OFFER

Swyftx Cryptocurrency Exchange

- 310+ cryptocurrencies

- Fast online ID verification & deposits

- Low fees and spreads

- Demo Mode for beginner traders

- Live chat support available 7 days/week

Swyftx Cryptocurrency Exchange

You can use the chart below to track the live price of XRP in Australian dollars and see how it has performed over time.

| Ticker symbol | XRP |

|---|---|

| Use | Cross-border Payments |

| Year released | 2012 |

| Origin | United States |

| Maximum supply | 100,000,000,000 |

| Consensus algorithm | Proof of Correctness |

| Notable team members | Brad Garlinghouse, David Schwartz, Stefan Thomas |

| Notable partnerships | Accenture, American Express, Deloitte, Royal Bank of Canada, MoneyGram, National Australia Bank, Western Union, Westpac |

| Mineable? | No |

Launched in 2012, XRP is now one of the world's largest cryptocurrencies.

It aims to offer fast, affordable and reliable cross-border payments.

Both XRP and the XRP Ledger were created by US technology company Ripple, which develops a range of solutions designed to transform the global payment industry.

"The revolution of blockchain is not going to happen from outside the system; it's going to happen from within the system."

- Brad Garlinghouse, Ripple CEO

The XRP network is designed to allow users – primarily financial institutions – to transfer money from any currency to any other currency in a matter of seconds, anywhere in the world. This is an ambitious goal meant to eliminate the need for older systems like SWIFT.

Ripple (also known as Ripple Labs) is a San Francisco-based technology company with more than 300 employees, focused on providing cross-border payment solutions.

It is the company that created and manages the XRP currency and network.

Ripple's main aim is to create a global settlement network that ensures more efficient transactions between the world's financial institutions.

This is a breakdown of the different components that make up the XRP and Ripple platform:

XRP is the name of the digital currency that facilitates transactions on the Ripple network. It effectively acts as a bridge between the two currencies being transferred, and also serves as a source of liquidity when necessary.

XRP is the native asset of the XRP Ledger, an open-source blockchain that runs on a network of peer-to-peer servers.

XRP Ledger (also known as XRPL) is the blockchain network that underpins the XRP ecosystem. Ripple transactions are recorded on XRP Ledger and processed and confirmed by a group of validators.

The ledger uses its own Ripple Consensus Protocol Algorithm (RCPA), which governs how validators manage the XRPL network. All transactions need to be verified by at least 80% of validator nodes before they are confirmed.

This is Ripple's network of payment providers around the world. It connects the different payment networks of banks, payment providers, digital asset exchanges and corporate entities, and can accept both fiat and cryptocurrencies.

This is the American technology company that develops the Ripple payment protocol and network. Originally known as OpenCoin, it later traded as Ripple Labs.

XRP is designed to allow fast borderless transactions and improve the process of international payments. It connect banks and payment providers to provide real-time settlements with low transaction costs.

Current methods of sending money internationally are outdated and slow.

This is best summed up in this excerpt from Ripple's cost model paper2:

"Today's global payments infrastructure moves money from one payment system to another through a series of internal book transfers across financial institutions. Because these book transfers occur across different systems with a low level of coordination, funds settlement is slow (often 3-5 days, trapping liquidity), error-prone (error rates run upwards of 12.7%), and costly ($1.6 trillion in system-wide costs for global cross-border transactions)."

Despite the fact that the global remittances industry is huge, there's currently no streamlined and well-organised international network to handle cross-border payments.

This is the problem Ripple aims to solve.

However, rather than going toe-to-toe in competition with the banking Goliaths that currently control this sector, Ripple's plan is to partner with major financials around the world to offer a blockchain-based solution.

By joining Ripple's global network, Ripple says that financial institutions can process their customers' payments anywhere in the world instantly, reliably and cost-effectively.

Let's say Bank A in Australia wants to send $5 million to Bank B in Bangladesh. Rather than converting Australian dollars to Bangladeshi taka, battling exchange rate margins, paying processing fees and facing slow transaction times along the way, Bank A can transfer $5 million worth of XRP to Bank B's Ripple wallet, which can then be converted to the local currency.

