Also known as critical illness insurance, trauma insurance provides a lump-sum payment if you suffer a serious medical condition.

How do trauma insurance policies work?

Trauma insurance covers for you serious illnesses, accidents or medical conditions. If you take out a policy and then develop an illness or condition that's covered under the policy you will receive a one-off payment that can be used to cover your medical costs, large debts such as a mortgage, and the cost of home modifications and professional care.

When am I eligible for a trauma payment?

To be eligible for a trauma insurance payout, your illness or injury must be one that is covered by your policy and while such conditions vary with insurers, the most common are cancer, heart attack, coronary bypass and stroke. The condition must also occur after what's known as the exclusion period.

{"userFilters":[{"config":{"MULTISELECT":true,"VALUES":"TPD cover,Trauma cover,Children's Insurance,No optional"},"dataSelector":{"recordType":"product","fieldCode":"FILTERS.OPTIONAL_ADD_ONS"},"dataType":"TEXT","label":"Optional Extras","order":1},{"config":{"VALUES":"Yes,No"},"dataSelector":{"recordType":"product","fieldCode":"FEATURES.FULLY_UNDERWRITTEN"},"dataType":"TEXT","label":"Fully Underwritten","order":2},{"config":{},"dataSelector":{"recordType":"product","fieldCode":"FILTERS.TERMINAL_ILLNESS_BENEFIT_2"},"dataType":"MONEY","label":"Cover Amount","order":3},{"config":{},"dataSelector":{"recordType":"product","fieldCode":"FILTERS.TERMINAL_ILLNESS_BENEFIT"},"dataType":"MONEY","label":"Terminal Illness Benefit","order":4},{"config":{},"dataSelector":{"recordType":"product","fieldCode":"FEATURES.FUNERAL_BENEFIT"},"dataType":"MONEY","label":"Funeral Benefit","order":5},{"config":{},"dataSelector":{"recordType":"product","fieldCode":"FILTERS.MAX_ENTRY_AGE"},"dataType":"NUMBER","label":"Maximum Entry Age","order":6},{"config":{"MULTISELECT":true,"VALUES":"Child cover,Interim accident cover,Counselling benefit,Guaranteed renewability,Increase cover without a medical,Premium suspension "},"dataSelector":{"recordType":"product","fieldCode":"FILTERS.INCLUDED_BENEFITS"},"dataType":"TEXT","label":"Benefits","order":7},{"dataSelector":{"recordType":"UI_FILTER_COMPONENT","fieldCode":"SPECIAL_OFFERS"},"dataType":"BOOLEAN","label":"Special offers","componentType":"SpecialOffersFilter","config":{"VALUES":"1","fields":[{"value":"rewards_exclusive","label":"Finder Rewards & exclusives"},{"value":"all_offers","label":"All offers"}]},"options":{"comparator":"eq"},"queryParameter":"special-offers"},{"config":{},"dataSelector":{"recordType":"product","fieldCode":"GENERAL.PROVIDER_ID"},"dataType":"UUID","label":"Providers","order":8},{"config":{"VALUES":"Apply directly online,Underwritten via a broker"},"dataSelector":{"recordType":"product","fieldCode":"FEATURES.POLICY_TYPE"},"dataType":"TEXT","label":"Product Type ","order":null},{"config":{"VALUES":"0"},"dataSelector":{"recordType":"UI_FILTER_COMPONENT","fieldCode":"FULL_MARKET"},"dataType":"FULL_MARKET","label":"More products","queryParameter":"full-market"}],"niche":{"currencySymbol":"$","decimalPoint":".","decimalPlaces":"2","thousandsSeparator":",","filterBoundsMap":{"product.FILTERS.OPTIONAL_ADD_ONS":null,"product.FEATURES.FULLY_UNDERWRITTEN":null,"product.FILTERS.TERMINAL_ILLNESS_BENEFIT_2":{"minimum":"100000","maximum":"25000000"},"product.FILTERS.TERMINAL_ILLNESS_BENEFIT":{"minimum":"100000","maximum":"25000000"},"product.FEATURES.FUNERAL_BENEFIT":{"minimum":"0","maximum":"30000"},"product.FILTERS.MAX_ENTRY_AGE":{"minimum":"10","maximum":"79"},"product.FILTERS.INCLUDED_BENEFITS":null,"product.GENERAL.PROVIDER_ID":null,"product.FEATURES.POLICY_TYPE":null}},"prefilled":false,"experimental":false}

6 of 18 results

Compare other products

We currently don't have that product, but here are others to consider:

Looking for other options? Check out these similar products.

