- Bessie Hassan

- Head of PR & Money Expert

- finder.com.au

- +61 402 567 568

- Bessie.Hassan@finder.com.au

Media Release

RBA Survey: Will the big four banks bounce back?

- 1 in 3 experts predict Royal Commission to result in fewer home loans with big banks

- Today represents the 28th consecutive time the RBA has held the cash rate at 1.5%

- 75% of experts predict a rate cut as next RBA move

5 March 2019, Sydney, Australia -

Home lending with smaller players will continue to gain momentum as borrowers increasingly turn away from the big four banks following fallout from the Royal Commission, according to Finder, Australia's most visited comparison site.

When asked whether the post-Banking-Royal-Commission environment could result in more borrowers turning away from the big four banks for home loans in this month's Finder RBA Cash Rate Survey, 33% of experts (6/18) said we'll see home loans with the big four decline.

Graham Cooke, insights manager at Finder, said the impact could be far-reaching.

"A third of our experts think that consumers will move away from the big four due to trust issues and stricter lending conditions.

"As a result, what we can expect to see is more borrowers turning to smaller and online lenders, which typically offer lower rates to lure in new customers. They often also tend to have easy-to-use platforms which can mean faster application and approval, lower fees and more personalised customer service than larger lenders.

"Some of the poor behaviour detailed in the Royal Commission may actually lead more consumers to think twice about the big guys," Cooke said.

Cooke said despite the Royal Commission findings, the home loan market is great for buyers with house prices easing.

"With house prices tumbling, and rates at all-time lows, the outlook for housing affordability is strong.

"It's a great time for borrowers to consider their options and get a good deal. Remember, these days if your rate doesn't have a 3 in front of it, you could be doing better," he said.

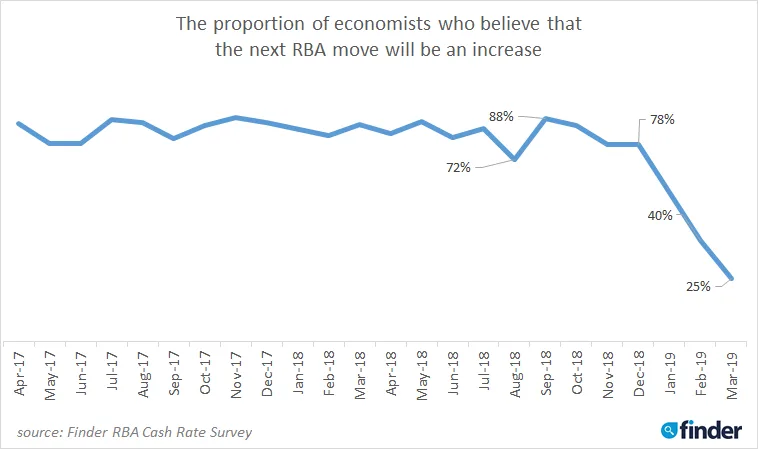

Cash rate holds, but cut looming

The Reserve Bank of Australia (RBA) today announced a hold on the cash rate at 1.5% for the 28th consecutive time, an outcome accurately predicted by all 31 members from the Finder RBA Cash Rate Survey.

In December, 78% (21/32) of experts predicted the next move would be a hike and in January 40% (11/28) predicted a hike.

Cooke said August and November were the most popular months for a forecasted cut to occur.

"Last month, I said the drop to 40% (of economists who believe the next rate move will be upwards) was the most dramatic I had seen in four years of running this survey. This month, that drama is elevated with just one in four believing this to be the case.

"With the housing market continuing to tumble, and other global and international economic factors looking grim, experts seem to be sure we're looking at at least one cut in 2019, if not two," Cooke said.

In the survey, some experts (9/17) forecasted the cash rate would drop to 1.00% before the year is out.

Nicholas Frappell, general manager from ABC Bullion was not surprised by the hold decision.

"Chances of a cut have grown, but the domestic outlook remains reasonably good employment wise and so far consumer spending remains okay despite sinking property prices on the east coast," Frappell said.

