The LMI advantage: How property buyers are unlocking more borrowing power

Purchasing property can be challenging in the current market. But Lenders Mortgage Insurance (LMI) could help you get there sooner.

2026 is here already and property buyers are facing a range of challenges.

- Rising property prices are outpacing savings

- High living cost

- Pressures

- It's getting harder to save.

For those buying property for the first time, it can be difficult to know how to get started.

The Australian Government 5% Deposit Scheme is an option for first home buyers purchasing a home to live in.

But it's not the only way to buy your first home. The scheme has property price limits, which can reduce your choices. Especially in major cities.

But the good news is that there are other options available, including Lenders Mortgage Insurance (LMI). LMI can help you buy sooner with a smaller deposit.

How LMI can help

When buying a home with less than a 20% deposit, your lender may charge LMI.

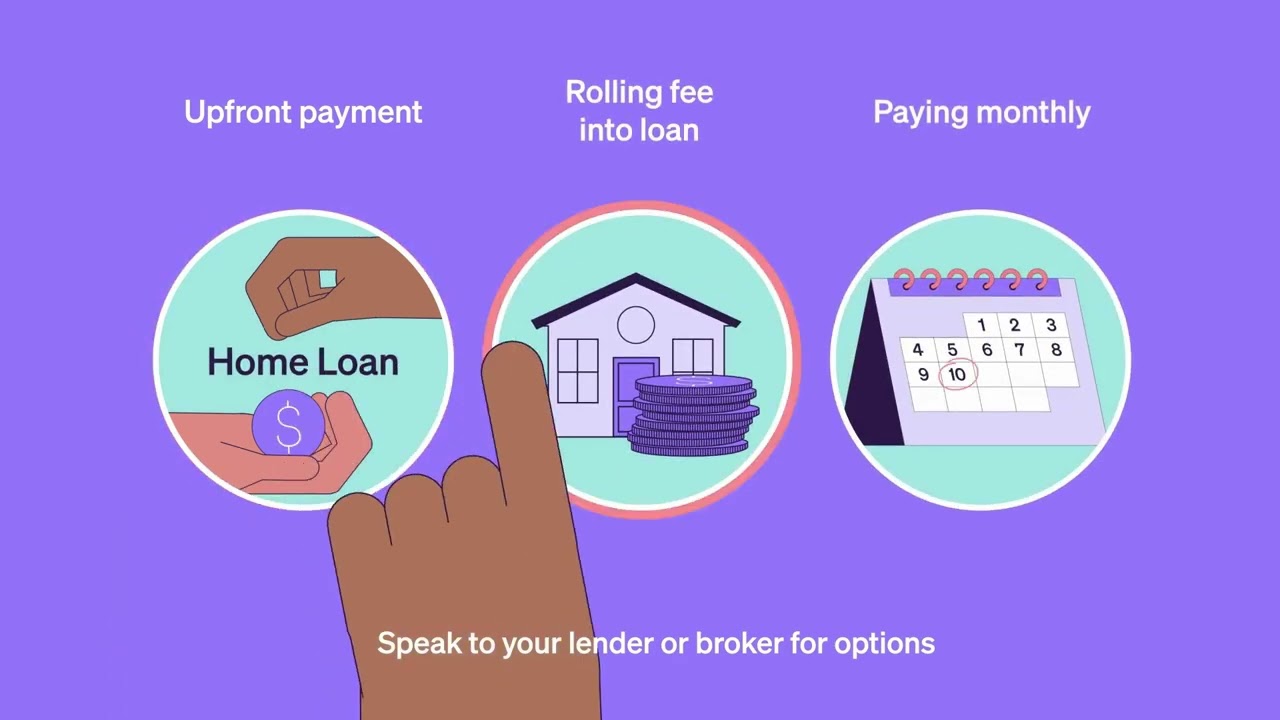

This is usually a one-off cost added to your loan. LMI can be viewed as an additional cost. But in today's property market, many buyers are using it as a way to get into a home sooner, instead of waiting years to save a bigger deposit.

LMI may help you:

- Buy a home with the deposit you have available now

- Increase how much you can borrow

- Buy a bigger, better, longer-term suitable home

We'll take a look at some of the practical ways this can help. But first, we need to consider the numbers.

Balancing your deposit and buying power

Australian property prices continue to rise faster than many people can save for a 20% deposit.

Additionally, high-growth metro areas -- and nearby regional ones have continued to see rising house prices.

For many buyers, saving a full 20% deposit is unrealistic and if you factor in property price limits under the Australian Government 5% Deposit Scheme, this can further limit your options.

