- Bessie Hassan

- Head of PR & Money Expert

- finder.com.au

- +61 402 567 568

- Bessie.Hassan@finder.com.au

Media Release

RBA survey: Experts on the fence about “honeymoon” rates for mortgage holders – September, 2018

- Today represents the 25th consecutive month since a cash rate movement

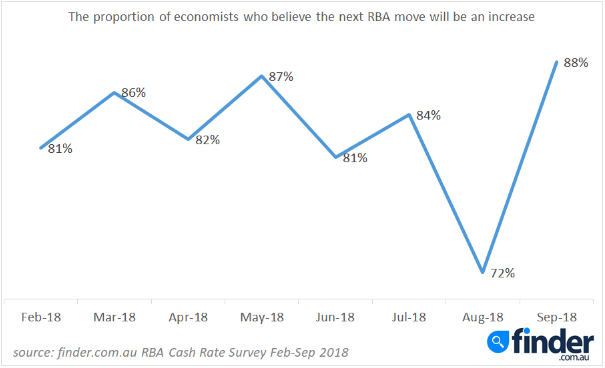

- 88% of panellists expect the next cash rate move will be in an upward direction

- Experts divided about “honeymoon” rates for home loan borrowers

4 September, 2018, Sydney, Australia – Today marks the twenty-fifth consecutive month since a cash rate movement, with all 30 members from the finder.com.au RBA survey accurately predicting the Reserve Bank’s decision to pause the cash rate this afternoon.

Expectation of a rising cash rate is at the strongest level this year, with 88% of panellists forecasting the next move to be in an upwards direction.

When it came to the timing of the next rise, there were eight predictions (38%) for a rise in the second quarter (April - June) of 2019, and five (24%) for the fourth quarter (October - December) of 2019. Four economists (19%) predicted the rise to hold off until 2020.

Graham Cooke, Insights Manager at finder.com.au, said the cash rate is likely to remain at 1.5% for the remainder of the year, and part of 2019.

“There are now very few predictions for a rise before the second quarter of 2019.

“It’s widely believed the cash rate will remain stagnant for some time now, but this hasn’t stopped lenders from lifting rates independently of the Reserve Bank, which we witnessed late last week.

“Westpac and Suncorp were among the first banks to increase home loan rates in response to offshore funding pressures, and many are keeping an eagle eye on the market for further announcements to come,” he said.

When asked about temporary low rates on home loans, otherwise known as “honeymoon” rates, experts and economists were divided.

Seven respondents (41%) felt honeymoon rates were bad for borrowers, with the majority of this group indicating such offers encourage customers to take on more debt than they can afford.

On the other hand, seven other economists (41%) felt honeymoon rates were good for consumers, with the majority favouring cost savings.

Three economists (18%) were on the fence about introductory rates, including Mark Crosby from Monash University who said; “[It] depends whether borrowers have the capacity to make additional repayments in these early years. If so [honeymoon rate loans] are a very good deal.”

Cooke said honeymoon rates can be useful for borrowers as long as they understood the terms involved.

“Often the honeymoon rate is one percentage point below the standard rate, which is why honeymoon rates can be suitable for first home buyers looking to keep their repayments down within the introductory period.

“Honeymoon rates can be a great way for first home buyers to get a foot on the ladder, but they need to be prepared for higher interest costs once the temporary rate expires.

“As we expect some rate rises over the next two years, borrowers need to be comfortable with paying a rate that’s at least two percentage points higher than their current revert rate,” he said.

You can compare honeymoon rate home loans on this page: https://www.finder.com.au/home-loans/honeymoon-rate-home-loans.

Here’s what our experts had to say:

Jordan Eliseo, ABC Bullion: "The RBA will hold interest rates at 1.50% at their next meeting, continuing a run of stability that now dates back over 2 years. Consumer confidence has been hit by the recent political chaos in Canberra, and job growth in the economy will likely slow down in the lead up to the next election, but the RBA is still reticent to cut, despite numerous headwinds the economy is facing."

Tim Nelson, AGL Energy: "RBA has stated that it continues to expect inflation to be around 2¼ per cent over the next couple of years as above-trend GDP growth reduces spare capacity in the labour market and there is an associated pick-up in wages growth."

Shane Oliver, AMP Capital: "While economic growth picked up a notch in the first half of the year its premature to start raising rates as uncertainty remains around the outlook for consumer spending, the housing cycle both in terms of construction and home prices has now turned down, and wages growth and inflation remain low. So remaining on hold makes sense and this is likely to remain the case for some time to come."

Alison Booth, ANU: "Fundamentals have not changed sufficiently to warrant changing the cash rate."

Richard Robinson, BIS Oxford Economics: "inflation and wages growth is low."

Paul Dales, Capital Economics: "The RBA is patiently waiting to see if the unemployment rate falls as it is hoping and inflation rises back to the 2-3% target rate. I suspect it will be waiting for a long time yet."

Saul Eslake, Corinna Economic Advisory: "The RBA has made it clear that although it thinks the next move in interest rates will most likely be up, it is in no hurry to act on that inclination. And nothing has happened since the last meeting to have prompted them to change that view."