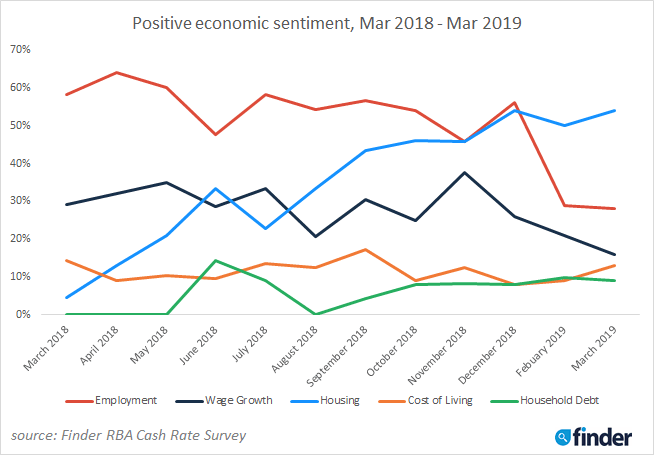

Shift in economic sentiment

Finder's Economic Sentiment Tracker, which gauges five key indicators – housing affordability, employment, wage growth, cost of living and household debt – has also seen a significant shift.

Introduced in March 2018, this month's tracker set three all-time marks, one positive and two negative.

Positive economic sentiment in housing affordability reached its highest level recorded, while positive sentiment for employment and wage growth dropped to their lowest levels.

Cooke said the economic sentiment and rate cut predictions signal good news for would-be mortgage holders, but a different story for savers.

Here's what our experts had to say:

Nicholas Frappell, ABC Bullion: "Chances of a cut have grown, but the domestic outlook remains reasonably good employment wise and so far consumer spending remains okay despite sinking property prices on the east coast."

Shane Oliver, AMP Capital: "Things aren't yet weak enough to push the RBA to cut but they aren't strong enough to push it to hike either."

Alison Booth, ANU: "The fundamentals do not warrant any rate changes."

John Hewson, ANU: "Insufficient evidence yet of a slowing economy."

Malcolm Wood, Baillieu: "Labour market still robust; inflation below target."

Tim Moore, CUA: "On the balance of the economic data in Australia, the RBA have clearly communicated that the risks are balanced therefore the trajectory of the cash rate from here will depend on how both downside and upside risks play out with the key hurdle to a rate cut being employment and inflation. I expect neither cash rate move in the near term."

Trent Wiltshire, Domain: "The RBA has stated the outlook for the cash rate is more balanced, rather than the hiking bias seen throughout 2018. But the RBA is still keen to avoid cutting rates, so will keep the cash rate on hold."

Debra Landgrebe, Gateway Bank: "This is a watching brief, as GDP growth is slower than expected, unemployment is expected to tick up, despite the January jobs report being stronger than expected. This means that quantitative easing may be required. GDP growth is feeling the effect of property prices falling and low wage growth, which is dampening consumer spending more than expected."

Mark Brimble, Griffith Uni: "Bias is moving toward rate reduction, and while there is a case for this in my view, the RBA is likely to want to hold position for now."

Peter Haller, Heritage Bank: "The RBA has clearly stated it is on hold for the time being."

Tim Reardon, Housing Industry Association: "Insufficient data to conclude that the poor results from end 2018 will be long lived."

Alex Joiner, IFM Investors: "The RBA emphasised that it does not think it will need to move on rates, in either direction, in the short term. I'd agree with this sentiment. While some indicators have softened, importantly the labour market has held up well and while this continues to be the case, the RBA has time to assess the remainder of the economy and wait for the better wages and inflation metrics it desires to emerge."

Michael Witts, ING: "Their recent comments suggest the outlook for rates is finely balanced."

Peter Boehm, KVB Kunlun: "The overall direction of interest rates appears to be at a crossroads. For now, I expect rates to stay on hold but recent mixed economic data (in particular the slowing of the housing market) not to mention what's happening internationally (political unrest, trade wars, strains on international relationships) is adding a fair degree of volatility to the economic and financial landscape, which may well last during the course of 2019. For this reason, the RBA may take a conservative approach to rate setting, erring on the side of caution. This caution may manifest itself in a rate drop, meaning, in part, the economy is not as solid as we would like. The next couple of months, leading up to the general election, will be telling."

Leanne Pilkington, Laing+Simmons: "There's somewhat of a stand-off in the housing market at the moment. The level of buyer interest is encouraging but reduced accessibility to finance is having a dampening impact on transactional activity. While this issue runs deeper than merely the cost of finance, a hold pattern remains the prudent course for the RBA in the current climate."

Nicholas Gruen, Lateral Economics: "The bank will see no need to move."