Payments using XRP settle in four seconds, and the current minimum transaction cost required by the network for a standard transaction is 0.00001 XRP. The network is also currently capable of consistently handling 1,500 transactions per second.

There are a total of 100 billion XRP tokens in existence, all of which were created when the project launched. This is known as a "pre-mine", and is different to other cryptocurrencies like Bitcoin, where the total supply is unlocked over time in a process known as "mining".

While there are 100 billion total XRP tokens, only around 57.8 billion are currently unlocked, with the rest held in escrow by the Ripple team.

This is because Ripple, the company behind the cryptocurrency, owns some 60% of the total supply of XRP. Most of Ripple's holdings (around 55 billion XRP) are locked in an escrow account, with up to 1 billion XRP to be released every month for a period of 55 months.

Of the 1 billion XRP released each month, any unused amounts are put back into escrow and will be re-released in the first month that there are no other XRP releases. Essentially, the unused amounts are sent to the back of the queue.

XRP is also deflationary. While the total XRP supply started off at 100 billion (100,000,000,000), around 13.5 million have been burned.

That's because XRP is a deflationary currency, with every transaction incurring a small fee (to prevent spam attacks) which is destroyed during the transaction.

The minimum fee for each XRP transaction is 0.00001 XRP (also known as 10 drops, or a fraction of a cent), although certain movements such as multi-signature transactions, or escrow transactions, will incur higher fees.

Since its inception, this means around 1 million XRP are burned a year on average.

Even with generous predictions of XRP uptake it's estimated that it would take thousands of years for circulating numbers to get low enough to start being a concern. Plus, XRP can be divided into individual drops (0.000001 XRP) if needed.

The fees and therefore the burn rate can also be modified by consensus at a later date.

In the immediate future, the real circulating supply of XRP will actually be increasing much more quickly than it's decreasing as Ripple releases XRP from its escrow account.

In December 2020, the Securities and Exchanges Commission (SEC) filed a lawsuit against Ripple and two of its executives.

According to the SEC press release, "The complaint alleges that Ripple raised funds, beginning in 2013, through the sale of digital assets known as XRP in an unregistered securities offering to investors in the U.S. and worldwide."3

Ripple filed a 93-page response to the lawsuit in January 2021, stating that "XRP performs a number of functions that are distinct from the functions of "securities" as the law has understood that term for decades. For example, XRP functions as a medium of exchange — a virtual currency used today in international and domestic transactions — moving value between jurisdictions and facilitating transactions."

The XRP blockchain works differently to Bitcoin, Ethereum and most others, and has often been criticised as being not truly decentralised.

The point of decentralisation in this context is primarily to ensure that it's impossible to interfere with the network by blocking or reversing transactions, sending money you don't have and similar.

If one entity manages to take control of a large enough part of the network, or if a sufficient number of participants collude to attack the network, they might be able to interfere with the network in these kinds of ways.

One of the reasons XRP Ledger is so fast compared to Bitcoin and other public blockchains is essentially because it depends on that tighter and faster set of "trusted nodes" to do the heavy lifting. These nodes can be found on Ripple's Unique Node List. Getting a spot on that list means publicly identifying and verifying oneself to the world.

It's mostly businesses and other well-known entities that operate validating nodes. At various points, Microsoft, MIT and other institutions have operated trusted nodes.

The reason this system has drawn so much criticism is because one of the big points of a blockchain is that you don't have to trust anyone, and can instead just trust the system.

So, the main question to ask if you're wondering whether XRP Ledger is sufficiently decentralised to be safe, might be:

Can trusted nodes be trusted?

Yes and no. You naturally can't trust any individual node, but you don't have to.

In this case, "trusted" doesn't mean that every single node needs to be honest. Rather, it just means that they can be trusted not to collude with each other for the purpose of interfering with the XRP Ledger.

The collusion threshold needed to attack the ledger depends on what they want to accomplish. This is because a supermajority of nodes (80%) need to approve a transaction before it can go through.

What this means is:

At the same time, any trusted nodes which want to abuse that trust will likely have to do so publicly and under their own name.

