have?

Are they members of any recognised associations or medical bodies?

What is their overall success rate?

What is their success rate for the procedure you are considering?

What are their clinic and lab hours (can be important if you are working)?

Can they freeze extra embryos for later use?

What does each cycle cost, including drugs?

Do you have to pay up-front or can you pay in instalments?

Are counselling services available?

Do they have patients you can speak with who have completed their program, successfully or otherwise?

FAQs about health insurance for IVF and fertility treatment

Hospital cover assists with inpatient services like egg collection or embryo transfer when performed in a private hospital or day surgery. It also helps with costs for anaesthesia, doctors fees and accommodation. Extras cover on the other hand can help with out-of-hospital expenses for example certain non-Pharmaceutical Benefits Scheme medications or allied health services like counselling.

To claim for IVF treatment you will typically need to submit invoices from your specialists hospital and pharmacy to your private health fund. Ensure you keep detailed records of all your medical appointments, tests and procedures. Many health funds allow you to claim online through their member portal via an app or by mail. It is best to contact your health fund before starting treatment to understand their specific claiming process.

Private health insurance generally only covers a percentage of medications that are not listed on the Pharmaceutical Benefits Scheme (PBS) and are taken as an outpatient under your extras policy. For inpatient hospital services, your hospital cover may contribute to the cost of some IVF related drugs for example anaesthetics. Many IVF medications are expensive and some may not be covered by either Medicare or private health insurance.

While Medicare does not impose specific age limits for IVF rebates, health funds typically do not have an age limit for assisted reproductive services in their Gold tier hospital policies. However individual IVF clinics may have their own age cut-offs for treatment based on success rates and medical advice. It is always best to check with both your chosen health fund and your fertility clinic.

Generally private health insurance does not cover the direct costs associated with purchasing or sourcing donor sperm or donor eggs. Medicare and private health insurance focus on covering the medical procedures involved in assisted reproduction such as the egg retrieval or embryo transfer. Any fees related to donor selection, administration or storage are usually an out-of-pocket expense.

If an IVF cycle is cancelled before certain key procedures have been performed, for example egg retrieval or embryo transfer, the associated medical services for those specific procedures may not be claimable. If a cycle is unsuccessful but completed your private health insurance will still contribute to the eligible hospital inpatient services that were performed during that cycle subject to your policy terms and benefit limits.

You do not need a GP referral to purchase health insurance that covers IVF. However you will need a valid referral from a general practitioner to a fertility specialist or gynaecologist to be eligible for Medicare rebates on your IVF treatment. Without this referral you will not be able to claim a portion of your treatment costs through Medicare.

Private health insurance generally does not cover the costs of preimplantation genetic testing (PGT). PGT includes services like PGT-A for aneuploidy, PGT-M for monogenic or single gene defects and PGT-SR for structural chromosomal rearrangements. These tests are typically considered out-of-hospital diagnostic services and are therefore not covered by hospital insurance. Some limited Medicare rebates may apply to certain aspects of genetic counselling or specific diagnostic tests but the bulk of PGT costs are usually out-of-pocket.

Gary Ross Hunter has over 6 years of expertise writing about insurance, including life, health, home, and car insurance. Having reviewed hundreds of product disclosure statements and published over 800 articles, he loves simplifying complex insurance topics for everyday readers. Gary has contributed to major outlets like Yahoo Finance, The Sydney Morning Herald, and news.com.au, and holds a Bachelor of Arts (Honours) in English Literature from the University of Glasgow, along with a Tier 2 General Advice certification, ensuring his work adheres to ASIC’s RG146 standards.

See full bio

Gary Ross's expertise

Gary Ross

has written

558

Finder guides across topics including:

Make sure your newborn is protected by your health insurance policy.

Important information about this website

Finder is a comparison service. We do not compare every product or every provider in the market.

We make money through commercial arrangements with some of the providers on this site. Products marked 'Sponsored', 'Promoted', 'Featured' or 'Advertisement' appear as a result of a commercial arrangement.

Our editorial content, product reviews and any 'Top Pick' designations are prepared independently of these commercial arrangements.

The default order of products in our tables can be influenced by commercial arrangements. You can re-sort or filter using the controls above each table.

Some content on this site may be generated or supported by AI tools. You should verify details directly with the provider.

Finder is one of Australia's leading comparison websites. We are committed to our readers and stand by our editorial principles.

Our comparison service does not include every product or every provider in the market. Some product issuers offer their products under multiple brands or through associated companies. Where we can, we identify the underlying issuer so you can compare like with like, but you should always check with the provider directly to confirm which brand you are dealing with.

Finder is a comparison website and an intermediary. We are not a product issuer and we do not provide personal financial or credit advice. When you click a link to a product, or apply for a product through our site, you deal directly with the product issuer. We may receive a referral fee, commission or other payment from the issuer if you click through, apply or take out a product. We describe these arrangements in more detail under 'How we make money' below.

Product features, fees, terms and eligibility criteria are set by the product issuer and may change. We rely on information supplied by issuers when we present product details on our site. Before you apply for or take out any product, you should confirm the details directly with the issuer.

We earn revenue from Finder in four principal ways:

Referral fees and commissions. When you click a product link, complete an enquiry form or apply for a product through our site, we may receive a referral fee, commission or other payment from the product issuer. We may also receive payment based on the volume of leads or conversions we send to an issuer.

Sponsored placements. Products marked 'Sponsored', 'Promoted', 'Featured' or 'Advertisement' appear as a result of a commercial arrangement between Finder and the issuer. These labels always indicate a paid placement. We do not use them for editorial choices.

Display advertising. Banner advertising, newsletter advertising and similar display ads on our site are paid by advertisers.

Content sponsorship. Some articles, videos and social media posts are sponsored by an issuer and are clearly labelled as such.

Our editorial opinions, product reviews and any 'Top Pick' designations are prepared independently of these commercial arrangements. A 'Top Pick' is an editorial choice made by our writers and editors based on the criteria described on each comparison page. A 'Top Pick' is not a personal recommendation and does not mean the product is appropriate for your circumstances.

If you would like to know whether we have a commercial arrangement with a specific product issuer, please contact us.

When products are grouped in a table or list, the default order can be influenced by commercial arrangements we have with product issuers. In some categories, sponsored or featured products appear in the top positions of the table by default, and are always labelled as such.

Other factors that influence default order include price, fees and features, and (where relevant) our editorial view of the product.

You can re-sort every comparison table using the controls above the table. You can filter by product features that matter to you. The order you see after re-sorting or filtering is not influenced by commercial arrangements.

Some content on this site is generated or supported by artificial intelligence tools, including our AI-powered assistant FinderBot. AI-generated content may contain errors. Please verify important information directly with the product issuer before making a financial decision. For more information about FinderBot, see the FinderBot Terms of Use and FinderBot Privacy Collection Notice.

Please read our website terms of use and privacy policy for more information about our services and our approach to privacy.

We update our data regularly, but information can change between updates. Confirm details with the provider you're interested in before making a decision.

Our goal is to create the best possible product, and your thoughts, ideas and suggestions play a major role in helping us identify opportunities to improve.