Retirement statistics for 2023

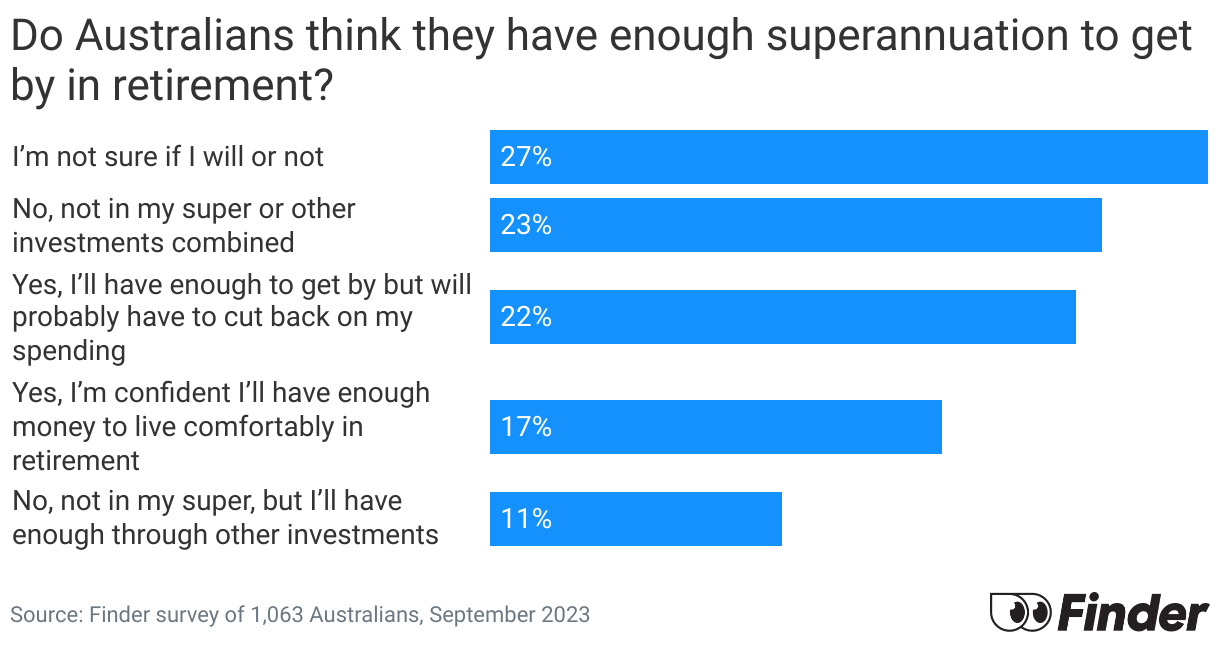

27% of Australians are not sure if they have enough to retire.

Planning for retirement might lack the thrill of saving for a new car or a dream holiday, but it's key to a relaxed future. Just as you diligently save for big purchases, it's equally vital to nurture your super for retirement.

As of December 2023, Australians ideally need around $641,223 for a comfortable retirement, but there's a gap in actual savings.

As 2023 came to an end, refining your super strategy was crucial amid rising living costs and evolving retirement goals. Starting early, contributing wisely and choosing the right investments are all part of reaching that essential retirement target.

Aussies have a real mixed bag of feelings about retirement. Some are confident they've got it all sorted with their super, while others are crossing their fingers and hoping for the best.

Finder surveyed 1,000+ Australians and asked them questions regarding retirement and their superannuation. The answers might just surprise you.

A lot of folks are asking themselves this. Some are pretty sure they'll scrape by, others are more upbeat about living comfortably. But there's definitely a chunk of people feeling a bit uneasy about whether their super's going to cut it.

27% of respondents are uncertain if they'll have enough superannuation for retirement. Nearly a quarter (23%) believe they won't have enough, either through superannuation or other investments.

22% think they'll manage but may need to cut back on spending, while 17% are confident they'll be comfortable financially in retirement.

A smaller segment (11%) anticipates relying on investments other than superannuation.