Firstly, this might indicate that Ripple is serious about not wanting to give anyone – even itself – too much power over the XRP Ledger, and that it's been taking consistent steps to that end.

And secondly, that particular balance means that even if literally every other trusted validator tried to attack the network, they wouldn't be able to get the supermajority needed to falsify transactions. The only thing they'd be able to do is block the network temporarily, ruining their own reputations for no clear gain.

Conversely, Ripple doesn't have enough node control to unilaterally do anything either, except refuse transactions.

Plus, the Unique Node List is just a set of recommendations put forward by Ripple to keep everyone on the same page and make things easier. Even if Ripple itself were to go rogue and block the XRP Ledger, the other node operators could theoretically keep things flowing by each cutting those misbehaving nodes out of their own personal trusted node lists.

"If Ripple as a company went away, XRP would continue to trade. To me, that's the definition of decentralisation." - Ripple CEO Brad Garlinghouse

So, although it may not be decentralised in the same way Bitcoin or other cryptocurrencies are, XRP Ledger might be sufficiently decentralised for its intended applications.

It's worth noting that Ripple's 27% majority node control, with an 80% supermajority required for takeover, and failsafes in the event of a takeover attempt, means that XRP is functionally much more decentralised than Bitcoin. Bitcoin only has a 51% threshold for takeover, already has individual mining firms controlling way more than 27% of the network, and has no failsafes in the event of a takeover attempt.

Ripple, the San Francisco-based fintech company behind XRP, was founded in 2012.

Though the project has roots dating back to 2004, it wasn't until Jed McCaleb and Chris Larsen joined forces in August 2012 that the Ripple we know today truly began to take shape.

Today, Ripple is led by CEO Brad Garlinghouse and notable team members like chief cryptographer David Schwartz and CTO Stefan Thomas.

The biggest obstacle to Ripple's quest for global domination is the adoption (or lack thereof) of XRP by banks and financial institutions around the world, and that's where the focus of the people behind Ripple might be.

If more banks join the network, this could encourage demand for XRP and entice other banks to join the platform, but Ripple may also face stiff competition from Stellar.

And that's before we even get to the established players in this space. Ripple needs to not only outperform other blockchain payment solutions, but also needs to be an improvement on the in-house blockchain creations being trialled by financial institutions around the world.

SWIFT currently connects more than 11,000 of the world's financial institutions through its own network, and has been working on its own trials of blockchain technology. Credit card giant Visa is exploring its own blockchain-based cross-border payment options, so Ripple won't be able to just waltz in and take a big chunk of market share without a fight.

There are also ongoing questions about the role of XRP within the Ripple ecosystem. Usage and network effects might drive price actions to a large extent, but this may not translate into higher prices as directly as one might expect. Trillions of dollars are crossing borders each year, but it's still not clear how much market cap XRP needs to adequately service the industry.

The XRP Ledger's construction and design choices have also attracted some criticism.

This guide provides step-by-step instructions on how to buy SPX6900, lists some exchanges where you can get it and provides daily price data on SPX.

This guide provides step-by-step instructions on how to buy Conflux, lists some exchanges where you can get it and provides daily price data on CFX.

This guide provides step-by-step instructions on how to buy Monero, lists some exchanges where you can get it and provides daily price data on XMR.

How to buy Bitcoin SV (BSV) in

Australia

This guide provides step-by-step instructions on how to buy Fantom, lists some exchanges where you can get it and provides daily price data on FTM.

A panel of industry specialists give us their predictions on the price of shiba inu to 2035.

Learn how to buy Shiba Inu in Australia with our simple step-by-step guide and tips on what to know before you get started.

Learn how to buy Dogecoin in Australia with our simple step-by-step guide and tips on what to know before you get started.

Learn how to buy in with our simple step-by-step guide and tips on what to know before you get started.

This guide provides step-by-step instructions on how to buy MATIC (migrated to POL), lists some exchanges where you can get it and provides daily price data on MATIC.

Hi there, how do i purchase ripple using cash? Do I go to an accredited australian post office (just like when buying bitcoin)? I do not want to pay via paypal or fund transfer hence, my question. Thanks, Neil

Hi Neil,

Thanks for your inquiry

This will depend on the exchange you have chosen to buy XRP from. Please contact the exchange’s support for clarification about this.

