Finder Parenting Report 2023

From pocket money to personal loans, Finder’s Parenting Report investigates how Australians are raising their children in 2023.

Let's face it, raising children ain't cheap. To make matters worse Australians are currently experiencing one of the most challenging housing markets in recent memory, among other rising expenses thanks to the cost of living crisis.

Emerging social trends are also shaping how parents raise their kids – working conditions have improved in recent years with increased paternity leave and work-from-home possibilities. Meanwhile, conundrums like the choice between public or private schools continue to be a hot topic.

Finder's Parenting Report, which surveyed 1,033 Australian parents of children aged under 12, makes sense of these often complex topics, aiming to provide consumers with insights on how Australian parents are managing their finances and how they are teaching the next generation about money.

Read all the latest data from our new 2026 Parenting report.

When it comes to pocket money, parents have been cutting back, most likely due to cost of living pressures. Children under 12 received just $8 a week on average. This is down from $10 in 2021. Kids in New South Wales can expect the most from their parents, earning a weekly allowance of $11 on average. Meanwhile, those in Queensland and Western Australia can expect to receive $8 and $7 respectively.

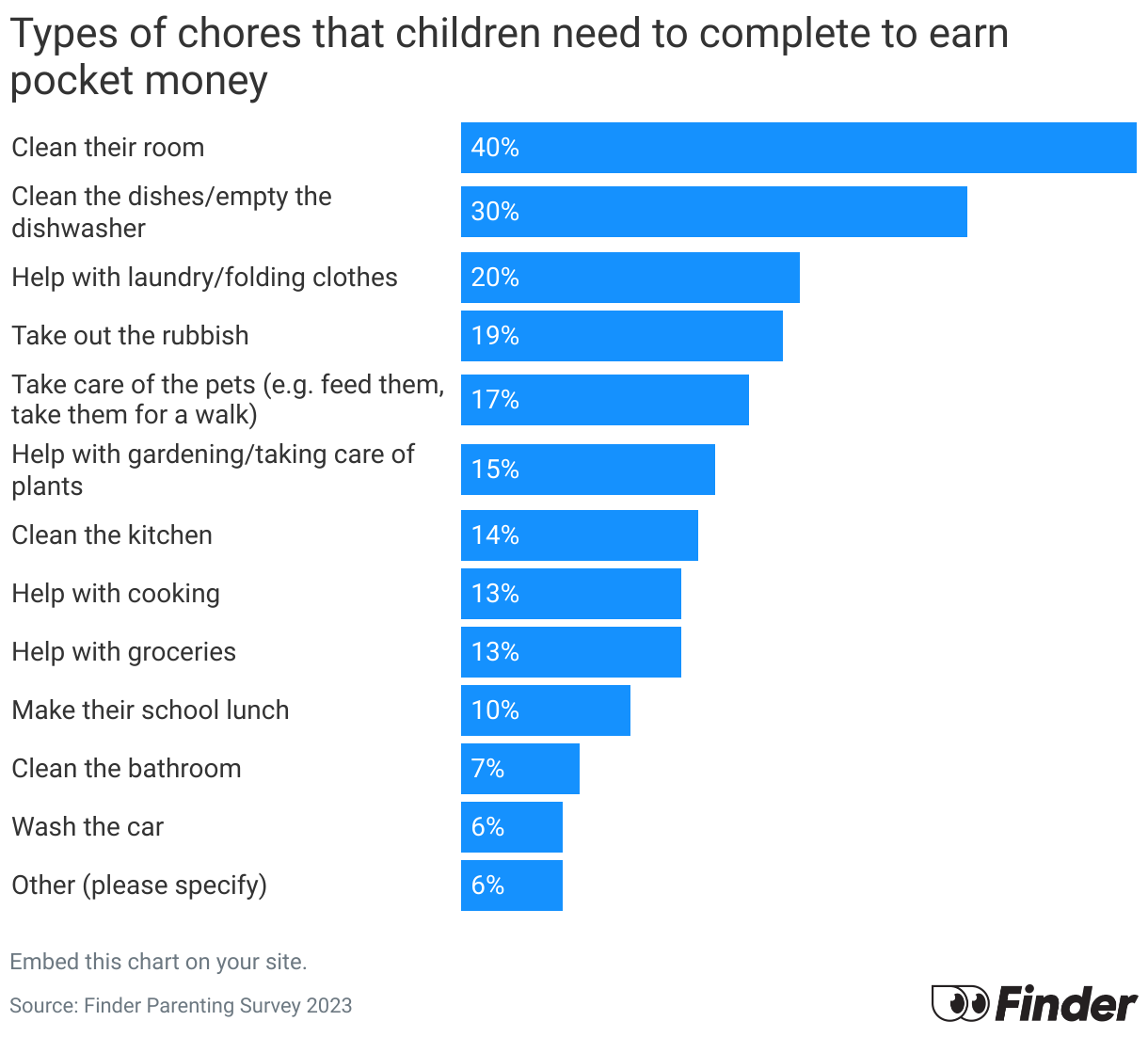

A whopping 2 in 5 (40%) parents admit their children do not have to complete any chores to receive their pocket money.