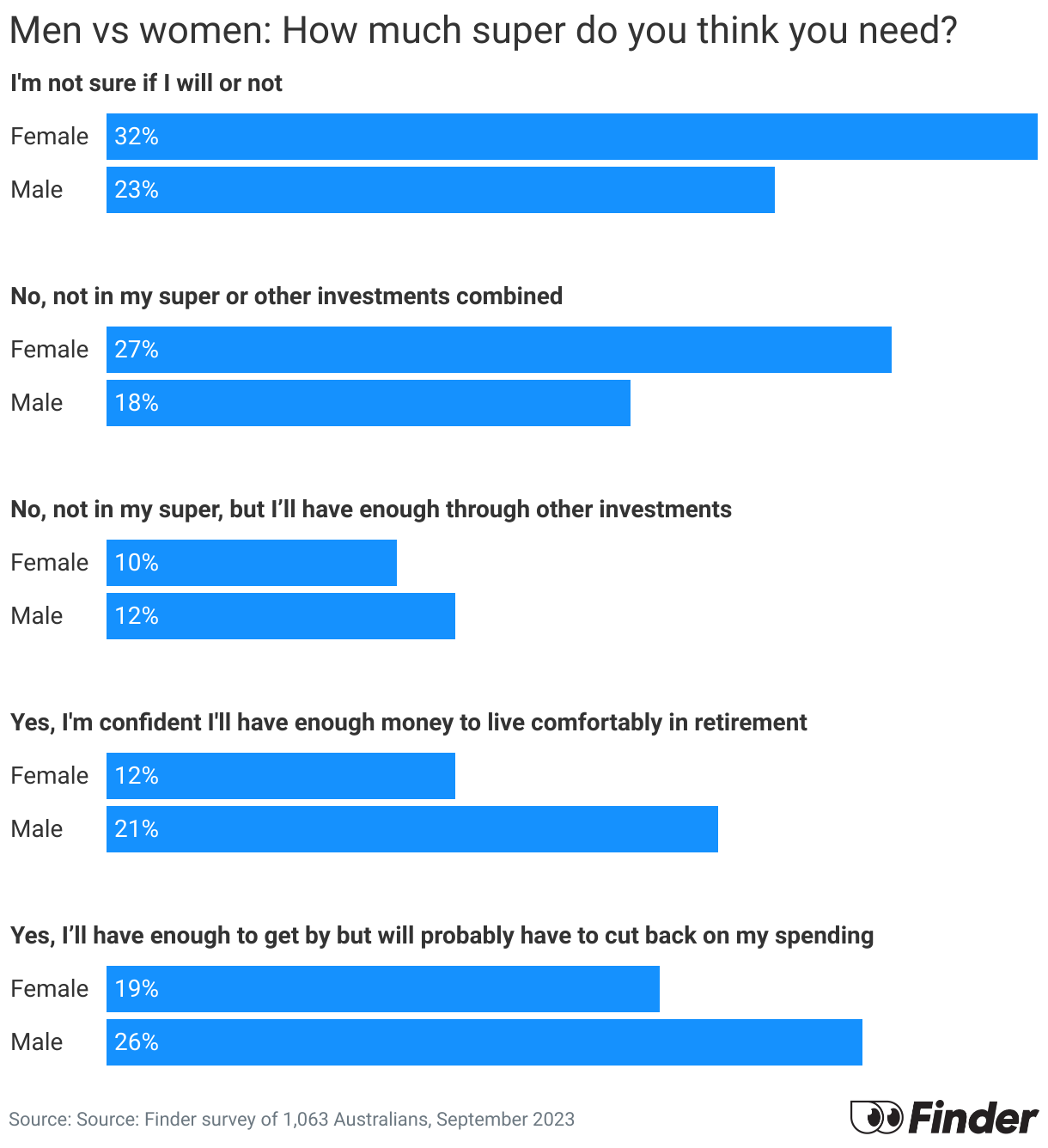

Aussie men and women have different levels of confidence in their super. We're seeing some interesting numbers showing how each gender views their retirement readiness.

Out of 1,063 Australians, 32% of women and 23% of men were unsure if they'd have enough superannuation for retirement.

27% of women and 18% of men doubted their superannuation and other investments would be enough, while 10% of women and 12% of men expected sufficient funds from other investments.

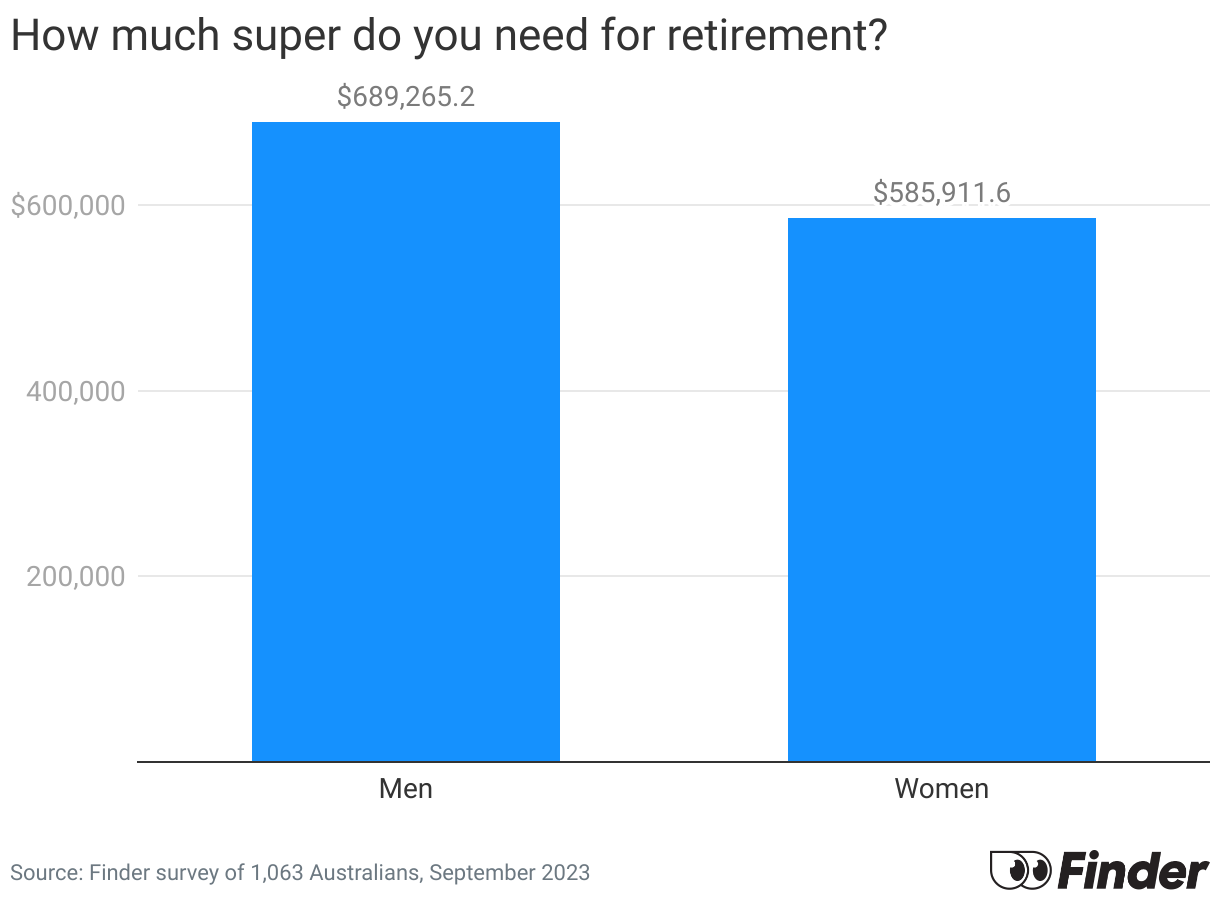

Australian men require an average of $689,265 for retirement, while the average requirement for women is $585,911.