Mathew Tiller, LJ Hooker: "Despite a deterioration in the outlook for the Australian and global economies, recent employment data shows that there are some economic bright spots. This means it remains too early for the RBA to shift rates just yet."

John Caelli, ME Bank: "The Reserve Bank recently moved their interest rate outlook to neutral territory, so it is likely they will hold rates for the near future. With growth and inflation forecasts downgraded, the focus will be on the housing market and unemployment for signs of stress."

Michael Yardney, Metropole Property Strategists: "The RBA has acknowledged that our economy is weaker and the likelihood that the next movement in rates is down. However, it is hoping for employment growth to buoy our economy and it is likely to wait a month or two and see how our property markets are faring before acting."

Mark Crosby, Monash University: "RBA held off raising rates with house prices rising for 3 years. It would be staggering if they cut after 12 months of falls, given a generally stable economy."

Jacqueline Dearle, Mortgage Choice: "I predict the RBA to hold the rate in March and beyond until it has a better handle on what's really happening locally with consumers and because there are no major external drivers, such as the Fed, to shift. In February, the Fed left the key interest rate unchanged and said it would be patient in the face of a mounting set of risks, including slowing growth in China and Europe, Brexit, ongoing trade negotiations and the effects of the five-week U.S. government shutdown. Back in Australia, the RBA's prediction of 3% economic growth this year (and 2.75% growth next year), may be too optimistic, say some economists. Softer growth numbers mean higher unemployment, which would suggest a rate cut down the track. The RBA will be keeping a keen eye on the housing market, especially the key markets of Sydney and Melbourne. With the housing adjustment threatening to spill over into the wider economy, the (negative) wealth effect may increase consumer desire to save and curb consumer spending, which in turn impacts retail and the wider economy. As we have seen this month, there are a lot of moving parts with the Australian dollar, which is sensitive to global economic uncertainties. Looking ahead, we will ideally see credit flow to borrowers to support the housing market, an increase in residential construction, and property investors encouraged to get back into the market."

Dr Andrew Wilson, My Housing Market: "Waiting for December quarter GDP data to be released March 6. If there is another weaker than expected result, the odds will narrow for a pre-Budget, pre Federal Election cut in April or May. Although recent wage data was reasonable (not good, not bad), RBA has conditioned the market to now expect a long-needed cut. This cut will attempt to revive consumption, which is now likely to also be impacted by continuing weaker housing markets."

Alan Oster, NAB: "RBA still watching the economy, the consumer and wages."

Andrew Reeve-Parker, NW Advice Pty Limited: "Sufficient economic activity is balancing housing market concerns."

Jonathan Chancellor, Property Observer: "Holding is the bank's inclination."

Noel Whittaker, QUT: "There is no way they will raise them and a drop would be premature."

Nerida Conisbee, REA Group: "Although the case is building for the next move to be a cut, I think that on balance, the data coming out is still too mixed. Unemployment is still very low even though we are still not seeing this flow through to consumer sentiment."

Janu Chan, St. George Bank: "The RBA has recently shifted toward a more neutral stance, and acknowledged that downside risks have increased. It however, is maintaining its central view that the unemployment rate will gradually fall. While the debate has shifted away from the next move being a hike, the RBA doesn't appear to be ready to cut rates either. "

Clement Allan Tisdell, The University of Queensland: "Comments of the Governor of the RBA lead me to believe the cash rate will be held."

Richard Holden, UNSW: "[The RBA is] waiting for new inflation numbers before they make a move."

Other participants: Bill Evans, Westpac.

###

For further information

- Bessie Hassan

- Head of PR & Money Expert

- finder.com.au

- +61 402 567 568

- Bessie.Hassan@finder.com.au

Disclaimer

The information in this release is accurate as of the date published, but rates, fees and other product features may have changed. Please see updated product information on finder.com.au's review pages for the current correct values.

About Finder

Every month 2.6 million unique visitors turn to Finder to save money and time, and to make important life choices. We compare virtually everything from credit cards, phone plans, health insurance, travel deals and much more.

Our free service is 100% independently-owned by three Australians: Fred Schebesta, Frank Restuccia and Jeremy Cabral. Since launching in 2006, Finder has helped Aussies find what they need from 1,800+ brands across 100+ categories.

We continue to expand and launch around the globe, and now have offices in Australia, the United States, the United Kingdom, Canada, Poland and the Philippines. For further information visit www.finder.com.au.

12.6 million average unique monthly audience (June- September 2019), Nielsen Digital Panel