Check your business credit score at least once a year to catch errors early and understand what lenders see before you apply for finance.

If your score is low, order your full business credit report to identify and resolve defaults or late payments before seeking a new loan.

Build a stronger score by paying on time, keeping credit applications limited and staying on top of any current loan payments.

While awareness of personal credit scores has been rising in Australia, business credit scores – yes, there are credit scores for business – are still woefully ignored by Australian small businesses. According to research from MYOB and small business lender OnDeck, 93% of businesses have never accessed their score.

Cameron Poolman, CEO of OnDeck, says the issue is awareness.

"I noticed that when the consumer credit scores became available. At that point, I thought small businesses really didn't know it either and it's just something where there just hasn't been the level of awareness in Australia that there has been, for instance, in the US, where FICO is a well-known score that people know."

Cameron Poolman

CEO - OnDeck

At OnDeck, we're trying to build people's awareness.

But what is a business credit score? What do you do if your score is low? And importantly, how do you find out your score?

What is a business credit score?

It is a number between 0 and 1,200 that is calculated using the information on your business credit file.

Source: Equifax

How is it different from a personal credit score?

According to Poolman, a business credit score doesn't include the personal information that is used to calculate individual credit scores.

Your company's file will contain:

Company details. Information on structure and current shareholders.

Public record information. This will include any legal matters or action taken against your firm by the Australian Securities and Investments Commission (ASIC).

Personal Property Securities Register (PPSR). Any information the PPSR have concerning your company's possessions will be on your credit file.

"A business credit score has got more of the commercial information, such as registered defaults, potential loan inquiries or any external administration that may be registered against the business, so it's very much the commercial and business attributes of the business," he said.

However, there are some similarities.

"In the same as in the personal space, without any positive credit reporting, it almost accentuates the negative. And so, it is quite difficult to get to build your credit score up again once you've got a negative listing or your score has dropped because you're not getting that positive reporting coming through to increase it," he said.

What impacts a business credit score?

Your business credit score is calculated using the information listed on your company credit file. This information includes:

Credit enquiries. Your business credit shopping patterns and the type of credit you've applied for can increase your credit score.

Time in operation. A newer business may be deemed riskier than a business that has been incorporated a longer time.

Director information. Court judgements, bankruptcies, defaults, external administration segments that are listed on a director's file.

Personal Property Securities Register (PPSR). Details of any PPSR registrations held on a business are listed in your file.

Company details. This includes the company structure, legal entity name, business address, directors, shareholders and more.

Information on the public record. This can include recorded liens, lawsuits, judgements or delinquent taxes.

Finder survey: Do Australians from different states know their business credit score?

Response

WA

VIC

SA

QLD

NSW

I don't have a business

52.14%

37.89%

55.7%

43.5%

42.67%

No

37.61%

51.58%

36.71%

46.64%

46.53%

Yes

10.26%

10.53%

7.59%

9.87%

10.8%

Source: Finder survey by Pure Profile of 1145 Australians, December 2023 Data for ACT, NT, TAS not shown due to insufficient sample size. Some other states may also be excluded for this reason.

Source: Equifax

What can damage your score?

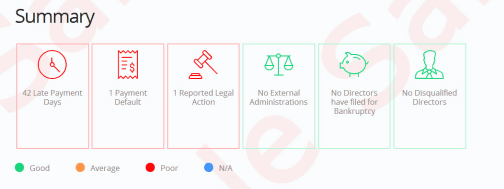

Business defaults and late or missed payments are some of the main contributing factors to a low score.

"Another way the score could be impacted is just by the quantum of applications for credit that you've made," said Poolman. "So if you are asking for credit from a large quantum of different institutions, that will have a negative impact on your score."

What else do lenders look at when considering you for a loan?

The criteria for business loans, and what information will be considered, varies greatly from lender to lender.

"If it's a secured loan, they're looking at the securities that the person has provided, and that might be over particular assets, it could be the business, or it could be the person's home that they're lending against. What's also important is the cash flow."

"We will look through, in detail, a company's cash flow and determine its ability to service the loan that they're looking to get. Other funders will look at profit and loss statements, balance sheets, tax returns. It's different for different funders."

