Leasing a car can be cheaper in the short-term and you can upgrade the car every few years, but you won't own anything.

Buying a car gives means you own the asset and you can sell it later if you need to. You pay more upfront but probably save in the long run.

Before deciding between leasing or buying, factor in your total costs including fees, taxes and depreciation.

"To lease a car, or to buy a car, that is the question."

If you can't decide between buying or leasing a car, then our guide will help you.

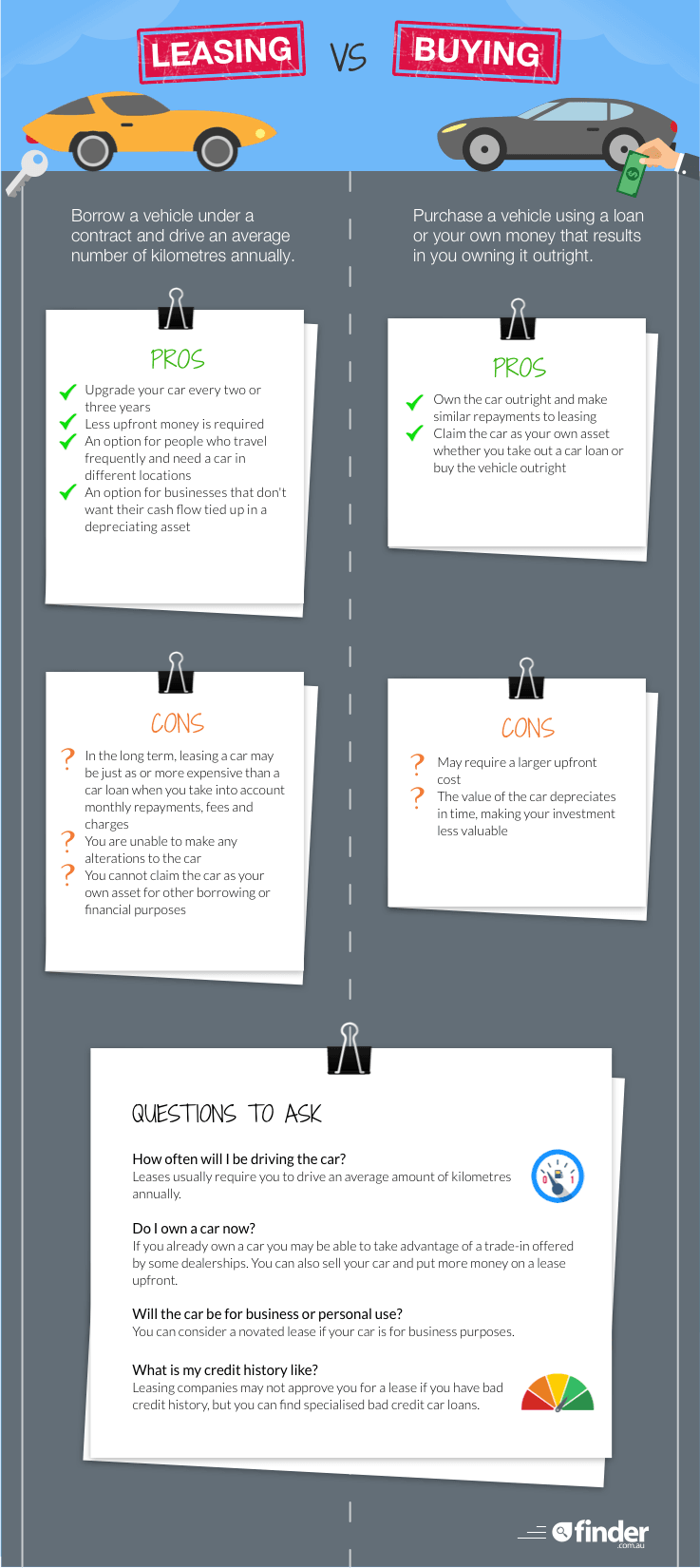

What is the difference between leasing and buying?

The key difference between buying and leasing a car is ownership of the vehicle, but this could be a positive or negative depending on your situation.

In general, leasing will offer more flexibility and likely cost less. Buying a car will likely to be more expensive, but could give you greater stability and the benefits of ownership.