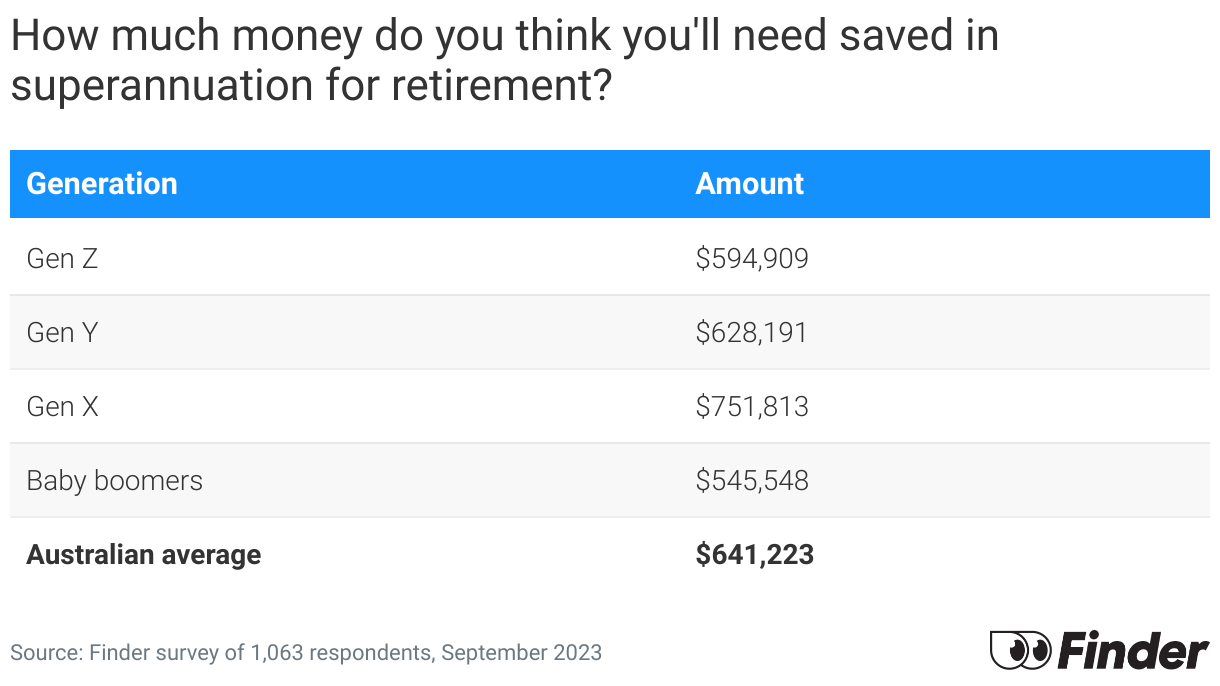

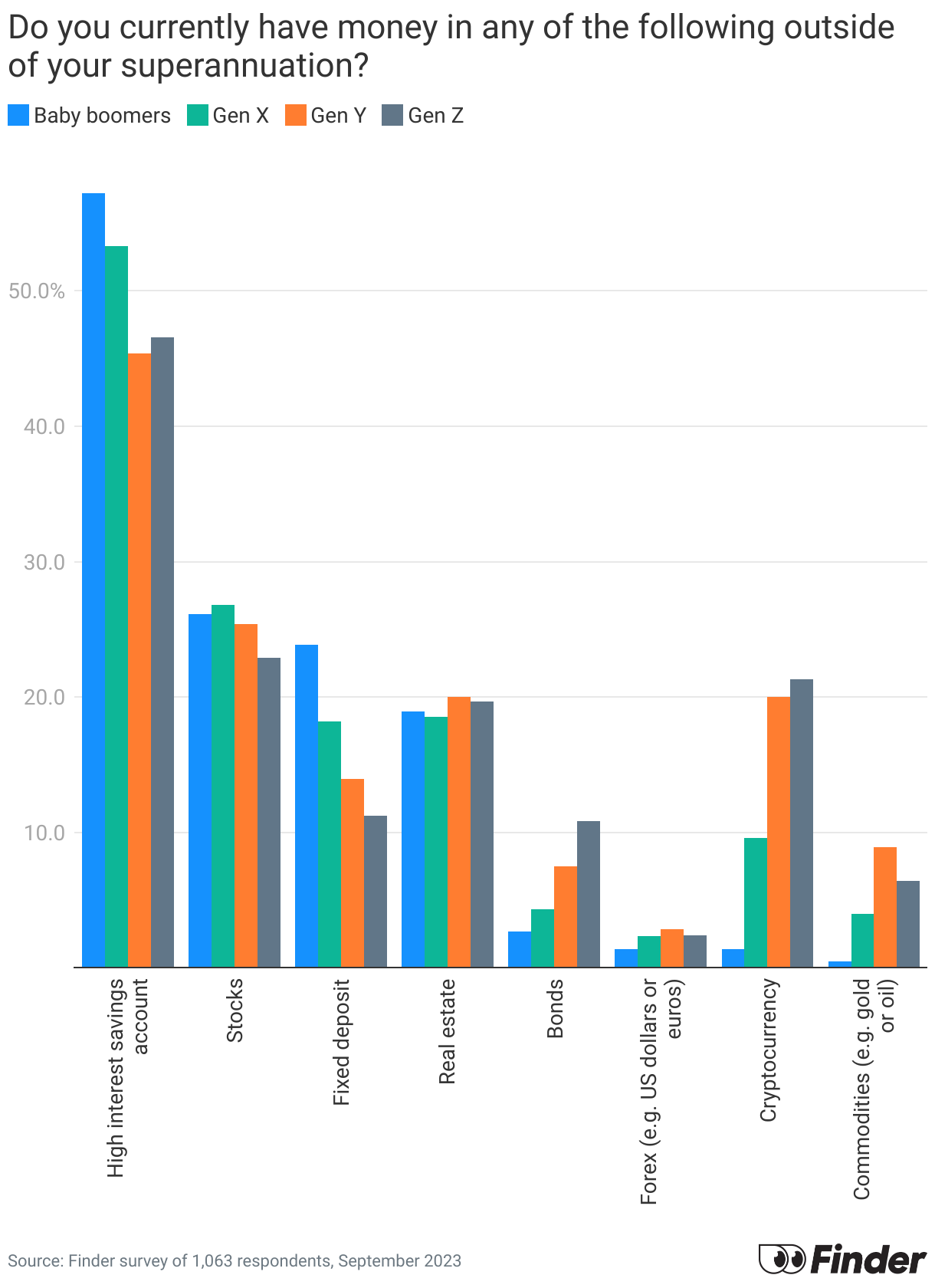

Every generation faces unique challenges and opportunities when saving for retirement. We'll compare the super needs of baby boomers, gen X, millennials and gen Z, highlighting how retirement planning differs across ages.