What should you do if your credit score is low?

Poolman's advice to any business that has a low credit score is to order a copy of their business credit report, which they can get for free directly from a credit bureau.

"Once you get that report, you know if it's a default issue. So if I a supplier has defaulted you, you know who it is, and then you could determine whether you're able to settle that issue and then remove that from your file, which will generally increase your score."

If you've found out your business has been flagged as a credit risk, there are a few things you can do to appear as less of a risk to lenders and improve your business's credit score:

Make payments on time. This is the easiest and most effective way to quickly increase your credit rating.

Stay away from legal problems. Any involvements with the courts will be highlighted on your credit file and will tarnish the image of your company.

Keep in touch with your creditors. If repayments are getting out of hand or you are evaluating your financial situation, keeping your creditors or business loans manager in the loop may help your situation down the track.

Where can you get your credit score?

You need to pay to receive your business credit score directly from a credit reporting bureau, such as Equifax, but OnDeck allows small businesses to receive their credit score for free.

Poolman believes that more and more small businesses will be looking to access their credit score because of its importance when applying for loans.

"I think in time, consumers, as well as small businesses, will become more aware of their credit score because it impacts their ability to access credit."

"We want to be at the forefront of different opportunities to help small businesses. We'd say this is one way of doing it."

The difference between hard and soft pull credit checks

Not all credit checks negatively affect your credit score. Lenders do two kinds of checks before approving or denying a business loan application.

Soft pull inquiries

Individual and business profiles are subjected to soft pull inquiries everyday without being aware of it. Lenders can do a soft pull check for an overall idea of your financial status before pre-approving your application, or credit bureaus can soft pull your file if you request your credit score.

Soft pull inquiries have no impact on your credit score, but may be noted as a file access.

Hard pull inquiries

Hard pull credit inquiries involve an official check of your credit report. When you apply for a car loan, personal loan or home loan and allow a lender to check your credit file, the lender will conduct a hard pull. While soft pull inquiries have zero effect, hard pull checks are listed on your credit file and therefore can affect your credit score.

Every hard pull credit check is listed on your credit report, including which lenders have denied previous applications and how many times you've applied for loans in the past. Too many hard pull inquiries in a short space of time can negatively impact your credit score.

You have to give the lender permission to conduct a hard pull inquiry. Before submitting a loan application, make sure that your business meets all the criteria and has a good chance of being approved. While a hard pull will reflect on your credit report either way, carefully considering your loan options can help avoid adding rejected applications to the list.

Improve cash flow

If your business has a few outstanding invoices, invoice financing can help improve your cash flow and get access to funds you need. It's a type of business loan that is secured by the unpaid invoices and comes with reduced risk, no asset requirements or interest payments.

Compare invoice financing products below.