For those children that are put to work for their weekly wage, the most common chores include cleaning their room (40%), cleaning the dishes and emptying the dishwasher (30%), helping with laundry (20%) and taking out the rubbish (19%).

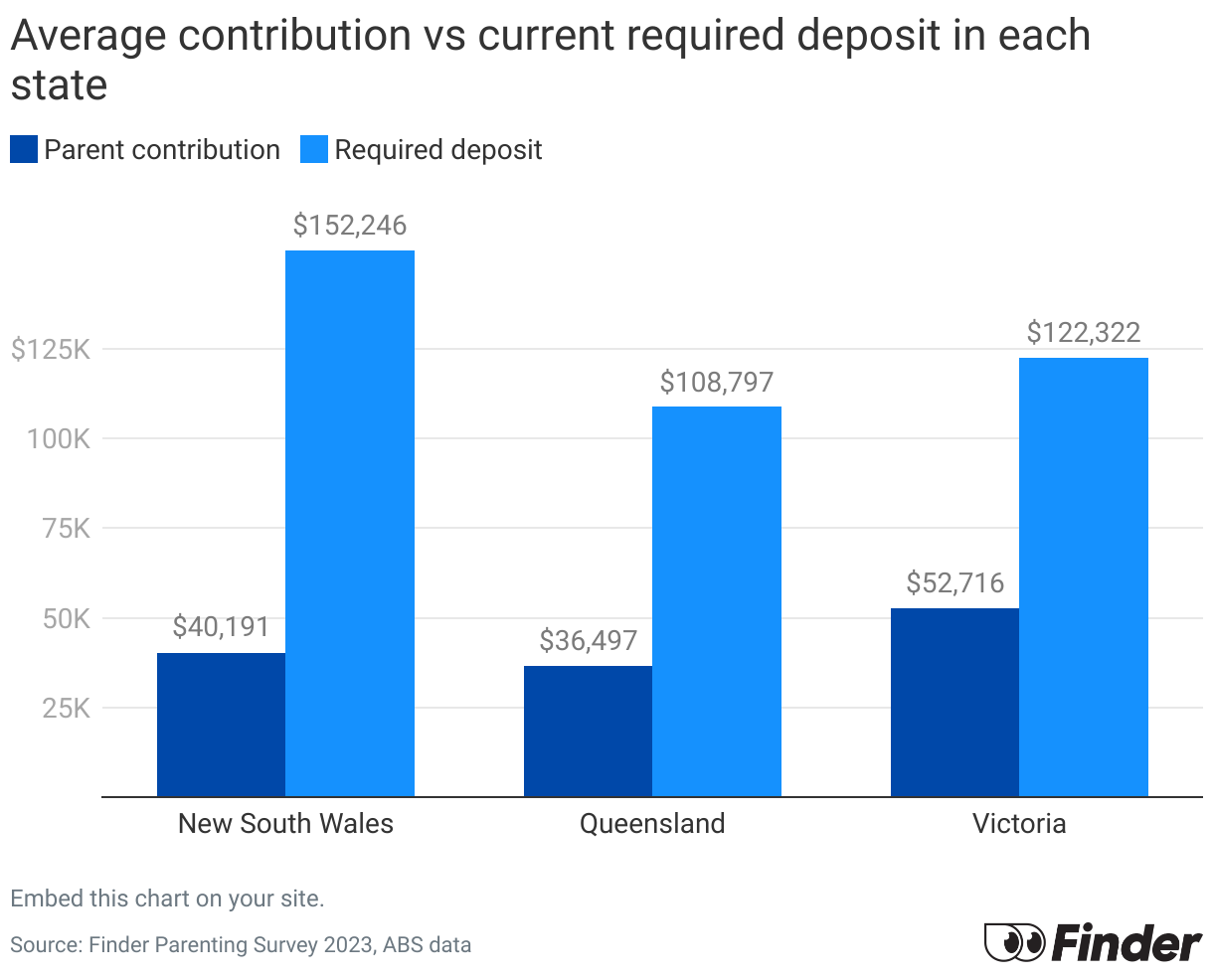

Looking to the future, buying a home is one of the biggest milestones many parents and kids will take into consideration. Finder data shows that the average Bank of Mum and Dad is planning to lend their children $33,278 towards a first home deposit. This is about a third of the current first-home buyer deposit ($98,617), based on the average first-home buyer loan of $493,085 in April 2023.