Peter Gilmore, Gateway Bank: "The economic fundamentals remain largely unchanged."

Mark Brimble, Griffith Uni: "No reason to move with inherent weakness in the economy exacerbated by political and regulatory uncertainty both domestically and internationally."

Peter Haller, Heritage Bank: "There is no reason for the RBA to change rates at the present time."

Paul Bloxham, HSBC Bank Australia Limited: "Inflation is still below the target band."

Alex Joiner, IFM Investors: "The RBA finds itself between a rock and a hard place, the economy does not as yet justify higher policy rates, but equally it can not foster any better conditions that might see inflation accelerate more quickly because of the financial stability constraints it has, rightly in my view, it has also chosen to focus on."

Michael Witts, ING Bank: "Despite the increase in mortgage rates from one of the majors, this is unlikely to alter the RBA stance."

Leanne Pilkington, Laing+Simmons: "There’s no compelling reason for the RBA to adjust the official cash rate at this time. Of greater interest is the approach the banks are taking with their lending terms. Some are cutting fixed rates in an attempt to build market share. Honeymoon interest rate deals are in vogue to attract first home buyer attention, but it’s necessary to crunch repayment numbers based on the actual rate you’ll be paying once the honeymoon is over. There’s significant rate movement irrespective of the RBA at the moment."

Nicholas Gruen, Lateral Economics: "That's what they keep saying they'll do."

Mathew Tiller, LJ Hooker: "No major changes to economic conditions over the past months will see RBA hold the cash rate steady. In addition banks and lenders continue to change their interest rates independently of the RBA."

Michael Yardney, Metropole Property Strategists: "There is no reason to alter interest rates. Our weakening housing markets, low inflation rate and soft wages growth suggest no rise in rates is imminent in the medium term. If anything this would dampen already sluggish consumer confidence which has already taken a hit over the last month."

Mark Crosby, Monash University: "The RBA has signalled its intent to hold rates for some months yet, though it is good to see some discussion about whether the current inflation target remains appropriate."

Dr Andrew Wilson, My Housing Market: "Macro environment relatively unchanged although out of cycle rate rises will be closely monitored by RBA if the level of increases impacts already constrained consumption."

Alan Oster, NAB: "The RBA has stated that for the time being, they wish to be a source of stability and confidence in the economy. Rates are low and supporting economic growth which should see employment continue to grow and the unemployment rate decline further. At present there appears to be some degree of spare capacity in the labour market with relatively weak wages growth and inflation only just around the bottom of the RBA’s target band. The RBA is likely to continue this on this track until it is convinced spare capacity has fallen, wages growth is lifting and inflation rising more generally. This is only expected to occur gradually."

Jonathan Chancellor, Property Observer: "The central bank doesn't need to make any move."

Matthew Peter, QIC: "While the RBA is clearly on hold for the time being, the market is not pricing a rate hike until 2020. But with growth picking up, the labour market tightening and the AUD heading to US70c, the RBA will surprise markets with a rate hike, probably as soon as the June quarter of 2019."

Noel Whittaker, QUT: "No reason to move either way."

Nerida Conisbee, REA Group: "The next move is still likely to be an increase but for now, the economy is not strong enough to start increasing."

Christine Williams, Smarter Property Investing Pty Ltd: "We have had a positive effect re unemployment, now under 6% together with a strong outlook in the job sector, both with full time and part time positions. I feel this needs to stay on an upward trend [for] least 1 more quarter before the Reserve Bank increases rates."

Janu Chan, St.George Bank: "Ongoing low inflation and expectations it will stay low for some time allows the RBA room to leave rates on hold."

Brian Parker, Sunsuper: "Still plenty of labour market slack, and wage and price inflation not picking up anywhere near fast enough to prompt higher rates."

Richard Holden, UNSW: "They should cut but they can't. [the] labor market is weak. Inflation is low."

Clement Tisdell, UQ-School of Economics: "The Australian economy is not overheated. Demand pull inflation is not at work. Cost push could become a problem. Private interest rates are liable to increase."

Other participants: Bill Evans, Westpac.

###

For further information

- Bessie Hassan

- Head of PR & Money Expert

- finder.com.au

- +61 402 567 568

- Bessie.Hassan@finder.com.au

Disclaimer

The information in this release is accurate as of the date published, but rates, fees and other product features may have changed. Please see updated product information on finder.com.au's review pages for the current correct values.

About Finder

Every month 2.6 million unique visitors turn to Finder to save money and time, and to make important life choices. We compare virtually everything from credit cards, phone plans, health insurance, travel deals and much more.

Our free service is 100% independently-owned by three Australians: Fred Schebesta, Frank Restuccia and Jeremy Cabral. Since launching in 2006, Finder has helped Aussies find what they need from 1,800+ brands across 100+ categories.

We continue to expand and launch around the globe, and now have offices in Australia, the United States, the United Kingdom, Canada, Poland and the Philippines. For further information visit www.finder.com.au.

12.6 million average unique monthly audience (June- September 2019), Nielsen Digital Panel