Hope this information helps

Cheers,

Arnold

Hello

I am a newbie at this ………I have XRP sat on two exchanges BTC and Etoro – should I move them into a wallet ?..or is it OK to leave them on the exchange?

Many Thanks

Hi Mike,

The answer to your question will depend on your intention. If you are not considering trading your cryptocurrency just yet, then the safest thing to do is always to withdraw your coins to a wallet.

You may compare cryptocurrency wallets that you can use for the purpose of saving your coins. Ledger Nano is one that supports XRP. Once you have chosen a particular wallet, you may then click on the “Go to site” button to be redirected to their website where you sign up or get in touch with their representatives for further assistance.

I hope this helps.

Cheers,

Anndy

I am having trouble finding a suitable wallet to use for Ripple. Do you have any suggestions?

Hi Alissa,

Thanks for your inquiry.

Ripple wallets require you to have 20XRP to book your wallet address. So if you add 1000 XRP to your Ripple wallet, 20XRP will be used to book the wallet address. This is one reason you don’t want to use multiple wallets for XRP (unless required).

Pick the right wallet from day one so that you don’t end up losing 20XRP on various wallet addresses.

Your first option is Ledger Nano S it is a hardware wallet that has recently added support for XRP.

Being a hardware wallet, it is one of the best ways to store your cryptocurrency as it offers great security, ease of use, and you can carry it with you anywhere.

The second option is Binance. It is not a wallet. It is a fast-growing exchange that started in the mid of 2017 year and is rapidly adopting many new cryptocurrencies for its users. If you want to get XRP right now, you can use Binance to get an XRP wallet.

However, you should not store your XRP for more than 1-2 days on an exchange (any exchange) as exchanges can shut down or go into issues at any time and put you at risk of losing your stored coins.

Hope this information helps

Cheers,

Arnold

Hi.. I am looking for the cheapest way to buy into ripple either by bank transfer or poli. Can you recommend a platform with low fees to trade please.

Hi Joe,

Thank you for your inquiry.

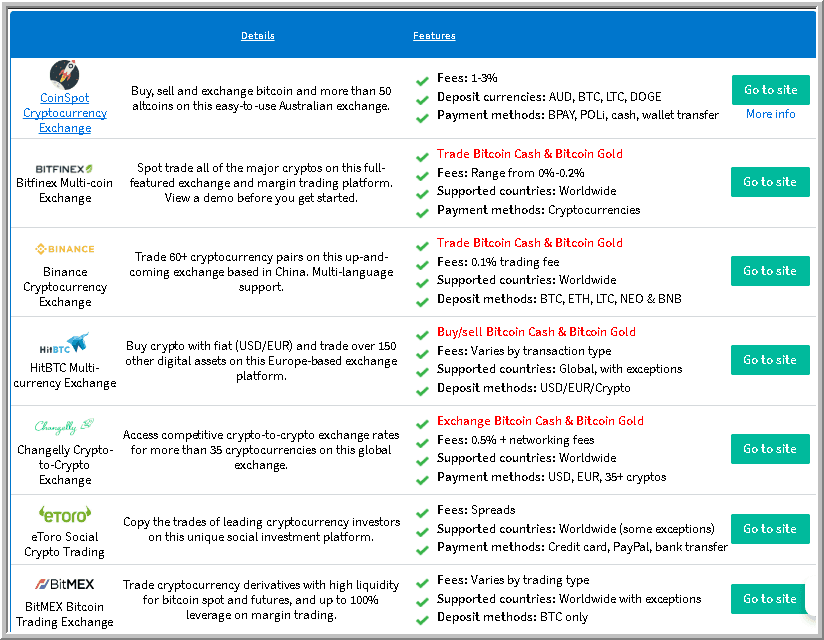

As per checking you are already on the right page. What you can do next is to compare the available options that will best fit your personal requirements. You can check the list of Ripple brokers and Ripple exchanges on the table provided above.

I hope this information has helped.

Cheers,

Harold