Parents in Victoria plan to lend the most financial help for their adult children to buy a home, gifting an average of $52,716, followed closely by parents in South Australia ($44,656) and New South Wales ($40,191).

However, many aren't planning on being so generous. More than 1 in 2 (51%) parents say they would give $1,000 or less to help their kids buy a home.

The Bank of Mum and Dad can be massively helpful and give fortunate children a much-needed boost in difficult times. However, some parents are going a step further, educating their children and providing them with a fundamental understanding of financial literacy from a young age.

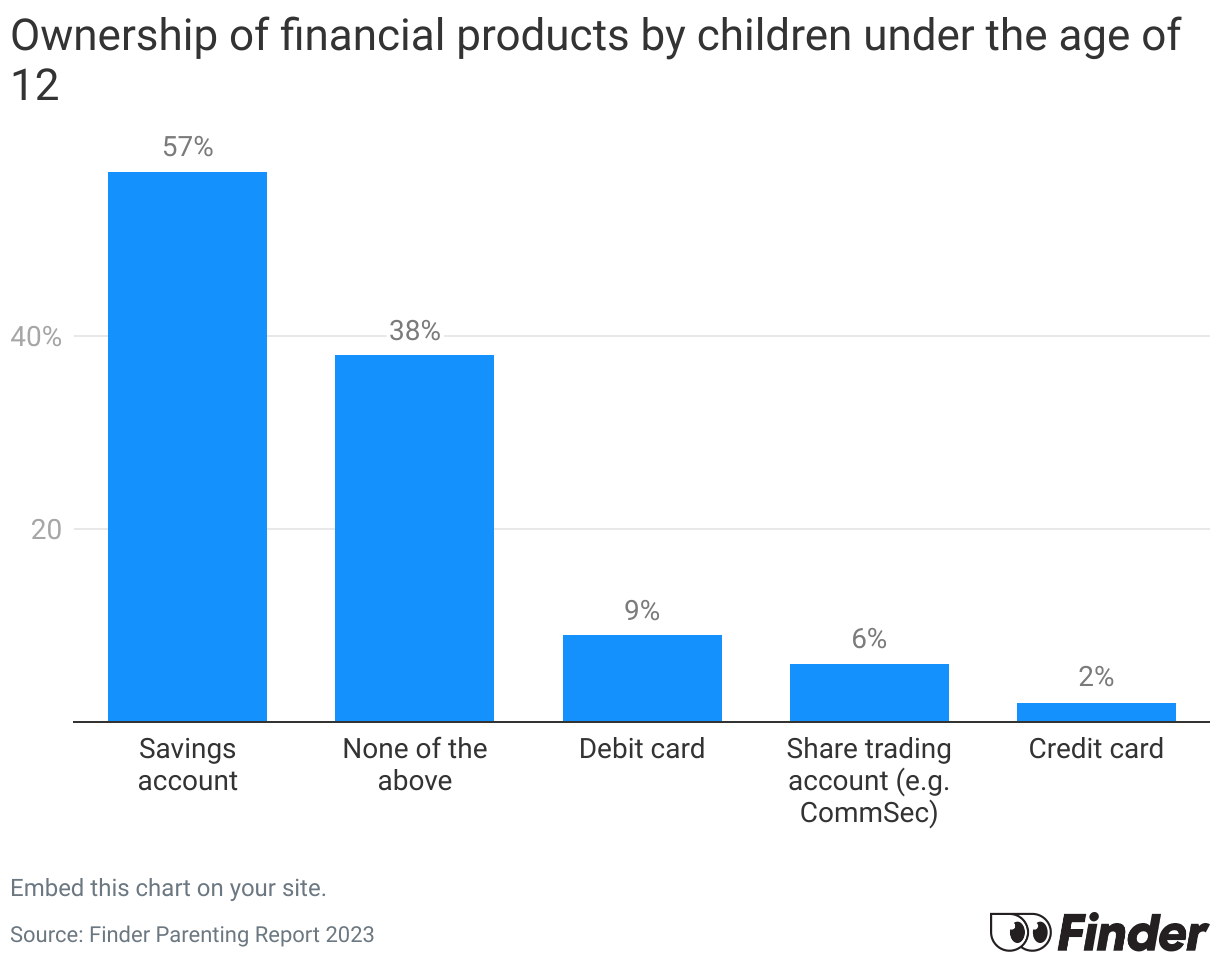

One of the most low-risk and positive financial behaviours is learning to save. More than half (57%) of parents have given their children access to a savings account. Moving on to other, more complicated forms of financial products sees usage from little tackers drop dramatically with only 9% of Aussie kids owning a debit card and 6% with access to a share trading account.