How we picked these

Why compare life insurance with Finder?

You pay the same price as buying directly from the life insurer.

We're not owned by an insurer (unlike other comparison sites).

We've done 100+ hours of policy research to help you understand what you're comparing.

Speak to an insurance specialist to help you find personalised cover

Should I buy a standalone trauma policy or bundle it with life insurance?

Trauma insurance can be purchased as a standalone product or as part of a plan, often bundled with life insurance and TPD insurance. There are advantages and disadvantages to both options.

Bundled trauma insurance

Cheaper (save on fees and stamp duty)

Less comprehensive cover

Standalone trauma insurance

More comprehensive cover

Generally more expensive

If your bundled trauma insurance policy doesn't provide sufficient cover you might need to consider additional cover options such as Buy Back and Double Trauma benefit to ensure you have adequate trauma protection.

Do all trauma insurance policies cover the same conditions?

Most claims for a critical illness or injury are for either heart attacks, strokes or cancer, but there are others that may vary between insurers. This is why it's essential you compare your cover, or speak to an adviser about a policy suitable to your needs.

You have two types of policies to choose between when signing up for trauma insurance: a standard policy or comprehensive policy. Most insurers cover the same medical conditions but there is a chance it will vary due to different definitions.

Conditions that are covered

Here's a list of what is usually offered under standard and comprehensive policies.

Standard policy

Comprehensive policy

The cheapest type of policy. It typically covers between 30–44 critical conditions, including the following.

Cancer

Heart attack

Stroke

Brain damage

Down's Syndrome

Time in intensive care

Offers similar cover to a standard policy, but also provides cover for another 15 conditions. Here are some of them.

Melanoma

Diabetes complications

Partial blindness

Partial loss of hearing

Carcinoma

Osteoporosis

One step you can take to find out what medical conditions are covered by your policy is reading your Product Disclosure Statement (PDS). This is the outline of your contract, and includes all included costs, benefits and exclusions. All insurers provide a PDS when you sign up for a policy.

The video guide to trauma insurance

1:52

What happens if I'm diagnosed with serious illness happens?

You will need to make a claim. Here's an outline of the process:

To make a trauma insurance claim you'll generally need to follow this process.

Fill out a claim form.This is completed by you, your doctor and any medical specialists involved. Your treating doctor will need to provide details of your condition and medical history.

Provide identification. This could include an Australian passport, birth certificate and a driver licenses.

Provide your original policy documentation. You'll need to show the original policy you were given or quote the policy number.

Provide any further documents. This might include additional medical reports or investigations.

Will I be paid straight away? No. Your condition will need to be assessed to see if it meets your insurers definition and you'll also need to pass the 'survival period' set out by your insurer.

