Saving vs stocks: What’s the best way to make money for your kids?

If you were to stick $100 into a savings account or stocks, how much money could you make for your kids in 17 years?

Kids have one major advantage over adults when it comes to saving money: time.

But kids are not the best with money.

Like lots of children, I received pocket money from my parents in return for doing some chores around the house.

Payday occurred once a week. 5 pounds of cold hard cash were deposited onto the kitchen worktop every Saturday, without fail, which was promptly spent by me as quickly as public transport could get me to the shops.

Growing up, there was no real reason to save for the future. My grandparents hadn't encouraged their kids to put money away and things had turned out well enough for them (for one, they bought their first home in their 20s).

Thankfully, there are some signs that financial literacy is improving. More than half (57%) of parents have opened a savings account for their children, according to Finder's Parenting Report.

Most Australians also say they would open their child's first bank account when they were 1, according to a survey we did of 1,000 people. The second most popular ages were 5 and 10.

How much could you save for your kids?

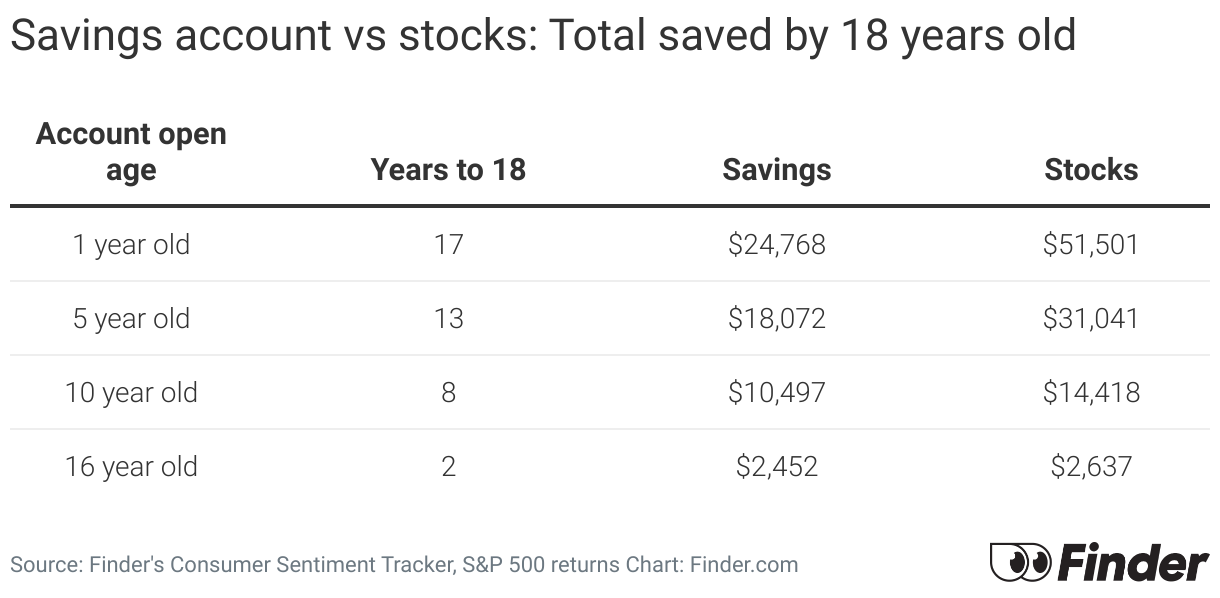

Our question got us thinking: if you were to put money into a savings account or stocks every month from the ages of 1, 5, 10 or 16 (when lots of kids tend to get jobs) until they turn 18, how much money could your children have?

We decided to find out by looking at average rates over the past 20 years.

If you were to stick $100 a month into a savings account for your kid for 17 years, you could have earned them $24,768 before tax.

If you did the same with the stocks, your kid could have earned an impressive $51,501 before tax.

These figures are based on the average savings account rate from Jan 2014-24 and the average return of the S&P 500 over the last 20 years with dividends reinvested before inflation.

There's one catch worth keeping in mind though: tax.

The Australian government may have binned inheritance tax in the late 70s and early 80s (making it easier for kids to inherit their parent's wealth) but they've done less for parents trying to save for their kids now.

For example, kid's bank accounts have a tax-free threshold of $416 per income year but once the threshold is exceeded, interest is taxed at 66%.

How Sarah saves for her three kids

As Gary mentioned, the biggest benefit kids have is one they don't even know or care about: time.

Compounding is the closest thing I know to magic. It allows the smallest of contributions today to add up to very big amounts in the future. And if we're able to plan decades and decades into the future, those amounts can be really substantial.

I have three children and right now, they have one joint bank account. My eldest is 13 so in a few years, I'll split the account into 3 so they each have their own pot.

I've been adding $5 each per week since she was born, and added another $5 when my other two children were born. Today, that account has a little over $12,000 in it, which may not sound super impressive. But if we keep adding $15 per week and the magic of compounding keeps doing its thing, by the time she's 25, the account could be worth around $35,000.

Now, that money needs to be split three ways. And it's not going to be nearly enough to get her a house deposit. But it's a great outcome considering the investment I make is equivalent to a couple of large oat-milk coffees each week.

Keeping funds in a savings account is a super low-risk way to invest. I could supplement this by investing small amounts in ETFs, stocks or a managed fund, which all have different risk profiles but also, the possibility of much higher returns.

They're riskier because there's more chance of markets changing and investment returns dwindling at different times. But, as we said, that's the benefit that kids have over us: time. When you have an investment timeline of a few decades ahead of you, you can ride the waves of poor performance (as you only crystalise those loses if you have to sell or exit).

Our job as parents is to set up the foundations and help them benefit from that extra time in the market, as they don't know how good they've got it!

Looking for more family finance-y stuff? Check out our brand new guide.

Sources

Ask a question