Survey data show varied sentiments across generations regarding superannuation sufficiency.

On average, estimated super needs ranged from $545,548 for baby boomers to $751,813 for gen X, with an Australian average of $641,223.

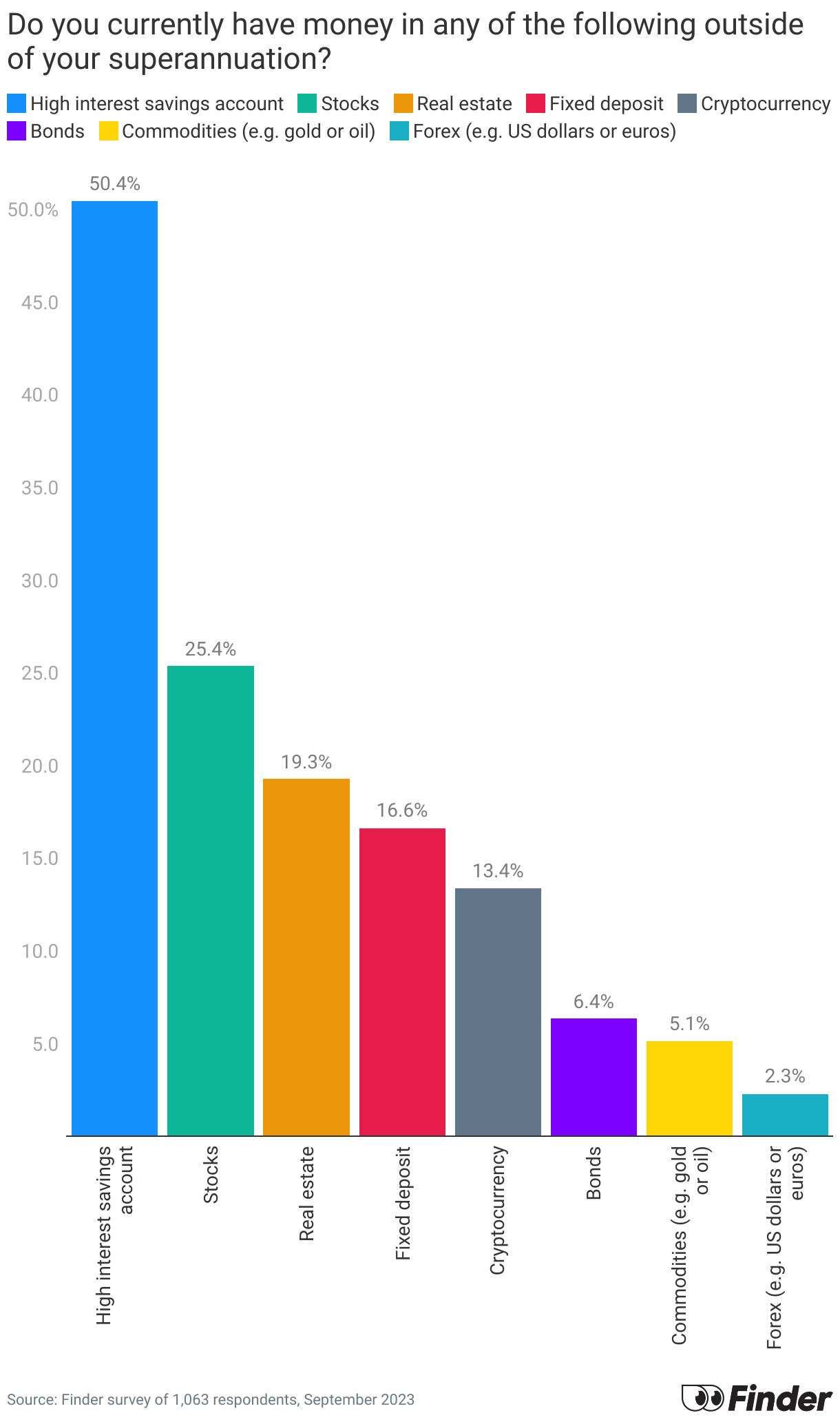

Diversifying investments is key to financial security. We'll check out what kinds of investments Aussies are making outside their super – from real estate to stocks and bonds.