Leasing a car gives you access to a vehicle for an agreed period, which can be for personal or business use, or a combination of the two. You will generally make regular payments over the course of the lease and may have the option to buy the car, or starting leasing a new vehicle, at the end of the lease term.

Buying a car involves you purchasing a vehicle so that you own the vehicle outright. You can either make your purchase using a car loan, which can be paid off in a period of up to seven years, or by buying the vehicle using your own savings. You are then free to use the vehicle as you wish, as well as sell it.

Buying vs leasing: Pros and cons

Pros

Cons

Leasing

Does not tie you down to a single vehicle and gives you the option of upgrading your car every two or three years

Requires less upfront money

Is an option for people who travel frequently and need a car in different locations

Leasing may be a good option for businesses who don't want their cash flow tied up in a depreciating asset

Often sill covered by the manufacturer's warranty, so servicing and ongoing maintenance charges are usually covered

In the long term, leasing a car may be just as or more expensive than a car loan when you take into account monthly repayments, fees and charges

You are unable to make any alterations to the car

You cannot claim the car as your own asset for other borrowing or financial purposes

Buying

If you decide to take out a loan your repayments will be similar to what you would pay when you were leasing, but at the end of the term you will own the car outright

Whether you take out a car loan or buy the vehicle outright, you can still claim the car as your own asset.

May require a larger upfront cost

The value of the car depreciates in time, making your investment less valuable

What financing options are available for cars?

Secured personal loan. A personal loan that is secured works by you using the car as a guarantee in order to finance it. This is less of a risk for the lender as they can sell the car should you default on the loan. These loans generally have lower rates and fees and are offered as a fixed or variable rate option.

Unsecured personal loan. An unsecured personal loan can not only be used to finance a vehicle, but can also be used for any other purchase you wish to make. These loans are flexible but they usually come with higher fees and rates because it is a risk to the lender.

Dealer finance. If you purchase a car from a dealership then they will most likely have a financing option they are able to offer you. It's best to do your research before you sign up as dealer financing usually comes with inflated rates and high fees. Dealer finance usually comes with a balloon payment at the end that is designed to lower your ongoing repayments.

Novated lease. A novated lease is basically a lease agreement between you, your employer and the lease provider. Some of your lease obligations are transferred to your employer and as such your car is treated like a company car for tax purposes. This type of lease can save you money by allowing you to access benefits such as GST discounts, income tax savings and savings on the cost of running the car.

We currently don't have that product, but here are others to consider:

Looking for other options? Check out these similar products.

How we picked these

Finder Score for car loans

To make comparing car loans even easier we came up with the Finder Score. Interest rates, fees and features across 200+ car loan products and 100+ lenders are all weighted and scaled to produce a score out of 10. The higher the score, the more competitive the product.

Frequently asked questions about leasing or buying a car

Yes. Many lease contracts give you the option to buy the car at the end of your lease term, often for a pre-agreed residual value. You'll need to check your agreement for specific terms, including any fees or conditions for an early or end-of-term purchase.

If you go over the set kilometre limit, you may be charged an additional fee for each extra kilometre. The cost per kilometre is outlined in your lease agreement, so it's important to estimate your driving habits accurately before signing.

For business use, leasing can be more tax-efficient because you can generally claim lease payments as a deductible expense. However, buying may make more sense if you plan to keep the car long term, as you can claim depreciation and interest costs. It depends on your cash flow, business structure and how long you intend to use the vehicle.

Usually not. Most lease agreements don't allow you to make modifications because the car must be returned in its original condition, minus normal wear and tear. Any unauthorised changes may result in additional charges at the end of the lease.

A lease typically includes the vehicle's use, registration and sometimes insurance and servicing if you choose a fully maintained lease. However, costs like fuel, tolls and excess wear and tear remain your responsibility.

Yes, but ending your lease before the agreed term often involves break fees or paying out the remaining balance. It's worth contacting your lender or leasing company to understand the total cost before deciding to terminate early.

A lease appears on your credit report as an ongoing financial commitment. Making regular, on-time payments can help build a positive credit history, while missed or late payments can negatively impact your score.

At the end of the lease, you can usually choose to return the car, extend the lease or buy the car for the residual value. You'll also need to ensure the car meets the return condition requirements set out in your lease agreement.

Leasing can be a smart way to drive an EV without committing to ownership, especially as battery and technology improvements continue. You can upgrade to newer models more easily once your lease term ends.