The thought of giving a primary schooler access to a share portfolio is a scary idea for many parents. However, apps like Spriggy and CommBank's Kit allow parents to give their kids access to these tools without losing control.

Financial literacy among Australians of all ages and genders declined between 2016 and 2020. According to findings from the Household, Income and Labour Dynamics in Australia (HILDA) survey of over 17,000 families released in late 2022, young individuals under the age of 35 saw the greatest drop in their financial expertise. Educating and establishing positive money habits early on in a child's life will hopefully help to reverse these worrying trends.

Over 2 in 3 (70%) parents believe they are responsible for developing financial literacy in their kids. While only 40% of respondents believe the onus of teaching financial literacy falls on schools, the vast majority (90%) believe financial literacy should be a compulsory subject in schools.

Almost half of the parents in the survey said they needed to tie the knot or be in a stable relationship before they had children. Other important milestones included buying a house, which was important to 43% of Aussie parents, and travelling, with 23% of respondents choosing to adventure before settling down and starting a family.

Possibly the most important consideration before bringing a baby into the world is whether your bank account can handle a new addition to the family.

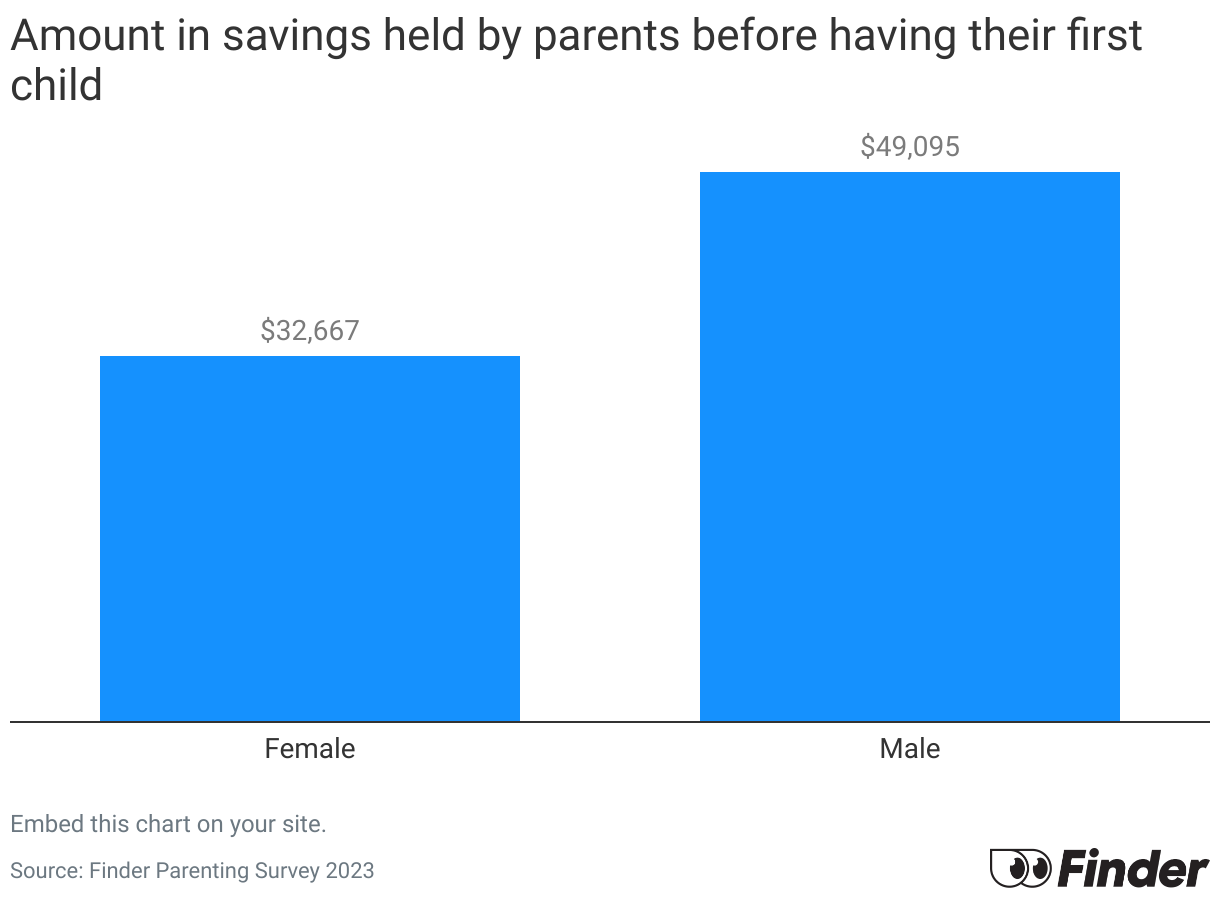

The average parent says they had just over $41,000 in savings before having their first child. Men had significantly more cash stashed away – a whopping $49,095 on average. Expectant mums had a lot less to rely on, with $32,667 in the bank.