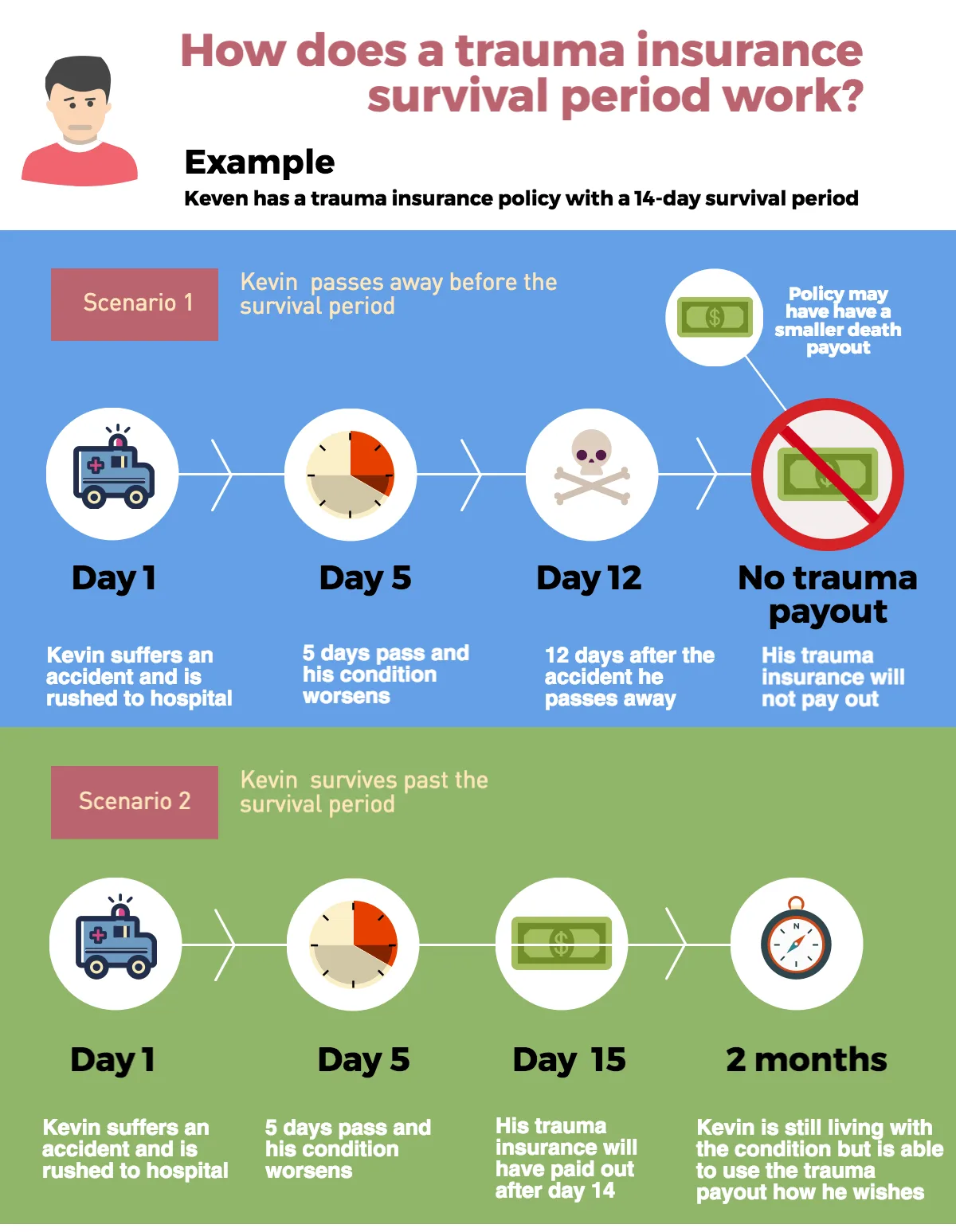

Understanding trauma insurance survival periods

The survival period is the amount of time a policyholder must survive before passing away, in order to receive a trauma insurance payment. Imagine, for example, a trauma insurance policy with a 14-day survival period. If the policyholder suffers serious trauma, is taken to hospital, and dies 12 days later the insurer will not pay out the policy. But if the policyholder passes away after the 14-day survival period (as a result of their injuries or illness) the insurer will grant the payout.

*This diagram is purely for illustrative purposes and is not indicative of all cases and policies.

What is the 90 day exclusion period?

Most policies also feature a 90-day exclusion period. This is standard to make sure you don't just take out trauma cover to make a claim for a condition you know you already have.

Under this exclusion, claims for many insured events will not be paid if the condition occurs or is diagnosed within 90 days of:

The start of your policy

The date of an applied-for increase in cover (but only in respect of the increase)

The most recent date your policy was reinstated

Is trauma insurance worth it?

Great, trauma insurance is important. But is it worth your money? What if you already have life insurance in place? Consider the following.

It covers you where other forms of insurance won't

Trauma insurance can offer cover in areas where life insurance, income protection and disability insurance fall short:

Unlike life insurance. Trauma insurance pays out if you survive a critical condition (as opposed to when you die).

Unlike disability insurance and income protection. Trauma insurance will pay out on diagnosis (as opposed to after you prove you are unable to work).