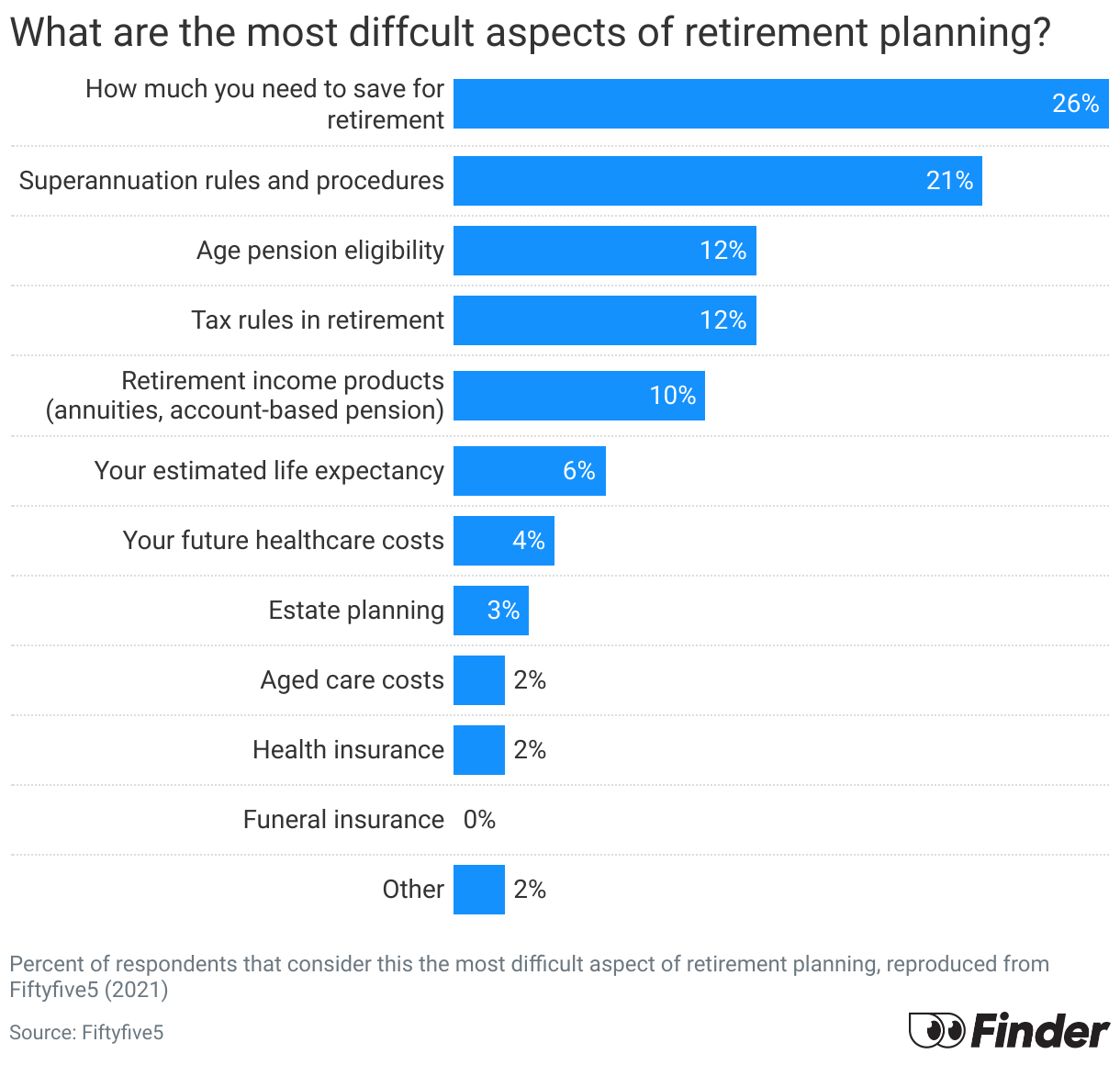

The most challenging aspects of retirement planning include figuring out how much to save (26%), understanding superannuation rules (21%) and determining age pension eligibility (12%).

Tax rules during retirement and choosing the right retirement income products also present difficulties.

Less concerning, but still notable, are estimating life expectancy, future healthcare costs, estate planning, aged care costs and health insurance, each with lower percentages of concern among respondents.

For retirement planning guidance, Australians primarily turn to financial advisers (40%) and resources provided by superannuation funds (38%). Friends and family also play a significant role (30%), along with accountants (23%).

Many seek information from personal finance websites, magazines and podcasts (20%). Government resources like Centrelink, the ATO website and the Australian government Financial Information Service are also consulted, along with ASIC's MoneySmart website and financial counselling services.

A smaller percentage refers to the Association of Superannuation Funds of Australia (ASFA) retirement income standards.

