These products offer the best value and outcomes considering various product features and price.

7+

Great

Competitive products within their group.

5+

Standard

But these products still offer reasonable value and have the basics sorted.

0+

Basic

Offering basic cover with limited features or higher pricing.

Our verdict

Pros

Bupa Health Insurance and Bupa Ultimate Health Insurance members may be eligible for discounts on their premium. Check Bupa's website to see the latest offer.

With an Australian-based customer care service and a 24/7 emergency phone line, you can get support whenever you need it.

If Bupa's Comprehensive cover isn't enough, you can upgrade to 'Ultimate Cover' for extra perks. (However, you will have to pay more).

Cons

We compared 37 comprehensive car insurance policies. On average, 22 brands offered cheaper comprehensive car insurance than Bupa.

Bupa's product disclosure statement includes vague terminology like 'reasonable costs'. This makes it difficult to know exactly what exactly you're covered for.

If you want your own choice of repairer, you'll have to upgrade to 'Ultimate Cover' and pay a higher premium.

How does Bupa compare with other car insurers?

We obtained quotes across a range of providers for a 30 year old male based in NSW.

We currently don't have that product, but here are others to consider:

How we picked these

Finder Score for car insurance

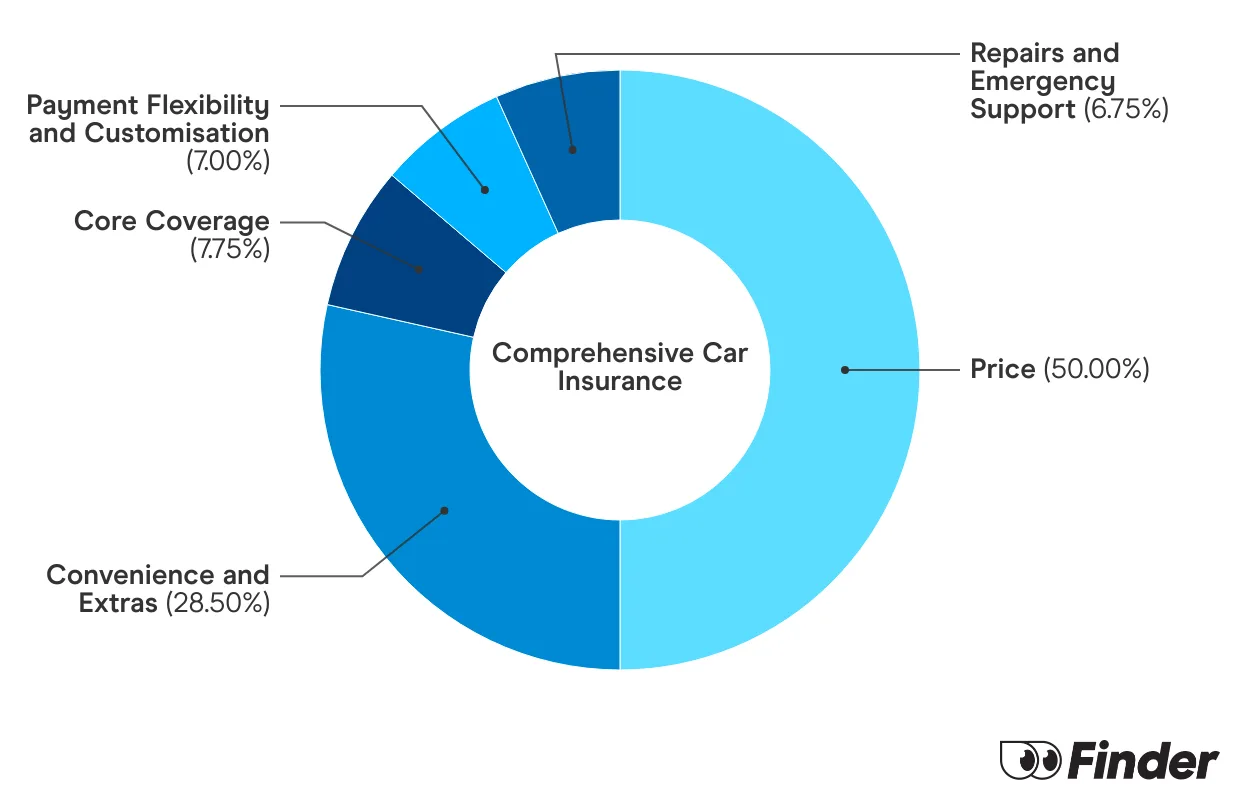

We analyse over 30 car insurance products across insurance providers, and rate each one for price and features. We collect up to 36 quotes per product, for male and female drivers in New South Wales, Victoria, Queensland, South Australia, Tasmania and Western Australia. Quotes are collected for 20 year olds, 30 year olds and 60 year olds, assuming an excess of $850 for a 2020 Toyota Corolla 4 door sedan model, with an average 15,000 kms driven each year. While we are not allowed to display actual quotes, our Finder Score aims to serve as an indicative guide to how cost and feature competitive a product might be for you.