Five ways trauma cover can help out during a tough time

Trauma Insurance (also known as critical illness cover) provides you with a lump sum payment if you suffer a serious medical condition such as a heart attack. A trauma benefit can be used to:

Remaining medical bills, including out-of-pocket expenses.

Rehab, if not already covered by health insurance

A live-in nurse if you need it

A holiday to take your mind off things

Let you take time off work

Trauma insurance can either be bought by itself or in conjunction with death cover (life insurance), cover for your salary (income protection) and disability insurance (TPD).

Trauma insurance offers a lump-sum payment (that in many cases is up to $2 million) if you develop a serious illness or injury. Here are some real-life examples of how critical illness cover is used:

The cost of surviving a critical condition such as a heart attack can be ongoing and is not typically covered by health insurance. You can use your benefit payment to alleviate any financial stress brought about by additional medical expenses, such as rehabilitation, carers and changes to the home.

3. Take a holiday with your family

After being diagnosed, you'll probably want to spend as much time with your family as possible. Trauma insurance lets you spend quality time with your family without having to worry about the costs.

If the illness is untreatable or the chances of survival are slim, you can use the money to fund family holidays and dream experiences. While it may seem inconsequential, the holidays could let the family spend time together and create some memories. It also allows the family member suffering from the critical illness to enjoy a quality life during their final months.

4. Take time off from work without any worry

When you have a critical illness, there is a good chance you will need to take some time off work or even stop working altogether to get extra care. Trauma insurance will allow you to get the assistance you need while you are receiving treatment. Both you and your spouse can take some time off from work without having to worry about having enough money.

5. Achieve your financial goals

When tragedy strikes, you may not be able to generate the same income you were making before since you may no longer be able to work or your spouse may work less to take care of you. You can use your trauma insurance to pay off the following financial commitments:

You can pay for someone to take your place if you are the proprietor of your own small business.

You can pay out any credit card or other debts to give you more cash flow.

You can pay off your mortgage so that you know that no matter what happens in the future, your family will always have a roof over their heads.

The cost of trauma insurance vs the financial impact of major illness

Monthly cost of trauma insurance

As little as $22.53

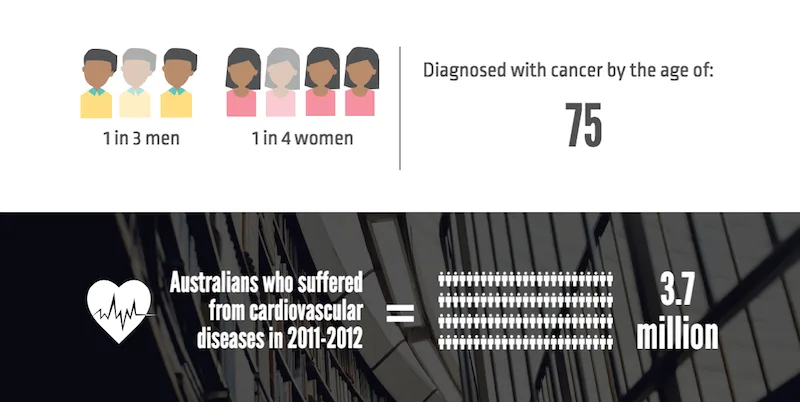

Australians at risk of chronic disease

Over 50%

Average financial impact of a stroke

$100,000

Average financial impact of a heart attack

$281,000

Cost of trauma insurance

Prices taken from finder's quoting engine for a 35 year old male who was looking for $100,000 in cover.. Data last checked October 2017

Risk of chronic disease

Taken from the Australian Institute of Health and Welfare's Australia's health 2016. Chronic diseases taken into account are:

Asthma

Back pain and problems

Cancer (such as lung and colorectal cancer)

Cardiovascular disease (such as coronary heart disease and stroke)

Chronic obstructive pulmonary disease (COPD)

Diabetes

Mental health conditions (such as depression).

Arthritis

Financial impact of a stroke and heart attack

These figures were taken from Access Economics. The economic impact of stroke in Australia. Canberra: Access Economics, 2013. and The economic costs of heart attack and chest pain (Acute Coronary Syndrome). Canberra: Access Economics, 2009.

Costs include: Direct health costs, loss of productivity, cost of care, transport, welfare costs, etc.

