Sponsored News

SPONSORED: Not sure if your current business account is right for your needs? Use our checklist to find out.

While awareness of personal credit scores has been rising in Australia, business credit scores – yes, there are credit scores for business – are still woefully ignored by Australian small businesses. According to research from MYOB and small business lender OnDeck, 93% of businesses have never accessed their score.

Cameron Poolman, CEO of OnDeck, says the issue is awareness.

"I noticed that when the consumer credit scores became available. At that point, I thought small businesses really didn't know it either and it's just something where there just hasn't been the level of awareness in Australia that there has been, for instance, in the US, where FICO is a well-known score that people know."

CEO - OnDeck

At OnDeck, we're trying to build people's awareness.

But what is a business credit score? What do you do if your score is low? And importantly, how do you find out your score?

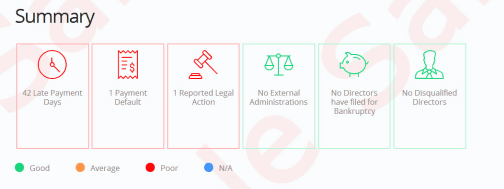

It is a number between 0 and 1,200 that is calculated using the information on your business credit file.

Source: Equifax

According to Poolman, a business credit score doesn't include the personal information that is used to calculate individual credit scores.

Your company's file will contain:

"A business credit score has got more of the commercial information, such as registered defaults, potential loan inquiries or any external administration that may be registered against the business, so it's very much the commercial and business attributes of the business," he said.

However, there are some similarities.

"In the same as in the personal space, without any positive credit reporting, it almost accentuates the negative. And so, it is quite difficult to get to build your credit score up again once you've got a negative listing or your score has dropped because you're not getting that positive reporting coming through to increase it," he said.

Your business credit score is calculated using the information listed on your company credit file. This information includes:

| Response | WA | VIC | SA | QLD | NSW |

|---|---|---|---|---|---|

| I don't have a business | 52.14% | 37.89% | 55.7% | 43.5% | 42.67% |

| No | 37.61% | 51.58% | 36.71% | 46.64% | 46.53% |

| Yes | 10.26% | 10.53% | 7.59% | 9.87% | 10.8% |

Source: Equifax

Business defaults and late or missed payments are some of the main contributing factors to a low score.

"Another way the score could be impacted is just by the quantum of applications for credit that you've made," said Poolman. "So if you are asking for credit from a large quantum of different institutions, that will have a negative impact on your score."

The criteria for business loans, and what information will be considered, varies greatly from lender to lender.

"If it's a secured loan, they're looking at the securities that the person has provided, and that might be over particular assets, it could be the business, or it could be the person's home that they're lending against. What's also important is the cash flow."

"We will look through, in detail, a company's cash flow and determine its ability to service the loan that they're looking to get. Other funders will look at profit and loss statements, balance sheets, tax returns. It's different for different funders."

Poolman's advice to any business that has a low credit score is to order a copy of their business credit report, which they can get for free directly from a credit bureau.

"Once you get that report, you know if it's a default issue. So if I a supplier has defaulted you, you know who it is, and then you could determine whether you're able to settle that issue and then remove that from your file, which will generally increase your score."

If you've found out your business has been flagged as a credit risk, there are a few things you can do to appear as less of a risk to lenders and improve your business's credit score:

You need to pay to receive your business credit score directly from a credit reporting bureau, such as Equifax, but OnDeck allows small businesses to receive their credit score for free.

Get your business credit score from OnDeck

Poolman believes that more and more small businesses will be looking to access their credit score because of its importance when applying for loans.

"I think in time, consumers, as well as small businesses, will become more aware of their credit score because it impacts their ability to access credit."

"We want to be at the forefront of different opportunities to help small businesses. We'd say this is one way of doing it."

Not all credit checks negatively affect your credit score. Lenders do two kinds of checks before approving or denying a business loan application.

Individual and business profiles are subjected to soft pull inquiries everyday without being aware of it. Lenders can do a soft pull check for an overall idea of your financial status before pre-approving your application, or credit bureaus can soft pull your file if you request your credit score.

Soft pull inquiries have no impact on your credit score, but may be noted as a file access.

Hard pull credit inquiries involve an official check of your credit report. When you apply for a car loan, personal loan or home loan and allow a lender to check your credit file, the lender will conduct a hard pull. While soft pull inquiries have zero effect, hard pull checks are listed on your credit file and therefore can affect your credit score.

Every hard pull credit check is listed on your credit report, including which lenders have denied previous applications and how many times you've applied for loans in the past. Too many hard pull inquiries in a short space of time can negatively impact your credit score.

You have to give the lender permission to conduct a hard pull inquiry. Before submitting a loan application, make sure that your business meets all the criteria and has a good chance of being approved. While a hard pull will reflect on your credit report either way, carefully considering your loan options can help avoid adding rejected applications to the list.

If your business has a few outstanding invoices, invoice financing can help improve your cash flow and get access to funds you need. It's a type of business loan that is secured by the unpaid invoices and comes with reduced risk, no asset requirements or interest payments.

Compare invoice financing products below.

We currently don't have that product, but here are others to consider:

How we picked theseWe assess over 150 business loan products for their rates, fees and important features, assigning them a score out of 10.

SPONSORED: Not sure if your current business account is right for your needs? Use our checklist to find out.

The right tools and approaches will help you and your business thrive – these tips and trends can help you find them.

ScotPac’s Boost Business Loan offers simple access to funding, allowing your business to borrow between $10,000 and $500,000.

Whatever your business loan requirement, ebroker may be able to help. With a range of loan options from over 80 bank and non-bank lenders compared on-site, could you find the right loan for your business?

Lumi offers a variety of short-term unsecured tailored business loans for SMEs, so you can find the loan that fits your business goals and your specific company.

Benefit from flexible loan terms and loan amounts through over 80 lenders from Valiant Finance.

Thinking of buying a pharmacy? Check out this guide to choosing the right pharmacy and finding the right pharmacy loan.

Buying a petrol station? Here’s how to find the right business and compare petrol station loans to finance your purchase.

Floorplan finance, also known as inventory finance, provides the funds your business needs to purchase high-value inventory without affecting cash flow.

We’ve covered a wide range of loans you can apply for if you’re a small business in need of finance.

If you're looking for a flexible business finance solution, Prospa has a competitive offering that you can consider. Apply for up to $300,000 online and receive approval within one hour.

Looking to apply for a business loan? This business loan calculator lets you compare the cost of two business loans so you can see which is the one to apply for.