Gen X parents, typically established in their careers, reported having $48,170 saved up compared to the $42,208 that their gen Y counterparts had stashed in the bank.

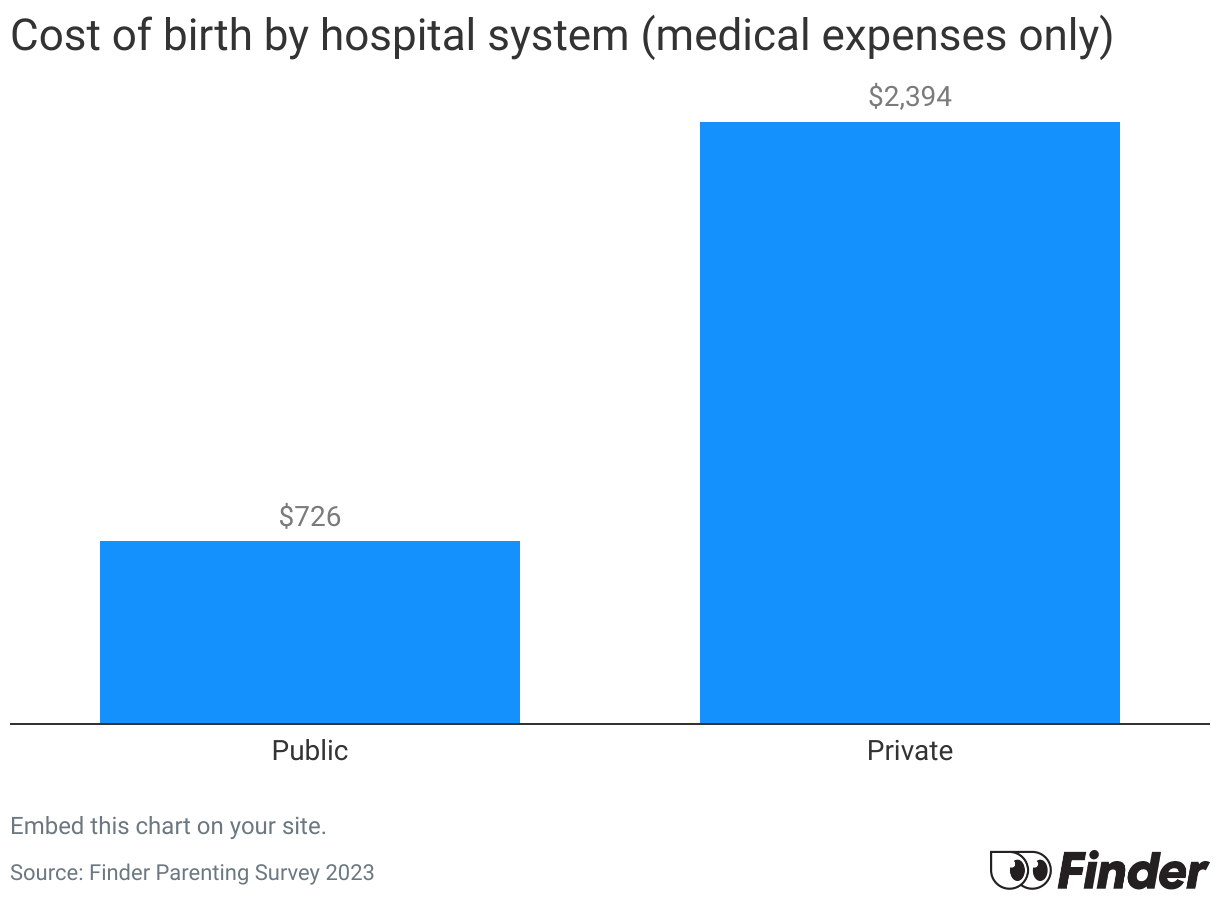

Ask any parent and they'll probably tell you the biggest day of their life was the day their little one was born – but it can also be one of the most expensive. The average Aussie will spend $1,244 on medical expenses, such as hospital visits throughout pregnancy.

The price of your pregnancy largely depends on which hospital system you choose: public or private. Using the public health system is significantly cheaper, costing $726 on average while those who prefer the perks of the private system will be left with an average bill of almost $2,400 once all is said and done.

The decision between public and private hospitals can be easy for some and a headache for others. Both options have their pros and cons. However, 2 in 3 Australians opted for a public hospital.