Australians are prone to serious illnesses

How do I compare trauma insurance quotes?

Trawling for the best trauma insurance quote can be a time-consuming exercise, but it's critical to do your homework to find the best policy to meet your medical and budget needs.

There are a number of factors to think about before you sign on to a policy. Here's a guide on what sort of questions you should weigh up.

What are your included benefits?

It's important to compare what medical conditions are covered by insurance companies. Not all funds offer the same benefits for certain illness or injuries under trauma insurance, so you need to understand what is included, and if there are additional options that could enhance your cover.

Here are some built-in benefits to look for when comparing policies:

Feature

What's covered?

Funeral Advancement Benefit

Pays a lump sum to cover funeral costs.

Terminal Illness Benefit

Lump sum in the advent of a terminal illness diagnosis.

Future Insurability benefit

You can increase your cover without medical evidence.

Waiver of Life Premium

Pay no premiums if you become totally disabled.

Interim Cover

Provides interim cover for an accident while your claim is processed.

Premium Freeze

You can freeze premiums at the previous year's amount, so it doesn't increase with your age.

Accommodation Benefit

Pays a benefit if you are bedridden, over 100km from your home and need a family member on hand.

Financial Planning Reimbursement

Reimburses costs of financial planning advice when you're paid a benefit under life insurance.

Benefit Reimbursement

An option to lift your cover each year in line with the CPI or another agreed percentage.

Suspension Cover Benefit

Here you can suspend your cover temporarily for 12 months due to financial trouble.

What are the optional benefits of the policy?

Insurers may offer you other optional benefits to give you more comprehensive cover at an additional cost. There is a wide range of extras insurers offer, but the following are the most common.

Optional benefit

What's covered?

Accidental Death Benefit

A benefit is paid to your family if you die from an accident.

Business Future Insurability

Here you can increase your business cover due to an event, and without added medical documentation.

Needlestick Cover

This benefit aims to compensate medical professionals if they suffer a needlestick injury on the job.

It's essential that you're clear on the benefits included in your policy, and any extras that could enhance your cover. By doing this, you'll have peace of mind that the policy is right for you and your family.

Your premium is the annual payment for a trauma insurance policy. It's made up of three elements: your base fee, policy fee, and sometimes stamp duty may be applied. Though stamp duty isn't normally linked to life insurance, it can be applied to other policies like income protection.

You have the choice of three options to help control the cost of your premium:

Stepped premium. This is the cheapest option initially, but your cost increases as you age.

Level premium. More expensive at the beginning of your policy, but your premium won't increase as you get older.

Hybrid premium. A combination of stepped and level premiums. It starts out as a stepped premium but after a certain length of time, it changes to a level premium.

Another point to consider is whether you want a stand-alone or combined trauma insurance policy to help control the cost of your cover.

Combined trauma cover

This provides the same amount of cover as stand-alone policies. The advantage is you can link policies together under one premium, but any claim made will impact your benefits by the same amount in all bundled policies.

You can link your trauma insurance with your life insurance and TPD insurance, but income protection policies are normally only offered as stand-alone cover.

There are a number of personal factors that will impact the cost of your policy. Here's a list showing what insurers look at.

Your age. Life insurers use a mortality table to assess your age. So the older you are, the higher the premium you'll pay.

Do you smoke? Smoking will be taken into account when starting a trauma insurance policy, as there is an increased risk of suffering from conditions like lung cancer.

Do you suffer a medical condition? You must be honest about any medical condition you might be suffering, and one that could lead to a critical illness. If you are dishonest the company can reject any future claims.

Lifestyle choices. Generally, pastimes and chosen activities are covered, although extreme sports like sky diving may be excluded.

Gender. You're gender can impact your premium depending on your age. For instance in your 30's women are at greater risk of having

Occupation (conditional). It's unusual for your employment to impact your policy, but some insurers take this into account. This could include working a dangerous job.

How much trauma insurance do I need?

You never know what curve balls life will throw your way, so it can be hard to calculate the amount of critical illness cover you'll need. There are many unforeseen treatment and rehabilitation costs that follow a trauma or critical illness, so you need to understand how becoming a sufferer will impact your individual circumstance or family situation.