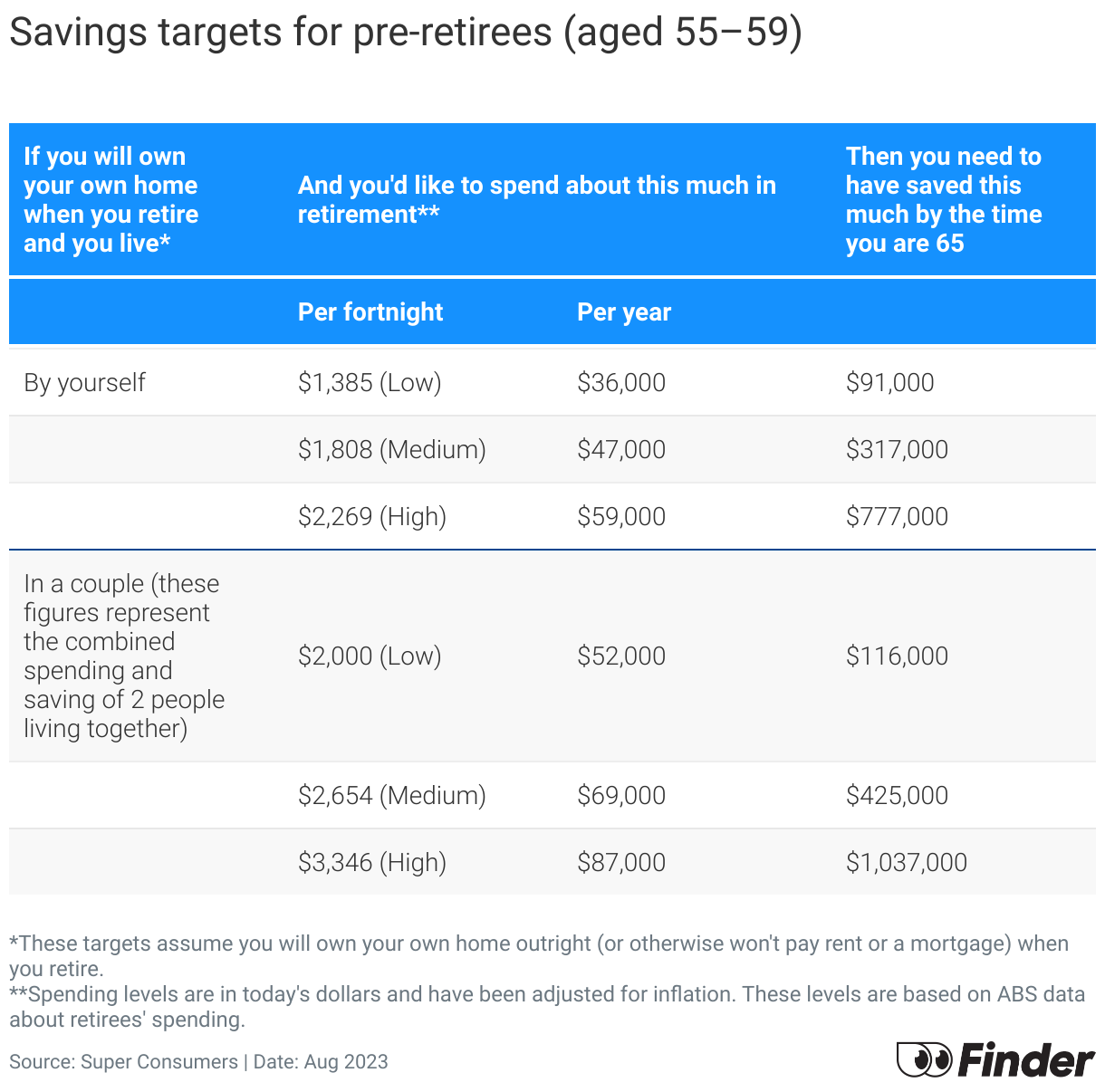

If living alone, you'd need to save between $91,000 (for a low spending level of $36,000 per year) and $777,000 (for a high spending level of $59,000 per year) by age 65.

Couples need to save between $116,000 (low spending of $52,000 annually) and $1,037,000 (high spending of $87,000 annually).

Note: These figures are based on Australian Bureau of Statistics (ABS) data about retirees' spending, adjusted for inflation.

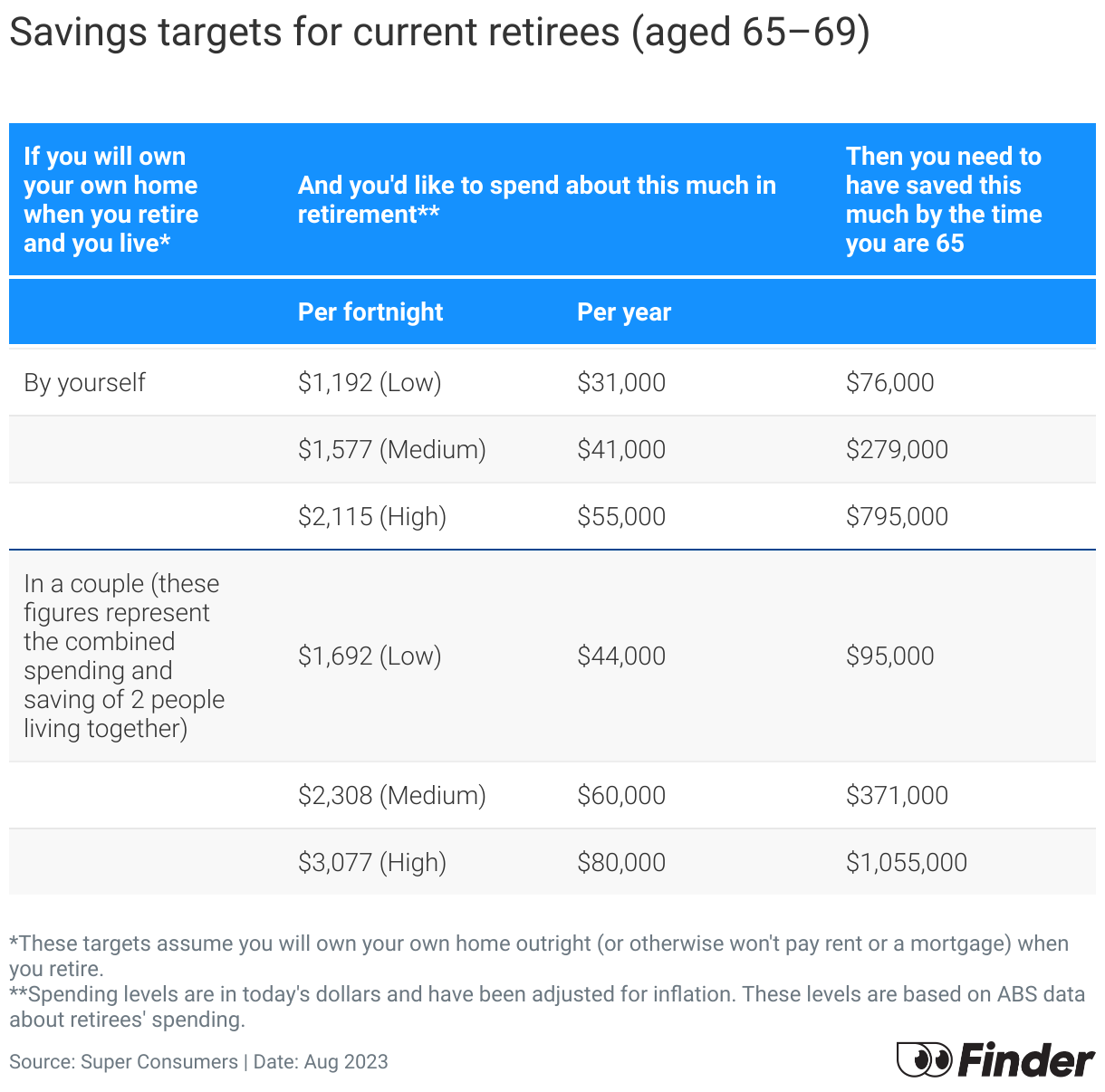

Individuals require savings ranging from $76,000 (for a low yearly spending of $31,000) to $795,000 (for high spending of $55,000 annually).

For couples, the required savings range from $95,000 (for low yearly spending of $44,000) to $1,055,000 (for high spending of $80,000 annually).

Note: These figures are also adjusted for inflation based on ABS data.