So while waiting may suit some buyers, understanding the options available is important to ensure you aren't left chasing rising prices.

Explore how far your deposit could take you with Helia's Home Deposit Estimator.

Let's take a look at a scenario with Mitch and Amelia.

Mitch and Amelia dreamed of owning their own home as they planned to grow their family.

Like many Australians, they found it hard to save a 20% deposit while property prices continued to rise. The home they wanted in Melbourne was above the property price limit for the Australian Government 5% Deposit Scheme.

Their broker explained that LMI could allow them to borrow up to 95% of the property value (subject to satisfying their lender's loan eligibility requirements), helping them buy sooner, instead of waiting years to save a larger deposit.

With help from LMI, Mitch and Amelia were able to:

- Purchase their home 2 years earlier with a deposit less than 20%

- Avoid ongoing rent and financial stress

- Bought in their preferred suburb, reducing the need to move again

LMI in action – equity vs cost

| Year | Property Value | Deposit | Purchase costs (incl. stamp duty) + LMI Fee | Capital Growth (5% pa) | Equity | Return vs LMI cost |

|---|---|---|---|---|---|---|

| Purchase | $1,000,000 | $160,000 | $57,500 + $23,667 | - | $78,833* | - |

| Year 1 | $1,050,000 | - | - | + $50,000 | $128,833 | 5.4 x fee |

| Year 2 | $1,102,500 | - | - | + $52,500 | $181,333 | 7.6 x fee |

*Equity equals deposit minus purchase costs and LMI fee.

Buying earlier helped Mitch and Amelia build $181,333 in equity in two years (over seven times the cost of their LMI fee) while avoiding two more years of rent.

Source: Calculations are indicative only and based on the Helia Home Deposit Estimator. Assumptions include a 30-year loan term and an interest rate of 5.5% p.a. This example is general information only. Estimates are based on information available as at February 2026 and may vary depending on borrower circumstances, account serviceability and lender criteria. This past performance is not indicative of future performance.

Assumptions: 5% annual growth

The key benefits

Using LMI can help increase your borrowing power, giving you more property options as a first-time buyer or investor.

The LMI fee can be added to your loan (capitalised), helping reduce upfront costs. For some buyers, LMI is considered a trade-off to enable entry into the property market sooner.

LMI may help you:

- Buy properties above government scheme property price limits

- Purchase in locations closer to work, schools, family or friends

- Choose a home that suits long-term needs.

Although opting for a "starter" property can have benefits, it can also lead to additional costs if you need to upgrade or move again later.

Buying small and upgrading can lead to doubling up on costs, such as agent fees, stamp duty, legal costs and moving expenses.

The respective costs -- and effort involved -- need to be weighed carefully to help buyers decide which option best suits their personal circumstances in the long term.

As with any major financial decision, buyers should always seek the advice of a professional.

Next steps

If you're thinking about buying a property soon, it's important to consider all your options.

One way to get started is to visit Helia's Home Deposit Estimator.

This can give you an indication of how your current savings can translate into your deposit options and purchasing power.

From there, speak to a mortgage broker or lender to help give you a clear picture of your options and what's right for your circumstances.

Learn more about LMI with Helia

![]() Sponsored by Helia. As a leading provider of Lenders Mortgage Insurance (LMI), Helia makes it easier and faster for home buyers to purchase property. T&Cs apply.

Sponsored by Helia. As a leading provider of Lenders Mortgage Insurance (LMI), Helia makes it easier and faster for home buyers to purchase property. T&Cs apply.

More information about Helia

Disclaimer

Lenders mortgage insurance (LMI) is insurance that protects lender/credit providers, not home buyers, and cannot be provided directly to home buyers. Eligibility criteria, terms, and conditions apply.

The information contained in this article is general information. It does not constitute legal, tax, credit or financial advice, and is not tailored to a home buyers' specific circumstances. Home buyers should consider their own personal circumstances and seek advice from their professional advisers before making any decisions that may impact their financial position. Any references to reports or data are provided for general information only and may not apply to your circumstances.

The information is current as at the date of publication but may change without notice. We are under no obligation to update the information or correct any inaccuracy which may become apparent later. We do not take any responsibility for any reliance on the information contained in this course or for its reliability, accuracy, or completeness.

Helia Insurance Pty Limited's ('Helia') does not provide or engage in credit activities as a credit provider, except for limited credit activities engaged by it as an assignee in relation to providing LMI products or as a credit provider under the doctrine of subrogation in relation to providing LMI products. The information provided in this article does not refer to a credit contract with any particular credit provider.

Image: Source not specified