- Bessie Hassan

- Head of PR & Money Expert

- finder.com.au

- +61 402 567 568

- Bessie.Hassan@finder.com.au

Media Release

RBA survey: Local banks may echo US Federal Reserve with out-of-cycle rate hikes – May, 2018

- No cash rate movement expected for May 2018

- Rising interest rates in the US could spur out-of-cycle rate hikes among Australian banks

- 53% of experts and economists have a negative outlook for household debt

30 April, 2018, Sydney, Australia – The cash rate is likely to remain untouched at the next board meeting (01/04/2018), but increased rates from the US Federal Reserve may trigger out-of-cycle rate hikes within the Australian lending market, according to finder.com.au research.

When asked to predict the cash rate decision for May 2018, 97% (29/30) members of the finder.com.au RBA survey forecast no change.

Experts and economists believe a mixed economic climate and low inflation are the main catalysts behind this expected monetary policy decision.

Eighty-seven percent of economists who weighed in on the direction of the next rate move believe the Reserve Bank of Australia (RBA) will push the cash rate upwards.

Economists were also asked to indicate exactly when the next cash rate change may happen.

Graham Cooke, Insights Manager at finder.com.au, says the estimated time of a rate movement is creeping forward.

“Of the seventeen economists who specified a date for an upward rate movement, fourteen of them (82%) don't expect this to happen until 2019.”

“We could be looking at a stagnant cash rate for the rest of the year, at least,” he says.

An Australian online bank recently lifted interest rates out-of-cycle for owner-occupiers and investors, citing increased funding costs as a result of rising US interest rates. When asked about this, most panellists (14, 78%) from the survey are expecting other banks to follow suit.

“Increased international lending costs may force banks to increase rates for home loan customers out-of-cycle, even if the cash rate doesn’t budge.

“The days of super-low interest may be over for borrowers sooner than expected.

“Brace yourself for out-of-cycle rate hikes, especially if the US Federal Reserve lifts rates again,” Mr Cooke says.

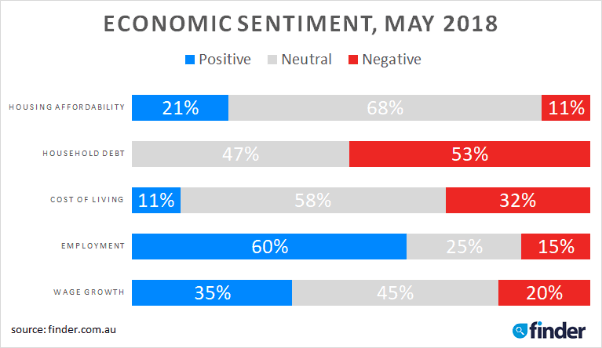

When considering the broader economic outlook, household debt was pinpointed as an area of concern in finder’s Economic Sentiment Tracker. Of the 17 panellists who participated, none had a positive outlook for household debt.

In fact, 53% of respondents reported a negative outlook on household debt.

“With household debt at an all-time high, this does not bode well for stressed borrowers,” Mr Cooke says.

On the other hand, the highest percentage of positive sentiment was given to employment (60%) followed by wage growth (35%) and housing affordability (21%).

“This optimism for future employment has likely been fostered by government support.

“Employment was a key part of the 2017-18 budget with a focus on helping disadvantaged members of society such as parents, Indigenous Australians and older people, find employment opportunities.

“Initiatives such as ParentsNext and Closing the Gap are two examples of this, and it’s likely employment and job creation will remain a central theme in the 2018-19 budget, due to be released next Tuesday (08/05/2018),” Mr Cooke says.

Here’s what our experts had to say:

Jordan Eliseo, ABC Bullion (Hold): "The RBA will keep the cash rate steady at 1.50% at their next meeting. Inflation is soft, property prices are easing, and employment growth looks to be slowing down, so we are still of a view that the next move will be a cut, though this will take some time to come through."

Shane Oliver, AMP Capital (Hold): "Strong business conditions and employment, rising non-mining investment, strong global growth and the RBA's own forecasts argue against a cut but low inflation and wages growth, risks around the outlook for consumer spending, the slowing Sydney and Melbourne property markets and tightening bank lending standards argue against a hike. So the RBA is likely to remain on hold."

Alison Booth, ANU (Hold): " The fundamentals do not yet justify a change."

John Hewson, ANU (Hold): "Economy still mixed Household debt constraint"

Malcolm Wood, Baillieu Holst (Hold): "Muddle-through economy, inflation at low end of target band"

Paul Dales, Capital Economics (Hold): "Economic growth and inflation still aren't strong enough to warrant higher interest rates"

Michael Blythe, CBA (Hold): "Inflation is low, the downtrend in unemployment appears to have stalled and the RBA is emphasising ‘patience’."

Saul Eslake, Corinna Economic Advisory (Hold): "None of the data released since the last meeting, nor anything else that has occurred since then, will have altered the RBA's assessment of the economic outlook sufficiently to prompt a change in its view that current monetary policy settings are appropriate for the time being."