Older parents, specifically gen X, were the most likely to deliver in a private hospital with 35% choosing this option compared to only 15% of gen Z parents.

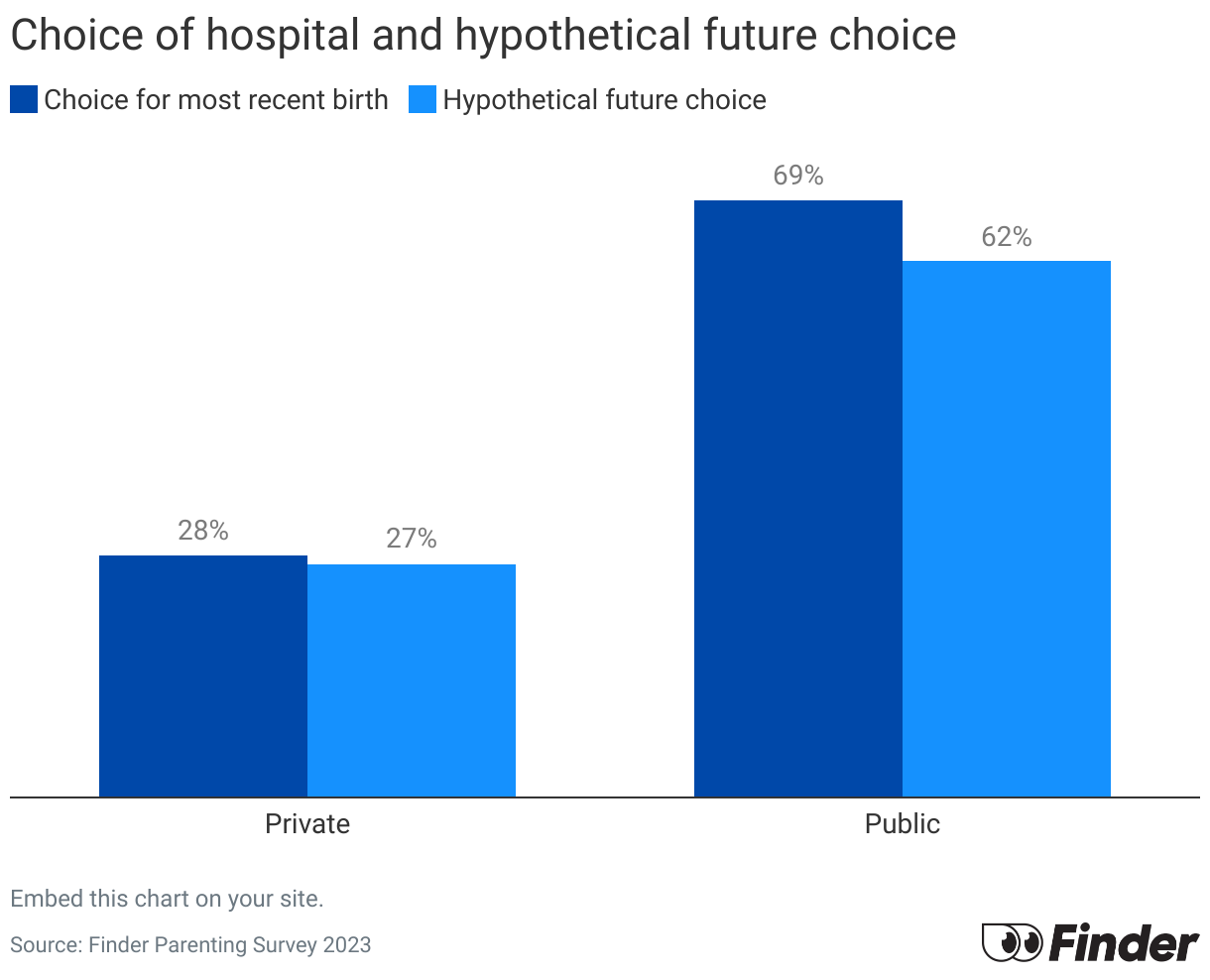

When asked which system they would use if they were to have another child, slightly fewer parents said they would use the public system, while the majority who went private would do so again. 1 in 10 parents said they were unsure what they would choose next time around.