Think about your individual circumstance and family

There are personal and family factors you should consider when assessing how much trauma insurance you need. Here are some points to factor in.

Affordability and income. Your policy depends on what you can afford. Weigh up how much you earn against your debts.

Entitlements. You may also have other government schemed benefits like sick leave and workers' compensation that could fill some gaps with your policy.

Your partner and other dependents. Your spouse or partner is the individual likely to be your carer, so take into account lost income on their behalf when deciding on the cover you need. It's also important to think about future finances for your children like university fees.

Should I link any other policies? It could be a good option to link a salary continuance policy with your trauma insurance to provide up to 75% of your monthly income in the advent of a critical illness or injury.

Consider the levels of cover available

You have a choice between two types of trauma insurance policies to ensure you're covered for the costs linked to one or more conditions. This is achieved through a standard or comprehensive policy.

Standard policy. The more affordable option. It takes into account 30–44 critical illnesses like heart attack, stroke and cancer.

Comprehensive policy. More expensive but comprehensive. It covers the same conditions as a standard policy, and also around 15 other conditions like melanoma, diabetes complications and brain damage.

Must read: The costs of serious illnesses

Statistics show that suffering a trauma can amount to tens of thousands of dollars in someone's lifetime. A study conducted by Access Economics in 2009 revealed some staggering results.

Having a heart attack

In 2009, heart attacks in Australia cost around AUD$15.5 billion.

In 2003, the average cost to a sufferer was estimated to be around AUD$18,000 a year, and AUD$44,000 during their life.

Suffering a stroke

In 2012, strokes totalled AUD$5 billion, with costs spent on productivity, medical treatment and carers.

In that same year it was estimated stroke sufferers will spend around AUD$57,000 in medical and rehabilitation expenses during their life.

Cost of cancer

In 2011, Cancer cost the community AUD$3.8 billion, while in 2006 a family's financial cost was AUD$47,000 a year.

It's estimated a male smoker suffering lung cancer could see costs of AUD$200,000 for his medical treatment and rehabilitation.

Cost of diabetes in Australia

Around 1.7 million Australians suffer from diabetes, and around 280 others develop the disease every day.

Diabetes costs the community around AUD $14.6 billion a year.

Do I need a comprehensive policy?

There are some alarming statistics surrounding the likelihood of suffering conditions covered in a comprehensive policy. Australians live an outdoor lifestyle, and the increased exposure to the sun could mean you're more at risk of skin conditions like melanoma.

Here are some statistics compiled by Cancer Australia.

In 2012, it was estimated that there were 12,036 cases of the skin disease.

In 2013, there were more than a thousand deaths related to melanoma.

In 2016, the number of sufferers is estimated to be around 13,283 people.

There's a higher risk of contracting melanoma as you age.

Severe diabetes is covered in both types of policies, but a complication is normally only covered in a comprehensive policy. The disease poses a huge challenge to Australia's healthcare system. Costs to the community and sufferers are huge, and the likelihood of contracting the condition is on the rise.

The Australian Securities & Investments Commission (ASIC) offers the following advice to consumers purchasing or comparing trauma insurance

Look for restrictions that might limit your cover such as those related to age, maternity leave, casual or part-time work and dangerous occupations.

Make sure the policy is fully indexed so that benefits and premiums keep up with inflation.

Be sure to answer all questions honestly in your application and declare any pre-existing medical conditions, to avoid having your claim rejected in the event of a trauma.

Discuss trauma insurance with your partner and consider covering them as well, as a trauma suffered by either of you would have the same impact on your lifestyle and income.

Know how much cover you will need by considering your financial assets and obligations both now and in the future.

Before purchasing a policy, read the Product Disclosure Statement (PDS) carefully so that you fully understand what is covered and what it will cost you.

What are the most common types of Trauma Insurance claims?

According to Experien Insurance Services, by far the most common Trauma Insurance claim is for cancer (74%), followed by heart conditions (17%), stroke (5%), Parkinson's Disease (2%) and Multiple Sclerosis (2%).

Other conditions often covered by a Trauma Insurance policy include Alzheimer's disease, blindness, loss of speech, paralysis, chronic kidney failure, liver disease, lung disease, dementia, head trauma and major organ transplants.