Our feature score assesses each product for more than 15 features across loss and damage coverage, repairs and assistance coverage, personal items coverage and policy coverage. Features we assess include but are not limited to legal liability, essential repairs, new car replacement, car hire events, roadside assistance, agreed or market value, windscreen damage and natural disaster coverage.

Depending on your answers to our car insurance quiz, we upweight the relevant price score or feature score to generate a dynamic Finder Score. Finder Score, Price Score and Feature Score are only to be used as indicative guides and are not product recommendations.

The ability to add extra cover options can help you craft the best car insurance policy for your needs. Keep in mind, limits apply to all of these additional cover options. Be sure to read the product disclosure statement.

Pay as you drive. If you drive less than 15,000 km a year, you could get cheaper cover.

Hire car cover. Get cover for the cost of a hire car if your insured car is stolen or damaged.

Excess-free windscreen cover. Bupa will pay for the cost of repairing or replacing your windscreen if it's broken or damaged.

Excess-free kangaroo damage cover. If your car is damaged in an accidental animal collision, Bupa will waive the excess.

Sports gear cover. Bupa will pay up to $3,000 for sports gear stored in your car if it's damaged or stolen.

Roadside emergency assist. Access to 24/7 roadside assistance and an Australian-based emergency support helpline.

Bupa Ultimate. Upgrade your policy to Bupa Ultimate to choose your own repairer in the event of an accident and to increase your claimable amounts.

FAQs

What's good really depends on what you need and what you're willing to pay. In our research of 37 comprehensive car insurance providers, Bupa sits around the middle of the pack.

Bupa car insurance is underwritten by Hollard and administered by Open.

Yes, you can pick an excess from $500 up to $5,000. The higher your excess, the lower your premium will be, and vice versa.

In most cases, you can lodge your claim online, via Bupa's online portal. You'll need the email address you used when you joined Bupa.

Alternatively, you can email Bupa at help@gi.bupa.com.au or call Bupa on 02 7201 5060 or 1300 976 062.

Nicola Middlemiss is a journalist with nearly a decade of experience in personal finance and insurance. She has contributed to Domain, Yahoo Finance, Money Magazine and Insurance Business Australia, offering in-depth insights into commercial insurance in the Australian market. Nicola holds a Bachelor’s degree in English from the University of Leeds and a Tier 1 General Insurance (General Advice) certification, which complies with ASIC standards.

See full bio

Nicola's expertise

Nicola

has written

256

Finder guides across topics including:

Personal finance

Personal insurance, including car, health, home, life, pet and travel insurance

Hume Bank Car Insurance, issued by Allianz Australia Insurance Limited, provides three levels of cover, a wide range of benefits and the peace of mind that comes with 24/7 claims support.

Compare cover from a range of car insurance providers and find out some of the things you will be covered for under a comprehensive policy.

Important information about this website

Finder makes money from featured partners, but editorial opinions are our own.

Finder is one of Australia's leading comparison websites. We are committed to our readers and stand by our editorial principles.

We try to take an open and transparent approach and provide a broad-based comparison service. However, you should be aware that while we are an independently owned service, our comparison service does not include all providers or all products available in the market.

Some product issuers may provide products or offer services through multiple brands, associated companies or different labeling arrangements. This can make it difficult for consumers to compare alternatives or identify the companies behind the products. However, we aim to provide information to enable consumers to understand these issues.

We make money by featuring products on our site. Compensation received from the providers featured on our site can influence which products we write about as well as where and how products appear on our page, but the order or placement of these products does not influence our assessment or opinions of them, nor is it an endorsement or recommendation for them.

Products marked as 'Top Pick', 'Promoted' or 'Advertisement' are prominently displayed either as a result of a commercial advertising arrangement or to highlight a particular product, provider or feature. Finder may receive remuneration from the Provider if you click on the related link, purchase or enquire about the product. Finder's decision to show a 'promoted' product is neither a recommendation that the product is appropriate for you nor an indication that the product is the best in its category. We encourage you to use the tools and information we provide to compare your options.

Where our site links to particular products or displays 'Go to site' buttons, we may receive a commission, referral fee or payment when you click on those buttons or apply for a product.

When products are grouped in a table or list, the order in which they are initially sorted may be influenced by a range of factors including price, fees and discounts; commercial partnerships; product features; and brand popularity. We provide tools so you can sort and filter these lists to highlight features that matter to you.

Please read our website terms of use and privacy policy for more information about our services and our approach to privacy.

We update our data regularly, but information can change between updates. Confirm details with the provider you're interested in before making a decision.

How likely would you be to recommend Finder to a friend or colleague?

0

1

2

3

4

5

6

7

8

9

10

Very UnlikelyExtremely Likely

Required

Thank you for your feedback.

Our goal is to create the best possible product, and your thoughts, ideas and suggestions play a major role in helping us identify opportunities to improve.

The information provided by Frankie is general in nature and has been prepared without considering your objectives, financial situation or needs. Frankie may make mistakes so it's important that you review the information before deciding. By messaging Frankie, you agree to our Terms and have read our Privacy Policy.