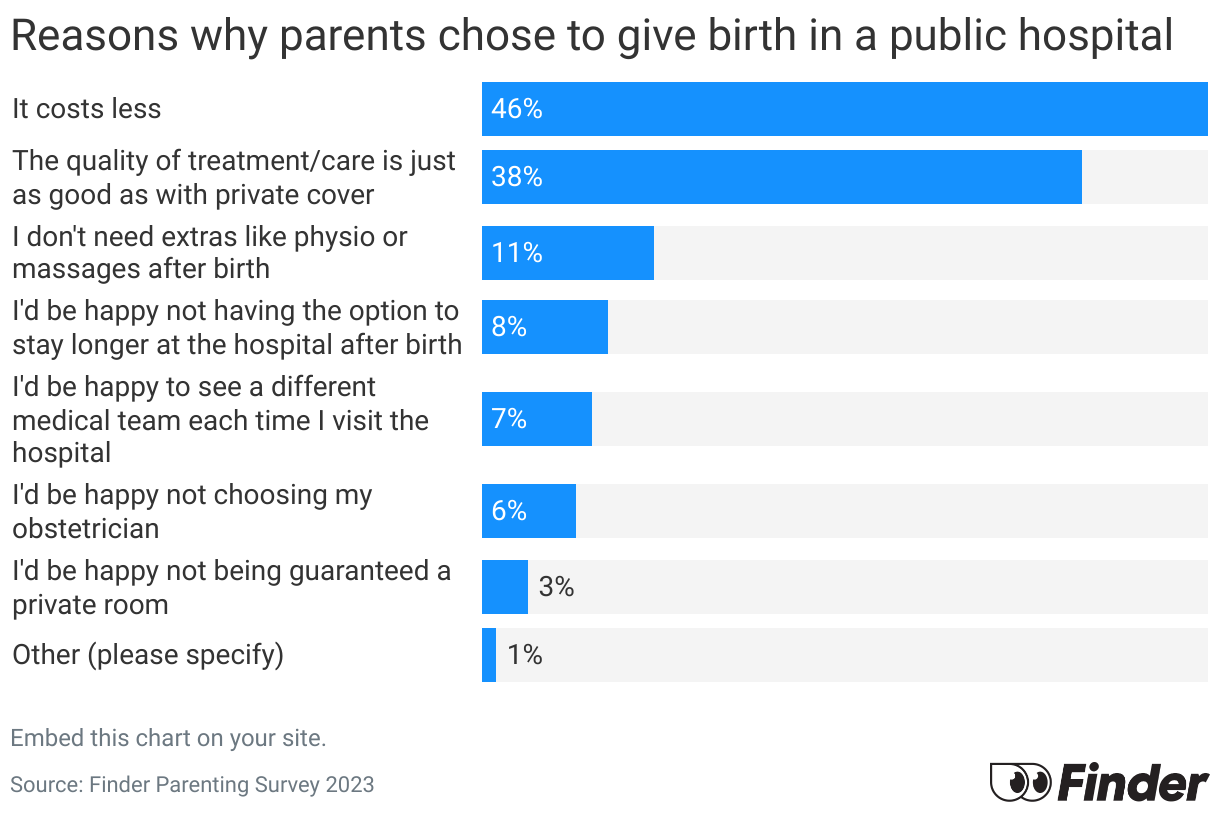

Reduced costs was the main reason almost half (46%) of parents said they would choose the public system. A further 38% believe the quality of care and treatment is equal to private cover.