{"userFilters":[{"componentType":"MULTI-SELECT CHECKBOX","options":{"comparator":"contains","includeAllSelection":false,"defaultMatcher":"ANY","values":["8.95-10","6.95-8.94999","4.95-6.94999","0-4.94999"],"fields":[{"label":"[[FINDER_SCORE_BADGE|9+]] Excellent: 9+","value":"8.95-10","comparator":"range"},{"label":"[[FINDER_SCORE_BADGE|7+]] Great: 7+","value":"6.95-8.94999","comparator":"range"},{"label":"[[FINDER_SCORE_BADGE|5+]] Standard: 5+","value":"4.95-6.94999","comparator":"range"},{"label":"[[FINDER_SCORE_BADGE|0+]] Basic: 0+","value":"0-4.94999","comparator":"range"}]},"dataSelector":{"recordType":"PRODUCT","fieldCode":"FINDER_SCORE.FINDER_SCORE"},"dataType":"NUMBER","label":"Finder Score","queryParameter":"finderScore"},{"dataSelector":{"recordType":"UI_FILTER_COMPONENT","fieldCode":"SPECIAL_OFFERS"},"dataType":"BOOLEAN","label":"Special offers","componentType":"SpecialOffersFilter","config":{"VALUES":"1","fields":[{"value":"exclusive_only","label":"Finder Rewards & exclusives"},{"value":"all_offers_no_rewards","label":"All offers"}]},"options":{"comparator":"eq"}},{"config":{},"dataSelector":{"recordType":"product","fieldCode":"GENERAL.PROVIDER_ID"},"dataType":"UUID","label":"Provider","order":100},{"config":{"MULTISELECT":true,"VALUES":"$0-10000, $10000-$20000, $20000-$30000, $30000-$40000, $40000-$50000, $50000 and above"},"dataSelector":{"recordType":"product","fieldCode":"TABLE_FILTER.BORROW_AMOUNT"},"dataType":"TEXT","label":"How much do you need to borrow?","order":null},{"config":{"MULTISELECT":true,"VALUES":"Haven\u2019t started yet, 0-6 months, 6-12 months, 1 to 2 years, 2 to 3 years, 3 years+"},"dataSelector":{"recordType":"product","fieldCode":"TABLE_FILTER.BUSINESS_AGE"},"dataType":"TEXT","label":"How old is your business?","order":null},{"config":{"MULTISELECT":true,"VALUES":"$0, $1 - $50000, $50000 - $100000, $100000 - $200000, $200000 - $300000, $300000+"},"dataSelector":{"recordType":"product","fieldCode":"TABLE_FILTER.BUSINESS_REVENUE"},"dataType":"TEXT","label":"How much does your business make per year?","order":null},{"config":{"MULTISELECT":true,"VALUES":"Secured, Unsecured"},"dataSelector":{"recordType":"product","fieldCode":"TABLE_FILTER.LOAN_SECURITY"},"dataType":"TEXT","label":"Loan Security","order":null},{"config":{"MULTISELECT":true,"VALUES":"1 month to 12 months, 1 to 2 years, 2 to 3 years, 3 to 4 years, 5 years and above"},"dataSelector":{"recordType":"product","fieldCode":"TABLE_FILTER.LOAN_TERM"},"dataType":"TEXT","label":"Loan Term","order":null}],"niche":{"currencySymbol":"$","decimalPoint":".","decimalPlaces":"2","thousandsSeparator":",","filterBoundsMap":{"product.GENERAL.PROVIDER_ID":null,"product.TABLE_FILTER.BORROW_AMOUNT":null,"product.TABLE_FILTER.BUSINESS_AGE":null,"product.TABLE_FILTER.BUSINESS_REVENUE":null,"product.TABLE_FILTER.LOAN_SECURITY":null,"product.TABLE_FILTER.LOAN_TERM":null}},"prefilled":false,"experimental":false}

To get a credit score for your business, you need to have a credit file established with a credit reporting bureau, such as Equifax or Experian. This happens automatically when your business starts using credit, such as applying for loans or trade credit. You can then request your business credit report from these agencies.

An ideal business credit score varies by bureau, but generally, a score above 700 is considered strong. A good credit score indicates that your business has a reliable history of managing credit, which can help secure favourable terms on loans and contracts.

There is no set minimum credit score for opening a business account. However, to qualify for a business loan or line of credit, most lenders prefer a score of at least 600. Higher scores typically lead to better financing terms.

A poor business credit score is generally below 500, with a score of 500-600 being in need of improvement. A lower score indicates a high risk for lenders or suppliers, which can make it difficult for a business to secure financing or negotiate favourable terms. Missed payments, defaults, or legal judgments can negatively impact your score.

A company gets a credit rating by establishing a credit history through loans, credit lines, or trade accounts. Credit bureaus then assign a credit rating based on the company's payment history, credit usage and other financial behaviours. Regular reporting from lenders and suppliers helps build this credit profile.

Yes. Every time you apply for a business loan, the lender may run a credit check, which creates a hard inquiry on your credit file. Too many hard inquiries over a short period can lower your business credit score, so it's best to apply strategically rather than submitting multiple applications at once.

You can improve your score by paying all bills and loan repayments on time, lowering existing debt levels, correcting any errors on your business credit report and maintaining a healthy cash flow. Consistent good financial habits build a strong credit history over time.

Yes. Several credit reporting agencies and financial platforms allow you to check your business credit score at no cost. It's a good idea to review your report regularly so you can spot inaccuracies and take steps to improve it before applying for finance.