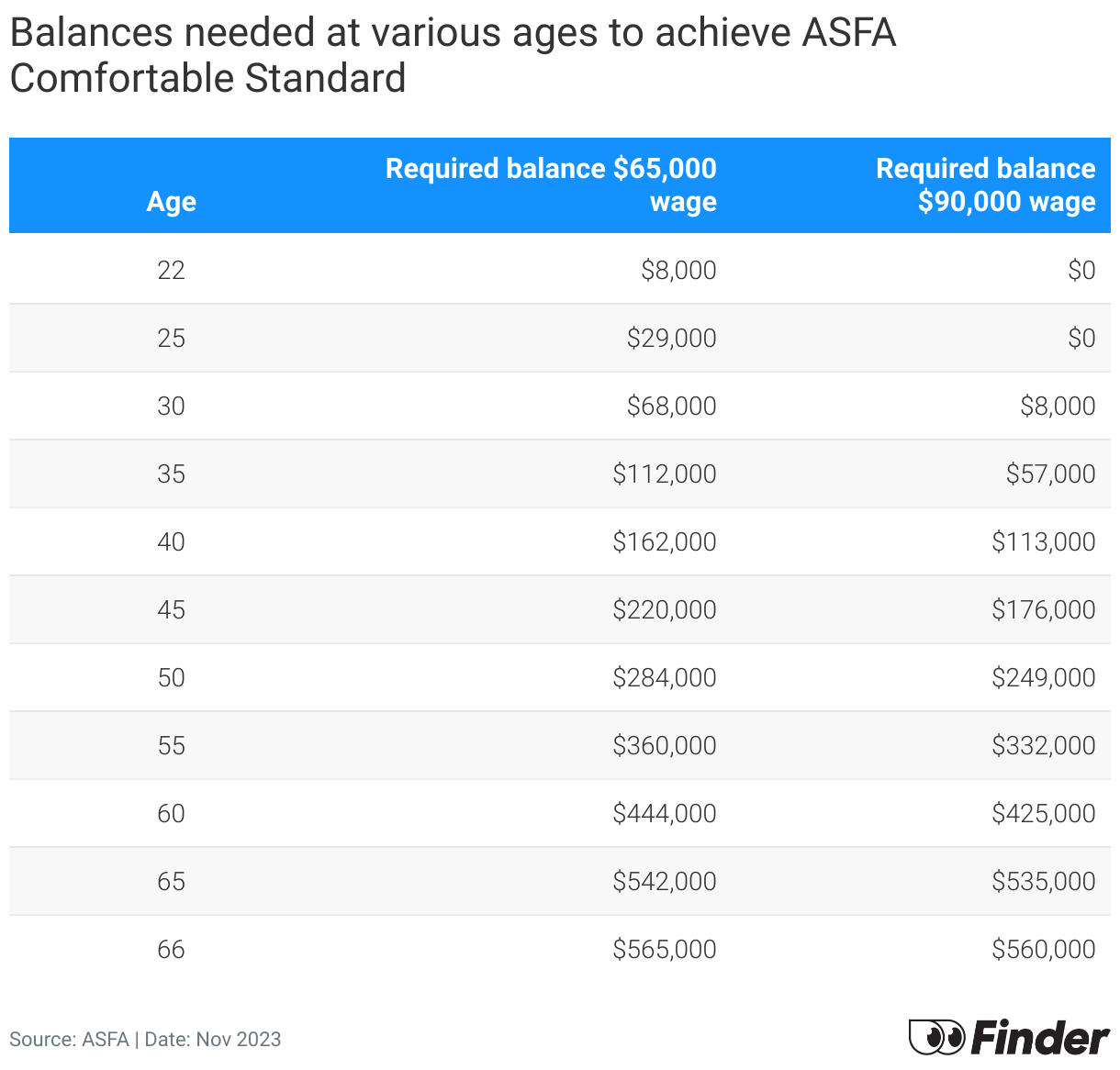

The ASFA Comfortable Standard is a benchmark for retirement savings, providing guidelines on the superannuation balance required for a comfortable lifestyle. This standard varies depending on age and salary.

For instance, at age 22, with a $65,000 wage, the target balance is $8,000, escalating to $565,000 by age 66.

This section provides financial benchmarks for Australians nearing or in retirement. It offers specific savings targets based on age and desired spending levels, using data adjusted for inflation.