Yes. Just like buying a car, the lease price, term length and included services may be negotiable. Comparing offers from multiple leasing providers can give you leverage to secure better terms.

Matt Corke is Finder’s head of publishing ventures. Prior to this he was head of publishing for Australia, New Zealand and emerging markets. Matt built his first website in 1999 and has been building computers since he was in his early teens. In that time, he has survived the dot-com crash and countless Google algorithm updates.

See full bio

Query : Lease or Finance

If I want to lease a $40000 car for 3 years for business use will this be treated as a loan as compare to Finance

If I Finance $30k with balloon payment of 10K at the end of 5 years what is my actual loan amount

$30K or $40K

I Want to know this as I will need a home loan 2years down the track.

what is the right approach to lease or to finance

Finder

MayJuly 23, 2018Finder

Hi Rahul,

Thank you for your inquiry and sorry for the delay.

1. If I want to lease a $40000 car for 3 years for business use will this be treated as a loan as compared to Finance?

Well, that depends on the type of car leasing you would choose. You can either go for “operating lease”, “finance lease” or “fleet management”. These three options are well-explained from the link above.

2. If I Finance $30k with a balloon payment of 10K at the end of 5 years what is my actual loan amount $30K or $40K

As to the actual loan amount, this will depend on the company/lender you go with, their interest charged to the loan, and the term. You might also add to the total loan amount the fees involved in the loan. You can learn more and compare your car loan without balloon payments.

3. What is the right approach to lease or to finance?

As we’re a comparison website, I’m afraid we can’t really suggest or recommend, as it entirely depends on your business financial situation. Both leasing or financing have pros and cons, so it’d be best to consider the financial factors as well as your business needs. The above article gives helpful advice about going for a lease or buying (including through loan financing) your business vehicle.

Hope this helps.

Cheers,

May

JacquelineApril 1, 2017

I have salary packaged the full amount possible. Am I still able to get tax benefits if I choose to lease a vehicle.

ArnoldApril 16, 2017

Hi,

Thanks for your inquiry.

Yes, you are still able to get tax benefits when opting for Novated Lease. This type of lease can save you money by allowing you to access benefits such as GST discounts, income tax savings, and savings on the cost of running the car.

Hope this information helped.

Cheers,

Arnold

SteveAugust 22, 2016

I work for a mining company who offer novated leases (employee contribution method) to employees.

There are two companies nominated to manage the lease arrangements.

I have found a suitable vehicle and have had quotes for lease finance from financiers not connected with then novation management companies for this vehicle.

According to the information that is available from the novation management companies on their website, there appears to be no restriction on where the vehicle is financed. In other words, it appears that I can source cheaper finance from a finance company and have the vehicle lease novated through a management company.

According to the Novation management company representative, finance can only be arranged through them and not from an outside source.

Is this correct? Are novation management companies finance companies also or do they pressure consumers into taking their finance option?

Finder

ElizabethAugust 23, 2016Finder

Hi Steve,

As you enter into the novated lease agreement in your own name you should be able to choose the financier. The lease is a financial responsibility and if you change employers you’ll become responsible for the repayments, so it’s important to select a financier you’re happy with. However, your employer may only offer novated leases through these specific providers. It would be best to talk directly with your employer and explain that you’ve selected a different leasing company.

I hope this helps,

Elizabeth

DarrenAugust 6, 2016

The company I work for as a sales representative offers novated leases. With a novated lease, you don’t pay the GST with the purchase of the car, so there is a saving there. I get a reasonably good car allowance as part of my salary, and currently have a loan, and pay all the other running costs out of my own salary. I do a PAYG tax variation so that I get the tax benefit upfront each week. With this way, you can only claim the interest part of the loan, and then claim depreciation and other running costs, which varies year by year.

Which works out better between a Novated lease, and the above method of loan for someone who uses the car for 95% business use?

Many thanks

Darren

Finder

ElizabethAugust 8, 2016Finder

Hi Darren,

Unfortunately, I’m unable to offer you personal advice, so I can’t advise you either way. However, it really would depend on a number of factors which would work out better for you cost-wise. These include running costs, your car allowance, etc. We have a few tools on finder that can help, including a novated lease calculator, but you may want to get some tax advice in this matter.

Thanks,

Elizabeth

DavidJuly 4, 2016

I’m about to start a 7-month stay in Australia as a visiting academic, with my family of 4.