Peter Gilmore, Gateway Bank (Hold): "The RBA knows that pressure from home price rises is beginning to stabilise, however, it's still too soon to move on the cash rate with so many borrowers heavily exposed to rising rates and inflation still low."

Mark Brimble , Griffith Uni (Hold): "Insufficient traction or momentum in the economy to consider any tightening for the year"

Shane Garrett, Housing Industry Association (Hold): "No real inflationary pressures, strong jobs market."

Alex Joiner, IFM Investors (Hold): "The economy is tracking along the RBA's own projections, however private demand is picking up only gradually and consequently inflationary pressures remain modest. Further strong labour market outcomes have not as yet prompted a discernible acceleration of broad-based wages growth that would underpin an inflationary pulse. The RBA has little cause to shift its policy stance as a result. "

Michael Witts, ING Bank (Hold): "Month on month no significant changes to require changes in policy rate."

Leanne Pilkington, Laing+Simmons (Hold): "The fundamentals have remained relatively static, meaning the RBA has no impetus to adjust interest rates at this time. There’s a strong argument to leave the cash rate unchanged for the foreseeable future given stagnant house prices, the marked drop in investor lending and other macro challenges to the economy, especially when the banks cannot be trusted not to hike rates independently."

Mathew Tiller, LJ Hooker (Hold): "Inflation and wages growth remain too soft to see any movement in the cash rate."

John Caelli, ME (Hold): "The RBA will want to see inflation and wages improve and lower unemployment before making any changes."

Michael Yardney, Metropole Property Strategists (Hold): "RBA Governor Philip Lowe has warned the next shift in the official cash rate will be up rather than down, but there is no reason for this to occur until there is a pick up in economic growth and wages. Both of these are likely to be gradual so there is no case for any near-term change in policy."

Mark Crosby, Monash University (Hold): "The RBA have signalled that they will keep rates at low levels for a while longer, but that the next move is likely to be upwards."

Jacqueline Dearle, Mortgage Choice (Hold): "When the economy can better absorb the impact of an increase and inflation is at 2% or near that target level, Gov Lowe will lift the rate."

Dr Andrew Wilson, My Housing Market (Increase): "Latest data remains neutral for the current setting environment with ABS March quarter CPI still clearly underwhelming.

Predictable end to APRA market manipulation reflects generally moderated housing market activity so RBA can concentrate on main macro game."

Alan Oster, NAB (Hold): "Too early to change.Waiting on data regarding wages and unemployment."

Matthew Peter, QIC (Hold): "After the tepid March quarter CPI report and the ongoing slowdown in the housing market, the RBA can park monetary policy into 2019."

Noel Whittaker, QUT (Hold): "Wont drop them - property prices flat - why move."

Nerida Conisbee, REA Group (Hold): "Although momentum seems to be slowly building in the Australian economy, it still isn't at a point where interest rates will start to increase. We are now running at quite a different speed to large parts of the rest of the world - our time will come but it is taking lot longer than expected."

Christine Williams, Smarter Property Investing P/L (Hold): "Even with unemployment reducing and the positiveness within the business sector, and the slowing of the housing market in many states I feel with the Royal Commission at is peak and the findings that have been released the RBA Reserve Bank would be very courageous to increase interest rates at the present."

Janu Chan, St.George Bank (Hold): "The RBA has explicitly stated that the next move is likely to be up, but given that spare capacity remains in the labour market, wage growth continues to be subdued and inflation pressure muted a hike is not likely to occur for some time."

Brian Parker, Sunsuper (Hold): "Nothing in the recent data to force them to adjust rates one way or the other. Still enough labour market slack to keep them from raising rates, and they've made it clear they would be very reluctant to ease at this point."

Clement Tisdell, UQ-School of Economics (Hold): "I agree with Kohler's assessment."

Other participants: Bill Evans, Westpac (Hold).

###

For further information

- Bessie Hassan

- Head of PR & Money Expert

- finder.com.au

- +61 402 567 568

- Bessie.Hassan@finder.com.au

Disclaimer

The information in this release is accurate as of the date published, but rates, fees and other product features may have changed. Please see updated product information on finder.com.au's review pages for the current correct values.

About Finder

Every month 2.6 million unique visitors turn to Finder to save money and time, and to make important life choices. We compare virtually everything from credit cards, phone plans, health insurance, travel deals and much more.

Our free service is 100% independently-owned by three Australians: Fred Schebesta, Frank Restuccia and Jeremy Cabral. Since launching in 2006, Finder has helped Aussies find what they need from 1,800+ brands across 100+ categories.

We continue to expand and launch around the globe, and now have offices in Australia, the United States, the United Kingdom, Canada, Poland and the Philippines. For further information visit www.finder.com.au.

12.6 million average unique monthly audience (June- September 2019), Nielsen Digital Panel