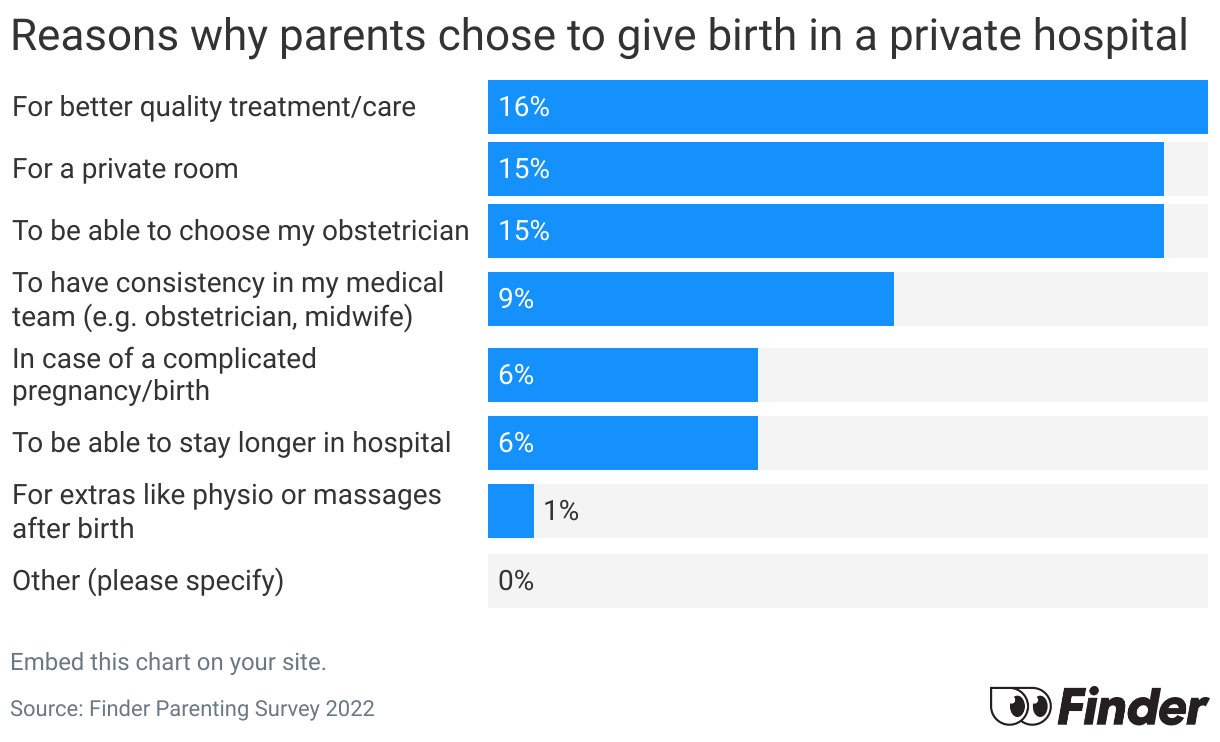

Parents who would choose private cover are more split, 16% would do so for better-quality treatment and care while 15% would like to be able to choose their obstetrician. A further 15% of parents prefer going private to use a private room.

Sarah Megginson – head of editorial, Australia

"Your kids' financial habits and their relationship with money starts really young – earlier than you might expect. From as young as 4 or 5, your kids will absorb your money values whether you're aware of it or not, because they're constantly soaking in life lessons from their biggest influence: you!

I'm a big fan of having open money conversations with your kids. Protecting your kids from money stress by not talking about it usually doesn't work, as a lack of money discussions has them coming up with their own stories about what your financial situation is. Also, when you don't talk about money, it can take on an air of being mysterious, taboo and hard work, which sets them up for future challenges.

Where do you start? It's in the language you use and the context you share with them. For instance, when they ask for things – which kids do constantly! – your reply might be, 'No, we can't afford it'. That's often the truth, but it also subtly sends the message that money is hard to manage and because of that, we miss out on fun things.

It might be more meaningful to say: 'We work really hard to pay for our home and our clothes and toys, so we're not going to spend money on ice-cream today. But do you want to make cookies later? Or we can add ice-cream to our shopping list next time we get groceries?' Or even, simply: 'No, we're not going to spend money on this today' is enough. It's a small but subtle shift in language that helps build the foundations of a positive relationship with money.

Having an open and healthy dialogue around money will also help them develop good financial habits, such as budgeting, saving and investing, because they're used to asking questions and working out the best way forward.

Lastly, when your kids are old enough to earn pocket money, gamify money to make it fun! A sticker chart or points chart can help make earning money fun and enjoyable. My kids earn points for each chore they do, and they get really competitive trying to beat each other, while also learning that they get rewarded for contributing."

James Martin – editor, insurance

"Before welcoming our first-born into the world, we looked for ways to save money. For example, most – if not all – of our bub's new room was kitted out with Facebook Marketplace finds. The one exception to our frugality was when we made the decision to go private.

This wasn't easy. Australia's public health system is the envy of most countries around the world. What's more, we spent far more than the $2,394 on average that most parents spend in the private system when having a baby. Our out-of-pocket costs totalled nearly 10 grand! One part was our insurance excess, a $750 wallet-slam we'd forgotten about until – full of exhaustion – we were leaving hospital on day 5.

The cost of going private was worth it for us. As with 15% of those surveyed in Finder's research, we welcomed the chance for a private room. But it wasn't just the possibility of having to share with another couple that turned us off going public; visiting hours apply to the secondary carer if you opt for the public system and that's not the case if you go private. I never had to worry about leaving my partner or my newborn's side for the first week. No amount of money we'd have otherwise saved would make up for that."

Head to our parenting hub for more family-related financial tips.

Following a cost of living crisis that won't let up, Finder’s Parenting Report explores how Australians are raising their children in 2026.

These savings accounts let you earn a decent ongoing interest rate on your cash with no annoying hoops to jump through.

You can open a joint savings account with another person to save for a shared goal. Here's how they work and how to find the best joint savings account for you.

See historical interest rates for savings accounts since January 2012.

Kickstart your savings plan with a high interest savings account.

Encourage your children to save with a savings account.

If you need help getting your savings back on track, a bonus saver account with competitive interest may provide you with the incentive and features you need.

See some of the best savings accounts in Australia right now with high interest rates and no fees, plus tips to help you find the best savings account for you.

Our range of simple calculators can help you plan your finances and compare potential interest earned.