Is it a good idea (and will I get approval) to lease a car for that period or should I directly look into buying 2nd hand?

Thanks in advance

David

Finder

ElizabethJuly 5, 2016Finder

Hi David,

Unfortunately, I can’t give you personal advice because it really depends on your personal financial situation, but it may help to break down the costs of each option to work out what may work best for you.

In terms of buying a car, there are several costs involved and you will also need to factor in insurance. If you wish to learn more about the expenses and costs of getting a car, please read our buying a car guide. With car rental, these costs will be factored into the rental cost. You may also be able to save with car hire coupon codes. Car-sharing services such as GoGet are another option to consider.

Want to buy a classic car but don't have the ready money? There are still financing options available for classic vehicles. Find out what loans you have to choose one and which one will work best for you.

Find out the range of RACV Car loans available for you to compare. You can finance a new car and lock in a competitive rate for your loan – find out about all the fees and features that come with this loan to apply today.

Important information about this website

Finder is a comparison service. We do not compare every product or every provider in the market.

We make money through commercial arrangements with some of the providers on this site. Products marked 'Sponsored', 'Promoted', 'Featured' or 'Advertisement' appear as a result of a commercial arrangement.

Our editorial content, product reviews and any 'Top Pick' designations are prepared independently of these commercial arrangements.

The default order of products in our tables can be influenced by commercial arrangements. You can re-sort or filter using the controls above each table.

Some content on this site may be generated or supported by AI tools. You should verify details directly with the provider.

Finder is one of Australia's leading comparison websites. We are committed to our readers and stand by our editorial principles.

Our comparison service does not include every product or every provider in the market. Some product issuers offer their products under multiple brands or through associated companies. Where we can, we identify the underlying issuer so you can compare like with like, but you should always check with the provider directly to confirm which brand you are dealing with.

Finder is a comparison website and an intermediary. We are not a product issuer and we do not provide personal financial or credit advice. When you click a link to a product, or apply for a product through our site, you deal directly with the product issuer. We may receive a referral fee, commission or other payment from the issuer if you click through, apply or take out a product. We describe these arrangements in more detail under 'How we make money' below.

Product features, fees, terms and eligibility criteria are set by the product issuer and may change. We rely on information supplied by issuers when we present product details on our site. Before you apply for or take out any product, you should confirm the details directly with the issuer.

We earn revenue from Finder in four principal ways:

Referral fees and commissions. When you click a product link, complete an enquiry form or apply for a product through our site, we may receive a referral fee, commission or other payment from the product issuer. We may also receive payment based on the volume of leads or conversions we send to an issuer.

Sponsored placements. Products marked 'Sponsored', 'Promoted', 'Featured' or 'Advertisement' appear as a result of a commercial arrangement between Finder and the issuer. These labels always indicate a paid placement. We do not use them for editorial choices.

Display advertising. Banner advertising, newsletter advertising and similar display ads on our site are paid by advertisers.

Content sponsorship. Some articles, videos and social media posts are sponsored by an issuer and are clearly labelled as such.

Our editorial opinions, product reviews and any 'Top Pick' designations are prepared independently of these commercial arrangements. A 'Top Pick' is an editorial choice made by our writers and editors based on the criteria described on each comparison page. A 'Top Pick' is not a personal recommendation and does not mean the product is appropriate for your circumstances.

If you would like to know whether we have a commercial arrangement with a specific product issuer, please contact us.

When products are grouped in a table or list, the default order can be influenced by commercial arrangements we have with product issuers. In some categories, sponsored or featured products appear in the top positions of the table by default, and are always labelled as such.

Other factors that influence default order include price, fees and features, and (where relevant) our editorial view of the product.

You can re-sort every comparison table using the controls above the table. You can filter by product features that matter to you. The order you see after re-sorting or filtering is not influenced by commercial arrangements.

Some content on this site is generated or supported by artificial intelligence tools, including our AI-powered assistant FinderBot. AI-generated content may contain errors. Please verify important information directly with the product issuer before making a financial decision. For more information about FinderBot, see the FinderBot Terms of Use and FinderBot Privacy Collection Notice.

Please read our website terms of use and privacy policy for more information about our services and our approach to privacy.

We update our data regularly, but information can change between updates. Confirm details with the provider you're interested in before making a decision.