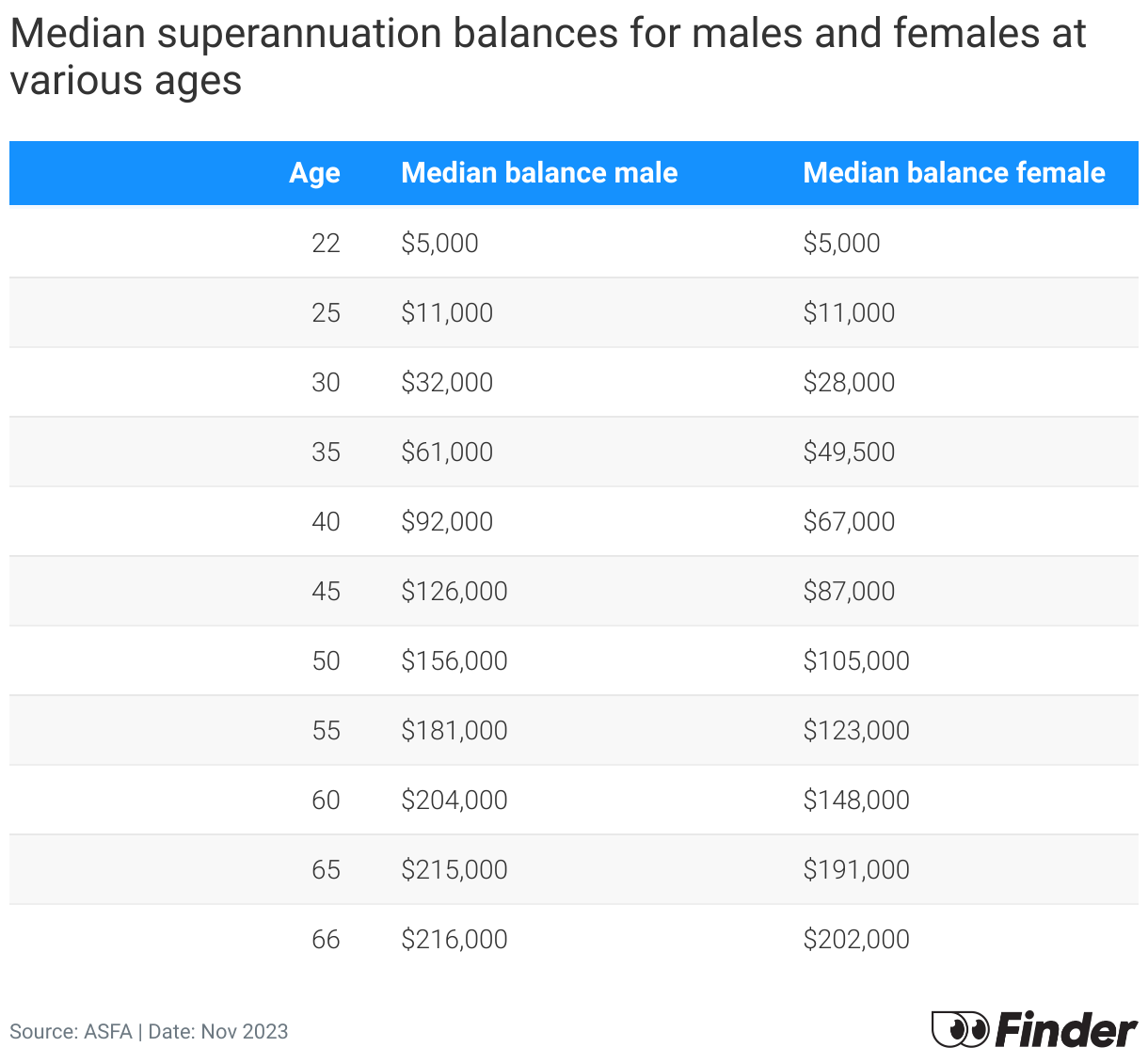

The median superannuation balances for men and women at various ages show a gender gap in savings. By 65, men have an average of $215,000, while women have $191,000.

This gap is largely attributed to several factors including career breaks, part-time employment and wage discrepancies, which disproportionately impact women's earning and saving potential over time.

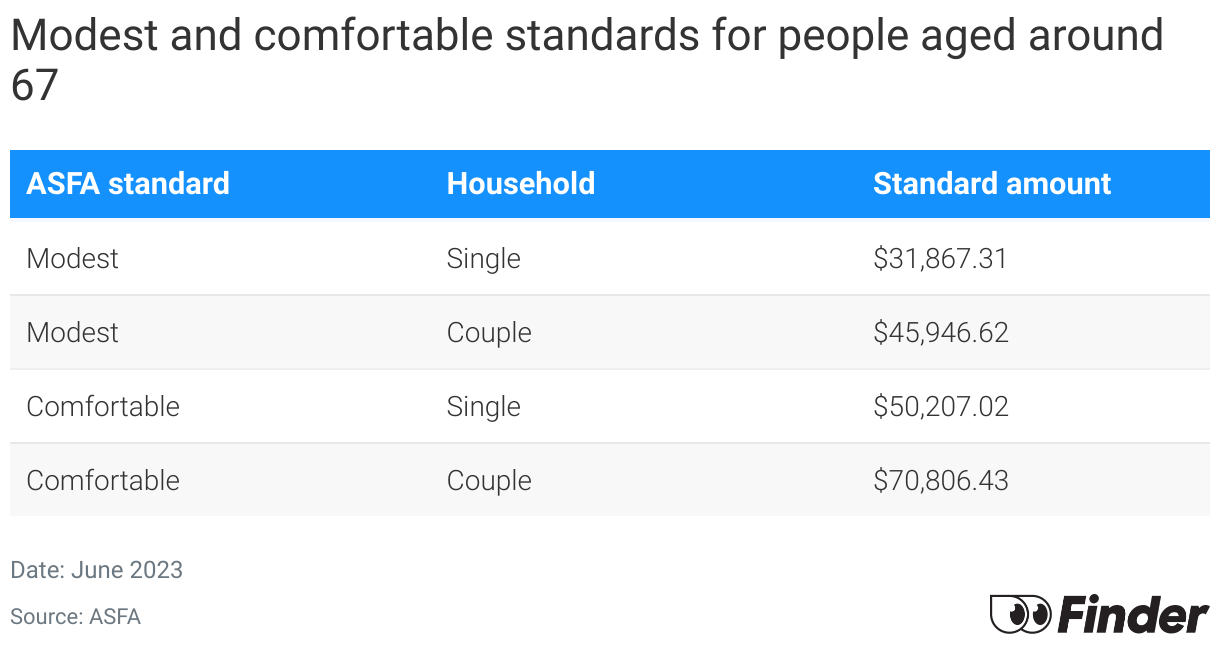

In planning for retirement, understanding different lifestyle standards is essential. According to ASFA:

Remember, these are just benchmarks to help guide your planning.

Use our free superannuation calculator to see your projected retirement balance, and how this could change by switching funds.

The average super balance is $154,350. Compare your super balance against the average balance for your age group to see if yours is on track.

Hostplus is an industry super fund with strong past-performance returns and low fees.

Here’s why it’s so important to consolidate your super, and the steps you need to follow to roll over your super today.

Sunsuper is an industry super fund that meets your needs as you move through the workforce and transition into retirement.

A comprehensive review of AustralianSuper, its investment options and how it can help you save for retirement.

Find a superannuation solution to suit your life stage, financial situation and retirement goals with UniSuper.

Unsure which super fund to choose? Here's what to look for when choosing your own super fund to ensure it's the best one for you.

Vision Super is a profit-for-members fund with 13 investment products to choose between including a MySuper option and an ethical option.

Aware Super is a low-fee super fund with 12 different ways to invest including a MySuper option and an ethical investment option.