Conditions where Trauma Insurance will only pay a partial benefit include benign tumours, osteoporosis, the loss of a single limb or eye, burns to less than 20% of the body and partial deafness or hearing loss in one ear.

Do I really need trauma cover if I have health insurance?

Your Medicare and private health insurance can help pay for your hospital bills and medical expenses. However, your health insurance will not cover any loss of income, especially when you are unable to work for an extended period of time.

It also will not cover any expenses incurred that are outside the capacity of your health cover, such as rehabilitation, equipment, vehicle or home modification and nursing care costs, leaving you to pay these expenses out of your own pocket. Trauma insurance is an additional layer of cover on top of your health insurance in the event that you suffer from a more serious medical condition.

It will give you an extra financial buffer for any ongoing commitments that are not covered under your health insurance. You can read finder's full guide on the differences between trauma and health cover for a wider understanding.

I have some more questions about trauma insurance

Trauma insurance is an insurance product that is becoming more attractive among Australians especially to those who want to secure their future and get protection coverage against serious illnesses. This type of insurance provides you the peace of mind of having a financial backup in case you become injured or diagnosed with an illness that is covered by your policy. With this financial backup, you get better security from the financial pressure caused by your condition. This can help you concentrate on your recovery with less burden to you and your family. The policy holder can claim a lump sum amount once eligible to make a claim.

The good thing about this insurance is the fact that it gives you financial freedom in facing a major medical crisis. Unlike other types of life insurance where claims can only be made upon the death of the insured member, trauma insurance benefits are paid while the insured member is still alive. The amount of money received from the proceeds of your claim can be used not only to finance your medication but to cover you for other expenses and can substitute your income while on your way to recovery.

Unlike income protection, anyone can take out trauma cover even if they do not belong to the workforce. This is more recommended to homemakers and those not engaged in a regular employment. They can apply for trauma insurance and enjoy the protection and benefits from their insurance claims which they can use to pay off debts, seek for medical cure, pay for their medical expenses and meet other financial obligations while recuperating from their condition. Trauma insurance can give you coverage in around 40 kinds of illnesses as specified by the insurers. The legal claim from your benefit will be based on the specific illnesses covered by your insurance policy. It is therefore best to assess your risk factors and choose a trauma insurance that covers the medical conditions you may likely develop in the future.

What's the difference between trauma insurance and life insurance, etc?

Trauma insurance is usually part of a package with life insurance. Life insurance covers death but gives you the option to cover additional life events e.g. trauma cover.

Details

Trauma Cover

Life Insurance

What's covered

Trauma insurance is essentially "living insurance". This means you are provided financial assistance in the event you are diagnosed with a life-threatening disease.

Life insurance is a form of death cover. This provides your family with financial assistance if you die during the term of the policy.

Is it available through super?

No

Yes

Form of payment

Lump sum

Lump sum

'Living insurance'

Trauma insurance falls under the "living" category of life insurance where the policy holder can use his insurance benefit while he is still alive to finance his medical costs.

While it gives financial benefits to the insured, the trauma insurance also eases the emotional and psychological burden that your condition brings to your family. Because the insurance benefit can be claimed the moment you are diagnosed with a serious illness covered by your policy, you can be assured of getting the peace of mind that your condition will not cause too much of a financial burden to your family.

Trauma insurance pays you out on the diagnosis of a condition (if covered by your policy). Total and permanent disability insurance on the other hand, pays out when you meet the insurers definition of a disability.

Details

Trauma Insurance

TPD Insurance

Situations covered

You are diagnosed with a serious illness such as cancer.

You are unable to work due to illness or injury.

Condition of payout

You'll need to survive a traumatic event as defined by the policy.

You'll need to prove your inability to ever return to work.

Is it available through super?

No (not anymore)

Yes

Form of payment

Lump sum

Lump sum

Income protection is primarily designed to replace some of your income if an injury or illness forces you out of work. Trauma insurance on the other hand provides lump sum for injuries or illnesses that are specified on the policy and not related to whether or not your put out of work.

Details

Trauma Insurance

Income Protection

Situations covered

You are diagnosed with a serious illness such as cancer.

You are unable to work due to illness or injury.

How can you use the benefit?