Our goal is to create the best possible product, and your thoughts, ideas and suggestions play a major role in helping us identify opportunities to improve.

Query : Lease or Finance

If I want to lease a $40000 car for 3 years for business use will this be treated as a loan as compare to Finance

If I Finance $30k with balloon payment of 10K at the end of 5 years what is my actual loan amount

$30K or $40K

I Want to know this as I will need a home loan 2years down the track.

what is the right approach to lease or to finance

Hi Rahul,

Thank you for your inquiry and sorry for the delay.

1. If I want to lease a $40000 car for 3 years for business use will this be treated as a loan as compared to Finance?

Well, that depends on the type of car leasing you would choose. You can either go for “operating lease”, “finance lease” or “fleet management”. These three options are well-explained from the link above.

2. If I Finance $30k with a balloon payment of 10K at the end of 5 years what is my actual loan amount $30K or $40K

As to the actual loan amount, this will depend on the company/lender you go with, their interest charged to the loan, and the term. You might also add to the total loan amount the fees involved in the loan. You can learn more and compare your car loan without balloon payments.

3. What is the right approach to lease or to finance?

As we’re a comparison website, I’m afraid we can’t really suggest or recommend, as it entirely depends on your business financial situation. Both leasing or financing have pros and cons, so it’d be best to consider the financial factors as well as your business needs. The above article gives helpful advice about going for a lease or buying (including through loan financing) your business vehicle.

Hope this helps.

Cheers,

May

I have salary packaged the full amount possible. Am I still able to get tax benefits if I choose to lease a vehicle.

Hi,

Thanks for your inquiry.

Yes, you are still able to get tax benefits when opting for Novated Lease. This type of lease can save you money by allowing you to access benefits such as GST discounts, income tax savings, and savings on the cost of running the car.

Hope this information helped.

Cheers,

Arnold

I work for a mining company who offer novated leases (employee contribution method) to employees.

There are two companies nominated to manage the lease arrangements.

I have found a suitable vehicle and have had quotes for lease finance from financiers not connected with then novation management companies for this vehicle.

According to the information that is available from the novation management companies on their website, there appears to be no restriction on where the vehicle is financed. In other words, it appears that I can source cheaper finance from a finance company and have the vehicle lease novated through a management company.

According to the Novation management company representative, finance can only be arranged through them and not from an outside source.

Is this correct? Are novation management companies finance companies also or do they pressure consumers into taking their finance option?

Hi Steve,

As you enter into the novated lease agreement in your own name you should be able to choose the financier. The lease is a financial responsibility and if you change employers you’ll become responsible for the repayments, so it’s important to select a financier you’re happy with. However, your employer may only offer novated leases through these specific providers. It would be best to talk directly with your employer and explain that you’ve selected a different leasing company.

I hope this helps,

Elizabeth

The company I work for as a sales representative offers novated leases. With a novated lease, you don’t pay the GST with the purchase of the car, so there is a saving there. I get a reasonably good car allowance as part of my salary, and currently have a loan, and pay all the other running costs out of my own salary. I do a PAYG tax variation so that I get the tax benefit upfront each week. With this way, you can only claim the interest part of the loan, and then claim depreciation and other running costs, which varies year by year.

Which works out better between a Novated lease, and the above method of loan for someone who uses the car for 95% business use?

Many thanks

Darren

Hi Darren,

Unfortunately, I’m unable to offer you personal advice, so I can’t advise you either way. However, it really would depend on a number of factors which would work out better for you cost-wise. These include running costs, your car allowance, etc. We have a few tools on finder that can help, including a novated lease calculator, but you may want to get some tax advice in this matter.

Thanks,

Elizabeth

I’m about to start a 7-month stay in Australia as a visiting academic, with my family of 4.

Is it a good idea (and will I get approval) to lease a car for that period or should I directly look into buying 2nd hand?

Thanks in advance

David

Hi David,

Unfortunately, I can’t give you personal advice because it really depends on your personal financial situation, but it may help to break down the costs of each option to work out what may work best for you.

In terms of buying a car, there are several costs involved and you will also need to factor in insurance. If you wish to learn more about the expenses and costs of getting a car, please read our buying a car guide. With car rental, these costs will be factored into the rental cost. You may also be able to save with car hire coupon codes. Car-sharing services such as GoGet are another option to consider.

I hope this information helps,

Elizabeth