If you're a sole trader or have provided a personal guarantee on a business loan, your personal credit score can influence your business borrowing. For incorporated businesses with established credit profiles, the two scores are usually assessed separately, though lenders may still review both.

Your business credit score updates whenever new information is reported to credit agencies. This can happen monthly or more frequently depending on your credit activity - such as loan repayments, new credit enquiries or changes to your business details.

Authorised lenders, credit providers and other entities permitted by law can access your business credit file when you apply for credit or enter financial agreements. You can also access your own credit report to understand what information is being shared.

A low business credit score can make it harder to get approved for loans or may mean higher interest rates. You can rebuild your score by demonstrating positive repayment behaviour, reducing outstanding debt and ensuring all business information held by credit agencies is current and accurate.

Yes. Sole traders, partnerships, companies and trusts are assessed differently because the level of legal and financial separation between the owner and the entity varies. For example, companies have distinct credit profiles, while sole traders are often assessed using both business and personal credit data.

Discover more business resources right here on Finder

Elizabeth Barry is an experienced journalist with over 10 years of expertise in personal finance, contributing to outlets like the ABC, Sydney Morning Herald, and 7News. She holds a Master of Arts in Creative Writing and a Bachelor of Arts in Communication from the University of Technology Sydney, and has earned multiple award nominations, including a Highly Commended recognition at the 2017 Lizzies. Elizabeth began her career at Finder in 2013, progressing through roles to become Lead Editor, where she oversaw a wide range of personal finance coverage until 2024.

See full bio

Elizabeth's expertise

Elizabeth

has written

200

Finder guides across topics including:

Macquarie Bank is a trusted independent global financial services group offering a wide range of business loans for a variety of purposes. Find the right loan for your business here.

Are you looking for a business loan but don't have an asset to offer as security? You still have loan options available. Find out what you need to know about unsecured business loans and how to compare them.

A peer-to-peer business loan from innovative lender Zool Capital may be a consideration if you’re looking for business finance and we can show you how it works.

Important information about this website

Finder makes money from featured partners, but editorial opinions are our own.

Finder is one of Australia's leading comparison websites. We are committed to our readers and stand by our editorial principles.

We try to take an open and transparent approach and provide a broad-based comparison service. However, you should be aware that while we are an independently owned service, our comparison service does not include all providers or all products available in the market.

Some product issuers may provide products or offer services through multiple brands, associated companies or different labeling arrangements. This can make it difficult for consumers to compare alternatives or identify the companies behind the products. However, we aim to provide information to enable consumers to understand these issues.

We make money by featuring products on our site. Compensation received from the providers featured on our site can influence which products we write about as well as where and how products appear on our page, but the order or placement of these products does not influence our assessment or opinions of them, nor is it an endorsement or recommendation for them.

Products marked as 'Top Pick', 'Promoted' or 'Advertisement' are prominently displayed either as a result of a commercial advertising arrangement or to highlight a particular product, provider or feature. Finder may receive remuneration from the Provider if you click on the related link, purchase or enquire about the product. Finder's decision to show a 'promoted' product is neither a recommendation that the product is appropriate for you nor an indication that the product is the best in its category. We encourage you to use the tools and information we provide to compare your options.

Where our site links to particular products or displays 'Go to site' buttons, we may receive a commission, referral fee or payment when you click on those buttons or apply for a product.

When products are grouped in a table or list, the order in which they are initially sorted may be influenced by a range of factors including price, fees and discounts; commercial partnerships; product features; and brand popularity. We provide tools so you can sort and filter these lists to highlight features that matter to you.

Please read our website terms of use and privacy policy for more information about our services and our approach to privacy.

We update our data regularly, but information can change between updates. Confirm details with the provider you're interested in before making a decision.

How likely would you be to recommend Finder to a friend or colleague?

0

1

2

3

4

5

6

7

8

9

10

Very UnlikelyExtremely Likely

Required

Thank you for your feedback.

Our goal is to create the best possible product, and your thoughts, ideas and suggestions play a major role in helping us identify opportunities to improve.