It helps you pay for immediate and ongoing medical costs as well as changes to your life style.

It provides you with a portion of your regular income to help you maintain your standard of living while you are unable to work.

Is it available through super

No

Yes

Form of payment

Lump-sum payment

Regular payments (income protection)

*The number of conditions covered will vary policy to policy. Always check the product disclosure statement to review what is and isn't covered.

Richard Laycock is Finder’s insights editor after spending the last five years writing and editing articles about insurance. His musings can be found across the web including on MoneyMag, Yahoo Finance and Travel Weekly. Richard studied Media at Macquarie University and The Missouri School of Journalism and has a Tier 1 Certification in General Advice for Life Insurance.

See full bio

Review the Australian Seniors Life and compare options available.

Important information about this website

Finder is a comparison service. We do not compare every product or every provider in the market.

We make money through commercial arrangements with some of the providers on this site. Products marked 'Sponsored', 'Promoted', 'Featured' or 'Advertisement' appear as a result of a commercial arrangement.

Our editorial content, product reviews and any 'Top Pick' designations are prepared independently of these commercial arrangements.

The default order of products in our tables can be influenced by commercial arrangements. You can re-sort or filter using the controls above each table.

Some content on this site may be generated or supported by AI tools. You should verify details directly with the provider.

Finder is one of Australia's leading comparison websites. We are committed to our readers and stand by our editorial principles.

Our comparison service does not include every product or every provider in the market. Some product issuers offer their products under multiple brands or through associated companies. Where we can, we identify the underlying issuer so you can compare like with like, but you should always check with the provider directly to confirm which brand you are dealing with.

Finder is a comparison website and an intermediary. We are not a product issuer and we do not provide personal financial or credit advice. When you click a link to a product, or apply for a product through our site, you deal directly with the product issuer. We may receive a referral fee, commission or other payment from the issuer if you click through, apply or take out a product. We describe these arrangements in more detail under 'How we make money' below.

Product features, fees, terms and eligibility criteria are set by the product issuer and may change. We rely on information supplied by issuers when we present product details on our site. Before you apply for or take out any product, you should confirm the details directly with the issuer.

We earn revenue from Finder in four principal ways:

Referral fees and commissions. When you click a product link, complete an enquiry form or apply for a product through our site, we may receive a referral fee, commission or other payment from the product issuer. We may also receive payment based on the volume of leads or conversions we send to an issuer.

Sponsored placements. Products marked 'Sponsored', 'Promoted', 'Featured' or 'Advertisement' appear as a result of a commercial arrangement between Finder and the issuer. These labels always indicate a paid placement. We do not use them for editorial choices.

Display advertising. Banner advertising, newsletter advertising and similar display ads on our site are paid by advertisers.

Content sponsorship. Some articles, videos and social media posts are sponsored by an issuer and are clearly labelled as such.

Our editorial opinions, product reviews and any 'Top Pick' designations are prepared independently of these commercial arrangements. A 'Top Pick' is an editorial choice made by our writers and editors based on the criteria described on each comparison page. A 'Top Pick' is not a personal recommendation and does not mean the product is appropriate for your circumstances.

If you would like to know whether we have a commercial arrangement with a specific product issuer, please contact us.

When products are grouped in a table or list, the default order can be influenced by commercial arrangements we have with product issuers. In some categories, sponsored or featured products appear in the top positions of the table by default, and are always labelled as such.

Other factors that influence default order include price, fees and features, and (where relevant) our editorial view of the product.

You can re-sort every comparison table using the controls above the table. You can filter by product features that matter to you. The order you see after re-sorting or filtering is not influenced by commercial arrangements.

Some content on this site is generated or supported by artificial intelligence tools, including our AI-powered assistant FinderBot. AI-generated content may contain errors. Please verify important information directly with the product issuer before making a financial decision. For more information about FinderBot, see the FinderBot Terms of Use and FinderBot Privacy Collection Notice.

Please read our website terms of use and privacy policy for more information about our services and our approach to privacy.

We update our data regularly, but information can change between updates. Confirm details with the provider you're interested in before making a decision.

Our goal is to create the best possible product, and your thoughts, ideas and suggestions play a major role in helping us identify opportunities to improve.